Cryptocurrency lending has emerged as a viable option for those looking to earn passive income on their digital assets or for those needing liquidity without selling their investments. With a wide array of crypto platforms offering services in this space, deciding which one to opt for can be a challenge.

In this article, we guide you through this process. We’ll consider aspects like the platform’s reputation, safety measures, loan terms, collateral requirements, and other key features. Whether you are an experienced investor seeking to make the most of your holdings, or a newcomer exploring borrowing options, this guide will provide the necessary insights to help you navigate the exciting world of crypto lending.

Methodology

BeInCrypto has thoroughly explored cryptocurrency lending platforms, focusing on YouHodler, Binance, and KuCoin for their standout features in lending and borrowing options, alongside ease of use. These platforms offer services tailored for novice and experienced users, featuring various financial tools, including margin trading, futures, and staking.

Through six months of rigorous evaluation, the review emphasizes the platforms’ user-friendly interfaces and comprehensive functionalities, ensuring users can effortlessly access lending services to enhance their crypto finance management.

YouHodler

-

- Provides loans in both crypto and fiat with competitive rates and a loan-to-value ratio of up to 90%.

- Supports a wide range of crypto tokens for loans and features Turbocharge and Multi HODL for investment growth.

- Offers interest-generating investment tools for earning passive income through asset storage.

KuCoin

-

- Features an easy-to-use platform for lending crypto assets with potential interest rates up to 12% for stablecoins like USDT.

- Designed for users seeking to earn passive income through a simple lending process.

Binance

-

- Offers flexible crypto loans with crypto assets as collateral, featuring market-adjusted interest rates.

- Allows for borrowing without fixed terms, providing a user-friendly environment for adaptable borrowing needs.

For further details on BeInCrypto’s verification methodology, follow this link.

- Popular cryptocurrency lending platforms

- 1. YouHodler

- 2. Binance

- 3. KuCoin

- What are cryptocurrency lending platforms?

- How to choose a cryptocurrency lending platform?

- What happens if I don’t pay back a crypto loan?

- How do I lend my cryptocurrency?

- What’s the best crypto lending platform for me?

- Frequently asked questions

Popular cryptocurrency lending platforms

1. YouHodler

YouHodler is a viable choice as a cryptocurrency lending platform due to its extensive range of services and products. It provides numerous passive income opportunities, and users can their crypto holdings to earn an interest on assets such as ETH, BTC, AVAX, and USDT.

The platform offers attractive savings options from simple yield-generating wallets to dual-yield pools, with up to 12% APR on select crypto tokens.

For borrowers, YouHodler offers crypto and fiat loans with competitive rates. The platform supports a high loan-to-value ratio of up to 90% and includes a broad selection of crypto tokens for loans. Its distinct features include Turbocharge and Multi HODL, which allow users to maximize their investments. The platform also provides interest-generating investment tools, letting users earn a passive income simply by storing assets in their YouHodler account.

Additionally, YouHodler offers dual and crypto savings accounts, enabling users to combine their crypto assets in a pool to earn boosted yield rewards. It provides regular payouts, including weekly savings interest payouts and instant crypto-backed loan payouts.

- User-friendly with a mobile app

- Diverse product offerings

- Competitive yield rates on savings

- Max loan term of 364 days.

- Not available in some countries, including the U.S.

- High minimum deposit of $100 in fiat

1. Access the “Loans” section. This is where you manage and create new loans on the YouHodler platform.

2. Create a new loan. Click on the “+” sign on your left to start the process.

3. Check loan terms. Depending on your chosen crypto asset as collateral, YouHodler offers different loan terms. Review the daily fees, maximum loan term (up to 364 days), and LTV (loan-to-value) ratios. Higher LTV ratios can mean higher risks and fees.

4. Set your collateral. Choose the amount of your crypto holdings you’d like to use as collateral. The value should be at least equivalent to 100 USDT for the loan to go through.

5. Confirm your loan. Review the conditions and fees for your crypto loan. Once you agree with the terms, click “Get Loan.”

6. Manage your loan. Once the loan is issued, you can manage it under the “Loans” section. The loan amount will be deposited in the corresponding wallet in your YouHodler account.

2. Binance

Binance offers an advantageous crypto lending platform, thanks to its wide variety of supported loanable and collateral assets including BTC, ETH, USDT, BUSD, BNB, among others. It offers two loan types – flexible and stable.

