Crypto tax planning is essential to reduce liabilities and ensure compliance with IRS guidelines. In this article, we’ll explore some tax-saving tips for crypto investors and delve into cryptocurrency tax deductions and capital gains tax. Here’s how to reduce crypto tax while staying within the law.

iTrustCapital

- Understand the tax implications of cryptocurrency

- Strategies for minimizing your crypto tax liability

- What is iTrustCapital?

- How to report your cryptocurrency taxes

- Additional tips for reducing your crypto tax liability

- Is it legal to use offshore accounts for crypto tax evasion?

- How can I avoid tax on cryptocurrency?

- How will you reduce your crypto tax liability?

- Frequently asked questions

Understand the tax implications of cryptocurrency

Things can get a bit tricky when it comes to crypto and taxes. One of the big questions is how to classify cryptocurrencies for tax purposes. Should they be considered as property or currency? When people make a profit by selling cryptocurrency, those gains are liable for taxation, much like gains from other assets. And when you use cryptocurrency to make a purchase, it should be subject to the same taxes that apply to cash transactions.

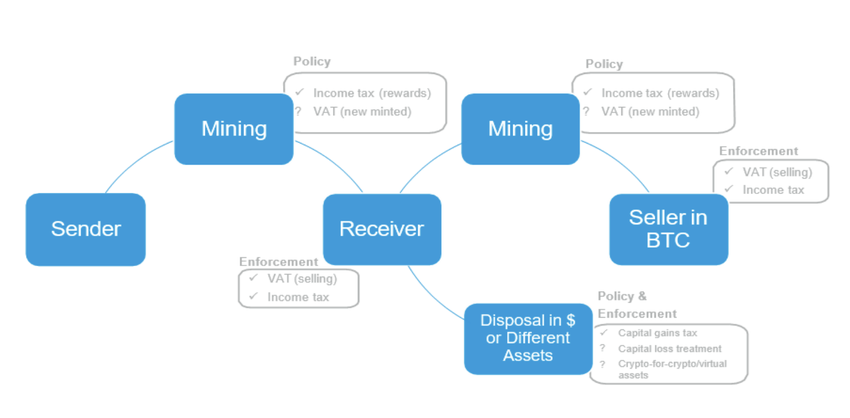

According to a July 2023 report published by the International Monetary Fund, all of the events displayed in the image below are taxable (mining, selling, converting to fiat, converting to other assets).

To do this, we need a clear and consistent way to define cryptocurrencies for tax purposes, treating them as currencies for value-added and sales taxes and as assets for income tax.

While this isn’t straightforward due to the ever-evolving nature of cryptocurrency transactions, it’s definitely doable. The real challenge lies in enforcing these rules. Enforcing tax on cryptocurrency is tricky because transactions are pseudonymous.

In other words, transactions use public addresses that are hard to trace back to individuals or businesses, making tax evasion easier. However, some countries are implementing rules for centralized exchanges, requiring them to perform a KYC (know your customer process) before allowing anyone to trade. Reporting rules for exchanges are growing, but the situation, as of 2026, is in flux.

The real challenge for tax collection is when people use decentralized exchanges or peer-to-peer transactions, which are difficult for tax authorities to monitor.

What is cryptocurrency, and how is it taxed?

Cryptocurrency is a digital, decentralized form of value and exchange. Unlike traditional currencies with physical bills, cryptocurrencies like Bitcoin, Ethereum, and many others exist digitally.

These currencies operate without centralized government oversight, relying instead on encrypted and distributed ledgers known as blockchain technology. Think of these blockchain ledgers as a constantly updated record of all transactions within a particular cryptocurrency, similar to a digital checkbook.

When talking about crypto transactions, income is realized when you dispose of or get rid of your cryptocurrency. Simply owning crypto is not taxable in itself, such as when gifting it or inheriting it. However, tax implications come into play when you:

- Sell or gift cryptocurrency

- Trade or exchange one cryptocurrency for another (e.g., exchanging Bitcoin for Ethereum).

- Convert cryptocurrency to a traditional currency issued by a central bank, like the U.S. dollar or the Euro.

- Use cryptocurrency to purchase goods and services.

Different types of cryptocurrency transactions and their tax implications

In the U.S., cryptocurrency is taxed based on a 2014 IRS ruling that categorizes it as capital assets, much like stocks or bonds, rather than traditional currency, such as dollars or euros.

Many other governments also classify crypto assets as capital assets. The IRS likely chose to treat cryptocurrency as a capital asset because most people view it as an investment. This means that gains on capital assets held for investment purposes are subject to taxation.

When you sell your cryptocurrency at a profit after holding it for more than one year, you incur capital gains taxes. These taxes are typically lower than ordinary income tax rates. For example, if you bought $20 worth of bitcoin and held it for three years, selling it for $200, you’d owe capital gains taxes on the $180 gain.

If you hold cryptocurrency for one year or less and sell it at a profit, you’ll be subject to ordinary income taxes. Conversely, if the value of your cryptocurrency decreases over time, resulting in a capital loss when you sell, you can use that loss to offset other income.

The IRS allows you to reduce your taxable income by up to $3,000 per year ($1,500 if married filing separately) using capital losses. You can continue to claim portions of the loss in subsequent years until the entire loss is offset. If you receive cryptocurrency as a form of wages or income, your employer will report it on your W-2 as fair market value. You must then report this amount on your income tax return and pay ordinary income taxes on the received cryptocurrency.

“As long as you follow the IRS rules, you’ll avoid problems. A crypto CPA knows the details though, so I’d talk to one of them.”

Leo Smigel, Founder of Analyzing Alpha

Understanding these tax implications is crucial for cryptocurrency holders to meet their tax obligations accurately.

Capital gains and losses

Considering cryptocurrency as a capital asset means that it will be subject to taxation whenever it’s sold at a profit. This means that even spending cryptocurrency can incur capital gains tax if its value has increased since you acquired it.

For instance, let’s say you bought $100 worth of Bitcoin and held onto it until its value surged to $1000. If you then used that $1000 worth of Bitcoin to purchase gaming equipment, the $900 profit you made from your initial $100 investment would be subject to a capital gains tax.

So, whether you spend it or sell it, as long as your initial investment realizes a profit, you owe crypto tax. However, if your crypto investment suffered a loss, you wouldn’t need to pay taxes when selling or spending it. You can even use your crypto losses to offset other investment gains. If you’re looking to reduce crypto tax, don’t cut corners. Failing to report crypto income is considered a violation of federal law, leading to penalties.

The tax rates on cryptocurrency vary based on your crypto assets’ gains and the holding period, as follows:

- For short-term gains (365 days or less), they are taxed as ordinary income.

- Long-term gains (lasting more than 365 days) are subject to long-term capital gains tax rates.

Note that in some countries, such as the U.K., there are different income tax brackets. Consult our UK tax guide for more info.

Income tax

When it comes to cryptocurrency, income tax applies to various scenarios:

- Getting paid in crypto by an employer

- Receiving crypto for goods or services

- Mining crypto

- Earning staking rewards

- Earning other rewards, which can be part of a reward system for certain cryptos, such as play-to-earn taxable assets

- Getting crypto from a hard fork

- Receiving an airdrop

- Receiving other incentives or rewards

It’s essential to stay informed about the latest crypto tax regulations in your country and accurately report your cryptocurrency income when filing your taxes.

Self-employment tax

Regarding self-employed cryptocurrency endeavors like mining and crypto staking, income tax considerations take center stage. Mining cryptocurrency entails a tax obligation based on the earnings derived from it. The taxable amount is determined by the fair market value of the mined coins at the time of receipt. Notably, if cryptocurrency mining is conducted as a business venture, it falls under the purview of self-employment income taxation.

Staking rewards are akin to mining proceeds in the eyes of taxation. Taxes are assessed by considering the fair market value of these rewards on the day they are received.

Gift and estate tax

The taxation of gifted cryptocurrency is contingent on the value of the gift and certain exemptions. Here’s a breakdown of how it works:

- Annual gift tax exemption: Each government will specify a maximum value for the gift.

- Exceeding the annual limit: If you exceed the limit for gifting cryptocurrency to a single recipient within a tax year, you may be subject to gift tax. There might be workarounds, depending on your government rules.

- The recipient’s tax obligations: When the recipient sells or disposes of the cryptocurrency, they must report the transaction on their tax return.

Keep in mind that both the annual gift tax exemption and the lifetime gift and estate tax exemption can change from year to year. It’s advisable to verify the current exemption limits before making cryptocurrency gifts. It’s essential to stay informed about the latest exemption limits and tax regulations, as they can change over time.

Strategies for minimizing your crypto tax liability

Managing cryptocurrency taxes can be complex, but there are several strategies to help reduce your crypto tax burden. Here’s a brief overview of five practical approaches:

- Hold your crypto long-term

- Harvesting tax losses

- Donations and gifts

- Crypto-friendly jurisdictions

- Consulting tax experts

Reduce crypto tax: Hold your crypto long-term

Holding your cryptocurrency for more than a year can lead to lower tax rates in many countries. Long-term capital gains rates are typically lower than short-term rates, allowing you to save on taxes by holding onto your crypto assets.