With flexible loans, you can borrow cryptocurrencies using your crypto assets as collateral without committing to a specific term. The interest rate is determined by market conditions and the type of cryptocurrency being borrowed.

On the other hand, stable loans let you borrow USDT or BUSD against your cryptocurrency holdings at a fixed interest rate based on the loan-to-value (LTV) ratio. This type of loan is great if you need quick cash access and are willing to use your crypto holdings as collateral.

Unlike traditional banks, Binance’s collateral system is robust, allowing you to borrow up to 60% of your collateral’s value. However, it’s essential to note that Binance reserves the right to claim the collateral if the current loan value exceeds the value of the pledged collateral (margin calls).

- Instant loans with flexible repayments

- Ideal for underbanked populations, people with little to no credit history, and self-employed workers

- Fast loans allow you to get quick money without having to liquidate assets

- Offers lower interest rates with a crypto-secured loan

- Need to keep an eye out on the margin calls

- The crypto collateral can be risky in volatile markets

- Late repayments risk liquidation and a 2% liquidation fee

1. Create and verify your Binance account if you don’t already have one.

2. On the Binance homepage, hover over ‘Payment’ and click on ‘Binance Loans’.

3. Choose a loan type (stable or flexible) and enter the amount you wish to borrow. Then, select a collateral asset.

4. The system will calculate the collateral amount based on the initial Loan-to-Value (LTV) ratio. You will also see the annualized and net-annualized interest rates, estimated hourly interest, and liquidation price.

5. Read and agree to Binance’s Loan Service Agreement and Simple Earn Service Agreement before checking the box next to it and clicking ‘Start Borrowing’.

6. A pop-up confirming the loan will appear. Click ‘Confirm’ to complete the process.

3. KuCoin

Established in 2017, KuCoin is a reputable cryptocurrency exchange that has made a name for itself in the crypto lending industry through its platform, KuCoin Lending. This service provides an easy-to-use platform for anyone looking to lend their crypto assets and earn a passive income. Lenders will find interest rates of up to 12% for stables such as USDT on the platform.

Borrowing crypto on KuCoin is only available for traders using their margin trading platform. Borrowers can’t withdraw the funds to other platforms.

- Low trading fees

- Huge variety of cryptocurrencies

- Easy access to lending and borrowing features

- High APY for lenders

- Lacks a U.S. operating license

- Website usability may be challenging

- Borrowing available only for margin trading

1. Start by adding assets to your Main Account that you wish to lend.

2. Navigate to the lending marketplace by clicking on ‘Finance > Crypto Lending’ on the top menu of your dashboard. You’ll be redirected to the marketplace where you can see the list of coins you can lend on the left sidebar. Click on a coin to see the daily returns you can earn.

3. Open a Lending Order. Fill in the ‘Loan Amount’, ‘Daily Interest Rate’ (which ranges from 0 to 0.2%), and ‘Lend Terms’ (7 / 14 / 28 days) to open a lending order. The daily returns are shown in daily interests; you can calculate the annual return by multiplying this by 365. Rates generally range from 3% to 70%, depending on the coin you’re lending.

4. Wait for Order Match. After opening an order, it will be listed on the market. All open orders are displayed on the right side of the screen. Once your order is matched, it’s moved to the ‘Unsettled’ page and officially becomes a loan.

What are cryptocurrency lending platforms?

Cryptocurrency lending platforms are online services that allow individuals to lend or borrow cryptocurrencies. These platforms can offer much higher annual percentage yields (APYs) than traditional high-interest savings accounts.

These platforms can be centralized or decentralized. Centralized platforms typically adhere to regulatory protocols like Know Your Customer (KYC) and anti-money laundering measures to mitigate risk.

Decentralized crypto lending platforms use smart contracts to automate loan payouts and yields. Users can deposit collateral, often in the form of crypto assets, to automatically receive a crypto loan if they meet the platform’s requirements.

One key advantage of bypassing traditional banks is that lending and borrowing become faster, more convenient, and often cheaper.

Depending on your geographical location, some of these services may not be available. This is especially true for crypto lending platforms in the US, which face regulatory scrutiny. For instance, Binance US doesn’t offer crypto lending, unlike its parent company Binance. Regulatory bodies like the U.S. Securities and Exchange Commission (SEC) are currently developing comprehensive regulations for the cryptocurrency market.

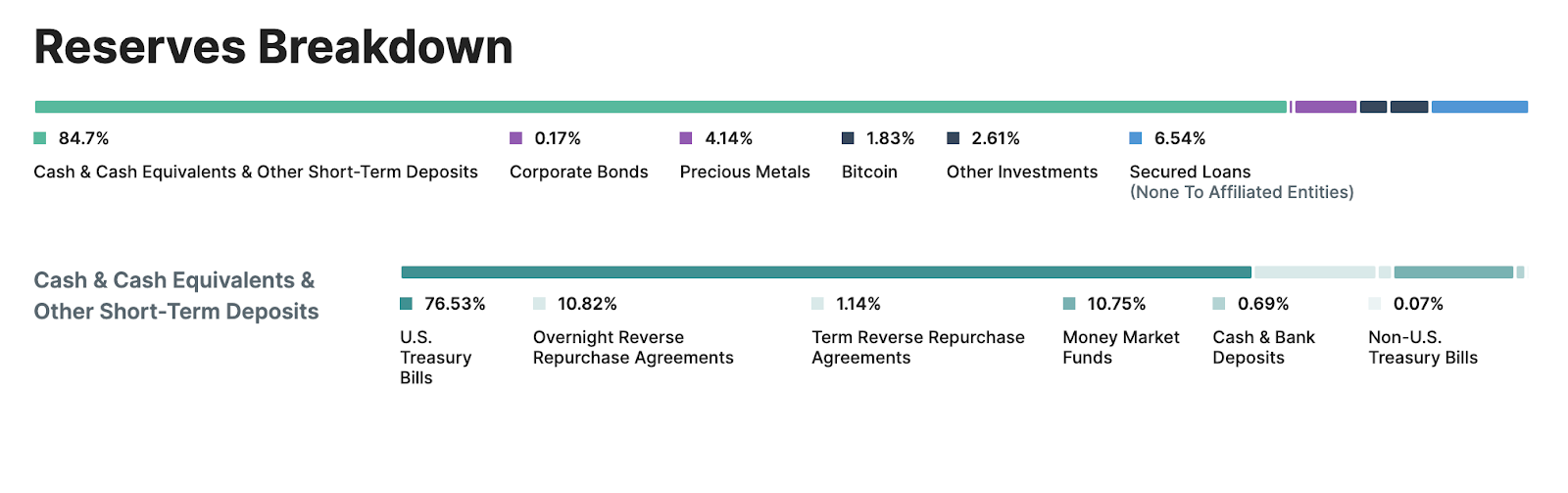

One of the most wanted cryptos for both lending and borrowing is USDT, a stablecoin backed by real-world assets. According to Tether.to, more than 84% of the available liquidity is backed by cash and short-term deposits.

However, there are risks involved. Just like any investment, you could lose money. The crypto market is still young and unpredictable, so it’s crucial to consider your financial goals and risk capacity carefully. It’s also vital to pick a reliable platform with a strong security track record. Always remember to do your research and think twice before lending or borrowing crypto.

How to choose a cryptocurrency lending platform?

When choosing a cryptocurrency lending platform to secure a favorable loan or earn income, you are responsible for performing your due diligence.

Remember, all investments come with risks, so it’s essential to make informed decisions when dealing with crypto lending platforms. Let’s go over some of the most important factors when choosing your crypto loan platform.

Assessing platform security

Assessing a crypto platform’s security is crucial due to the lack of federal deposit insurance, unlike traditional banks, where deposits are guaranteed up to a certain limit. If a crypto platform becomes insolvent, you risk losing all your funds, and your assets become part of the insolvency proceedings.

Centralized crypto lenders such as Binance are more accountable in case of insolvency as compared to decentralized finance DeFi platforms. DeFi platforms technically can’t file for bankruptcy, and in such events, there might not be sufficient liquidity for new loans or interest payments.

To manage this risk:

- Diversify. Don’t put all your crypto assets on one platform. Spreading your holdings across multiple platforms can minimize potential losses.

- Choose carefully. Consider the platform’s reputation, security measures, and history of handling insolvency or hacking events.