Reduce crypto tax: Offset gains with losses

Similar to traditional investments, you can use tax loss harvesting with cryptocurrencies. Sell assets that have decreased in value strategically to offset capital gains, reducing your overall tax liability. Be sure to understand your jurisdiction’s rules on tax loss harvesting.

Reduce crypto tax: Time your sales

Timing your sales is another effective strategy to minimize your tax liability. For instance, in the U.S., when you hold cryptocurrency for over 12 months before selling, you pay less tax. When you golf your crypto for more than 12 months, you can benefit from lower long-term capital gains tax rates (0-20%) compared to short-term rates (10-37%). This approach reduces your tax liability by taking advantage of favorable tax treatment for longer holding periods.

Reduce crypto tax: Consider using a crypto IRA

A Crypto IRA is a retirement investment option that allows individuals to use their retirement savings to invest in cryptocurrencies like Bitcoin.

It operates as a self-directed Individual Retirement Account (IRA) offered by select financial institutions in the U.S. This means you can diversify your retirement portfolio by including cryptocurrencies alongside traditional investments.

While crypto IRAs offer diversification, they come with high risk due to cryptocurrencies’ volatile nature and often involve additional fees and costs.

Investors can choose from various cryptocurrencies, not limited to Bitcoin, including Ethereum, Ripple, Litecoin, Bitcoin Cash, and Ethereum Classic. However, it’s important to note that custodians managing these accounts may not have a fiduciary responsibility to the investor, increasing the risk. Selling crypto for a profit typically incurs capital gains tax.

However, when you buy and sell crypto within a self-directed IRA, you can defer these taxes as long as the funds and assets remain in the account. This tax-efficient approach allows your investments to grow through compounding without the drag of taxes.

What is iTrustCapital?

iTrustCapital offers self-directed IRAs designed for investing in cryptocurrencies, gold, and other commodities. Based in Irvine, California, the company has facilitated more than $4.5 billion in transactions since its inception and boasts a team of over 100 professionals.

With a focus on seamlessly integrating digital finance into the traditional retirement investment system, iTrustCapital provides a user-friendly platform that allows clients to securely and legally transfer funds from their retirement accounts into cryptocurrencies and other commodities.

The platform stands out for its low fees and offers access to over 30 digital assets for trading. Coupled with its strong customer service, diverse IRA account options, and intuitive interface, iTrustCapital is an excellent choice for both novice and experienced investors.

How does iTrustCapital work?

iTrustCapital offers the opportunity for investors to incorporate non-traditional assets such as cryptocurrency and precious metals into their IRA. Similar to regular IRAs, iTrustCapital’s crypto IRAs come with specific tax advantages. Depending on the type of account — whether it’s traditional or Roth — the IRAs can be tax-deferred or tax-free.

Traditional IRAs are funded with pre-tax funds, and taxes are applied to withdrawals. In contrast, Roth IRA contributions are made with post-tax funds, resulting in tax-free withdrawals. The choice between the two depends on an individual’s tax situation and financial objectives.

iTrustCapital provides three funding options. Users can transfer an existing IRA, roll over an employer plan, or open a new account. Direct contributions are typically processed within a few days while rolling over an employer plan may take up to a month.

The trading platform is active and accessible 24/7, allowing users to buy and sell assets once their accounts are funded. All available assets are presented in a user-friendly format, along with their respective prices. Users can execute trades by simply selecting the “Buy” or “Sell” button, with a 1% transaction fee applied to all transactions. To begin trading, an initial minimum deposit of $1,000 is required, followed by a $500 minimum for subsequent contributions.

Want to know more about iTrustCapital? Check out our comprehensive review of the platform here.

What are the benefits of using iTrustCapital for your crypto IRA?

iTrustCapital is a leading digital asset IRA platform that has been operational since 2018. It offers investors the opportunity to include over 35 popular cryptocurrencies as well as physical gold and silver in their IRAs. With over $7 billion in transactions conducted since its inception, iTrustCapital has become a preferred choice among self-directed IRA options for crypto enthusiasts.

Here are the key benefits of using iTrustCapital for your crypto IRA:

- Diversification

- Low fees

- Easy account setup

- Secure custodianship

- Tax advantages

iTrustCapital enables you to diversify your retirement portfolio, which can help protect your retirement savings from market volatility.