- Consider DeFi. While they present their own unique risks, DeFi lending platforms can sometimes be safer in regard to insolvency as they often operate through smart contracts and are more decentralized, thus spreading the risk.

Evaluating interest rates

Interest rate is a key factor when choosing an option among the best platforms for crypto lending. Select a platform that offers a favorable interest rate for your particular crypto assets. DeFi rates tend to be higher when choosing to lend crypto assets.

With careful research, you can find crypto loans with interest rates under 10% or even as low as 0% in some instances.

Understanding loan terms

Crypto lending involves using your digital assets, similar to a property in a mortgage, as collateral to secure a loan. The process involves collateralizing your crypto holdings, receiving the loan, and then paying it off over time to reclaim your collateral. It’s a useful way to access cash without needing to liquidate your cryptocurrency holdings.

There are options for crypto lending without collateral in the form of flash loans, but this option requires a thorough understanding of the crypto space and the associated DeFi lending platforms.

The amount you can borrow is determined by the value of your collateral, which is calculated using a loan-to-value (LTV) ratio. For instance, if a platform offers a 50% LTV ratio, you would need to put up $10,000 in crypto as collateral to borrow $5,000.

You still technically own the cryptocurrency used as collateral, but you lose certain privileges, like trading or selling them, until you fully repay the loan.

Investigating platform fees

Crypto lending platforms, much like traditional banks, charge interest fees on loans. These can vary greatly, ranging from around 0.5% APR to over 12% APR. Ensure you review the platform’s crypto lending rates and terms to avoid any surprises. Depending on the use of the loan, it’s possible to write off these interest fees on your taxes, especially if it’s used for investment or business purposes. Consult a tax professional for precise guidance.

Checking liquidity

Liquidity in crypto lending platforms refers to the ease with which digital assets can be converted into cash or other tokens without impacting the market price. It’s a key factor in understanding the operational efficiency of these platforms.

Two main types of crypto lending platforms exist: decentralized and centralized.

Decentralized platforms use liquidity pools, essentially pool funds provided by lenders. Here, peer-to-peer lending in crypto is possible using automated smart contracts to manage interest rates based on the liquidity level of each pool. If a pool (for example, an Ether pool) is low on liquidity, the smart contract will increase the interest rates to attract more lenders and encourage borrowers to repay their loans. When lenders contribute assets to the pool, they receive a token equivalent from the platform, which gains interest over time.

On the other hand, crypto lending on Binance and other centralized platforms involves the management of liquidity from a centralized pool of deposits. They determine interest rates and approve loans individually. Centralized lenders may also diversify their income streams to provide returns to depositors.

Checking liquidity on a crypto lending platform involves understanding the source of its liquidity and how it manages interest rates and loan approvals. This understanding can help assess the platform’s stability and operational efficiency.

Evaluating loan-to-value (LTV) ratio

Loan-to-value (LTV) is a financial metric used by crypto lending platforms to determine the risk associated with a loan. It compares the value of the borrower’s crypto assets used as collateral to the loan amount. High LTV ratios indicate high-risk loans are often subject to higher interest rates, while low LTV ratios suggest low-risk loans with lower interest rates.

This is the LTV formula:

LTV = Loan Amount / Collateral Amount x 100%

(Loan Amount = Principal + Interest)

Unlike traditional financial institutions that use credit histories to evaluate borrowers, crypto lending platforms rely primarily on the LTV ratio as they typically do not perform background checks.

This ratio becomes crucial during market volatility as a sharp drop in crypto asset values can increase the LTV, potentially leading to the sale of the collateral if borrowers fail to repay the loan or add more collateral. Popular crypto lending platforms like YouHodler offer LTV ratios ranging up to 90%, based on the type of crypto assets used as collateral.

Checking a platform’s reputation

When choosing a crypto lending platform, it’s crucial to opt for one with a robust reputation in the market. Secured lending in the crypto market largely depends on the measures a platform has put in place. Seek out cryptocurrency loan providers with a history of several years in the industry, demonstrating consistency and reliability.

A proven customer satisfaction record also speaks volumes about the platform’s credibility. Don’t just rely on a company’s own words; do your research, read reviews, and check user feedback to get a well-rounded view of the platform’s reputation.

User experience

The user experience of a cryptocurrency lending platform is critical in fostering adoption and making the platform more accessible. Many potential investors are often dissuaded from venturing into cryptocurrencies due to the perceived complexity of the platforms.

What happens if I don’t pay back a crypto loan?

There are two types of loans – crypto loans without collateral and those with collateral.

With collateralized loans, you pledge a certain amount of crypto (see Loan-To-Value ratios) to receive a larger loan. This system’s design protects the lender should the value of the borrowed crypto dip below the loan’s value. Once you repay the interest and the loan, the lender returns your collateral crypto. However, failing to repay your loan exposes you to the risk of liquidation, and the lender may use your collateral to cover the debt.

The other type of loan is crypto loans without collateral, which have emerged thanks to decentralized finance (DeFi) protocols. Platforms like Aave, dYdX, and Uniswap primarily offer flash loans, executing loan terms and conditions using smart contracts. Borrowers take and return these loans almost instantaneously, often to capitalize on arbitrage opportunities.

If a borrower fails to repay the capital or doesn’t meet the conditions of the smart contract, the smart contract reverses the transaction and returns the funds to the lender. However, there is a scarcity of platforms offering crypto loans without collateral, and it’s crucial to do thorough research before engaging with these platforms, as they may be targets for scammers.

How do I lend my cryptocurrency?

You can also choose to earn a passive income using your crypto holdings. When you want to learn how to earn interest on cryptocurrency, you first need to choose and deposit your crypto asset on a crypto platform that offers earning through lending.

Depending on the crypto lending service, this feature may also be called earning, savings, or deposits. In exchange for your deposit, you will receive an interest rate similar to how traditional bank deposits work.

However, interest rates vary depending on the crypto asset and chosen platform. Also, most crypto lending platforms accept popular assets, but it might be difficult to find a platform that accepts lesser-known crypto.

As a crypto lender, you may choose between flexible or fixed deposits. The interest rate is called APR (annual percentage rate). When you withdraw your deposit, you will also receive the corresponding interest. Note that the APR is not guaranteed and can fluctuate.

All these details should be researched at the time of your deposit because crypto platforms tend to change earning conditions for lenders regularly. Ensure you take the time to learn the risks and benefits of cryptocurrency lending to inform your decision on whether it suits your investment profile.

| Platform | LTV Ratio | Availability | Cryptos | Terms |

| YouHodler | 50-90% | E.U. | BTC & 50+ Others | One year |

| Binance | 60% | E.U. & 100+ Countries | BTC & 380+ Others | 7/14/30/90/180 days |

| Bake (Cake DeFi) | 50% | E.U. & 150+ Countries | BTC & 7 Others | N/A |

| Bybit | 65% | E.U. & 100+ Countries | BTC & 40 Others | 7/14/30/90/180 days |

| Nexo | 90% | E.U. & 150+ Countries | BTC & 60 Others | Up to 1 year |

| OKX | 65% | E.U. & 100+ Countries | BTC & 100 Others | N/A |

| KuCoin | N/A | U.K. & 150+ Countries | BTC & 50 Others | 7/14/28 days |

What’s the best crypto lending platform for me?

If you aim to earn a passive income from your crypto holdings, you may use these crypto lending platforms to deposit your digital assets. Note that the interest rates vary, and some assets have a higher interest rate than others. Before entering into any lending agreement, you should always carefully consider your individual financial goals, risk tolerance, and the need for liquidity.

Frequently asked questions

What is the best crypto lending platform?

What is a cryptocurrency lending platform?

Are crypto lending platforms safe?

Is crypto lending a good idea?

Can I lend crypto on Binance?

What is crypto lending?

Is crypto lending a good idea?

What is a crypto lending protocol?

How much can I earn with crypto lending?

Is lending crypto risky?

What are the risks of crypto lending?

Can I lose money lending crypto?

Is crypto lending profitable?

What are the benefits of crypto lending?

Which platform is best for lending crypto?

Disclaimer

In line with the Trust Project guidelines, the educational content on this website is offered in good faith and for general information purposes only. BeInCrypto prioritizes providing high-quality information, taking the time to research and create informative content for readers. While partners may reward the company with commissions for placements in articles, these commissions do not influence the unbiased, honest, and helpful content creation process. Any action taken by the reader based on this information is strictly at their own risk. Please note that our Terms and Conditions, Privacy Policy, and Disclaimers have been updated.