There are no monthly maintenance fees; you only pay a 1% transaction fee for cryptocurrency transactions. This fee model is straightforward and cost-effective compared to many other self-directed crypto IRA options.

Setting up an iTrustCapital account is quick and simple. You can choose from various IRA types, including Roth, Traditional, and SEP IRAs. Funding your account can be done via bank wire or check. The account review and opening process typically takes only one to three business days, making it convenient for investors.

iTrustCapital partners with Coinbase as its custodian, ensuring that most of your crypto assets are securely stored in cold storage. Additionally, Coinbase’s insurance policy provides protection against theft, cybercrime, and hacks. Fireblocks, a security provider for digital currency transactions, further enhances security measures.

How to use iTrustCapital to save crypto taxes

Using iTrustCapital to save on crypto taxes involves leveraging the platform’s features and benefits to optimize your tax strategy within the framework of self-directed IRAs. In many jurisdictions, a crypto IRA is tax-deferred. You will not be required to pay taxes for the crypto IRA as long as those assets sit in your account.

Claim mining expenses

To save on crypto taxes by claiming mining expenses, it’s crucial to treat your mining activities as a legitimate business and carefully document your expenses.

Here’s how you can potentially reduce your tax liability:

- Electricity costs

- Equipment expenses

- Office space

- Losses

Electricity is often one of the largest expenses for crypto miners. You can deduct the portion of your electricity bill that’s exclusively used for mining as a business or trade expense.

If you’re mining in a location where electricity serves purposes other than mining, calculate and deduct the portion directly related to Bitcoin mining. Maintaining a separate meter for your mining operation can help with this calculation.

In most cases, you can deduct the purchase price of mining equipment in the year it was bought. If this deduction isn’t suitable, your crypto tax professional may recommend deducting the equipment’s cost over several years (typically 3 to 5). Additionally, expenses related to repairing mining equipment may be deductible as a trade or business expense.

If you rent space specifically for housing your mining rigs, the rental expenses can be deductible. If you’re mining from your home, whether you rent or own, you might be eligible for the home office deduction.

Due to hardware and electricity expenses, coupled with the volatile nature of the crypto market, mining businesses can experience losses in a tax year. In such cases, these losses may be used to offset other sources of income, reducing your overall tax liability.

Consider retirement investments

To reduce crypto tax through retirement investments, prioritize maximizing your contributions to traditional 401(k) and IRA accounts. These contributions are deductible from your taxable income, effectively lowering your tax liability. Traditional accounts offer an immediate tax break, while iTrustCapital accounts allow your investments to grow tax-free, with tax-free withdrawals in retirement.

Additionally, be mindful of contribution deadlines. Workplace 401(k) contributions must be made by the end of the calendar year. In contrast, tax-deductible contributions to traditional IRAs can be made until the tax-filing deadline, typically April 15th of the following year. This flexibility allows you to plan your contributions to optimize tax savings strategically.

Charitable giving

To reduce crypto taxes through charitable giving, you can consider the following strategies:

- Itemize your deductions

- Donor-advised funds

Charitable contributions are deductible on your tax return, but you generally need to itemize your deductions to claim these. This involves listing out all your deductible expenses, including charitable donations, instead of taking the standard deduction.

If you have the means and want to maximize your charitable deductions, you can set up a donor-advised fund. Contributions made to these funds are deductible in the year they are made.

However, the unique advantage of donor-advised funds is that you can then distribute donations to charities over the course of several years. This strategy allows you to bundle several years’ worth of donations into a single year, potentially surpassing the standard deduction threshold and enabling you to itemize deductions.

For example, if you have a substantial amount of cryptocurrency gains in a particular year, you can donate a portion of those gains to a donor-advised fund. This donation reduces your taxable income for that year while still allowing you to distribute the funds to your chosen charities over time. By taking advantage of these strategies, you can reduce your crypto tax liability while supporting charitable causes that matter to you.

How to report your cryptocurrency taxes

Recordkeeping

When it comes to reporting crypto taxes, diligent recordkeeping is crucial. Start by calculating your cryptocurrency gains and losses, as these will determine your tax liability. Crypto disposals that trigger these calculations include selling cryptocurrency for fiat, trading one cryptocurrency for another, or using cryptocurrency to purchase goods and services. To calculate your gain or loss for each transaction, you’ll need to monitor how the price of your cryptocurrency has changed since you originally acquired it.

You can use the following capital gain formula:

Gains (or losses) = Proceeds – cost basis

Your “proceeds” represent what you received when disposing of your cryptocurrency, typically the fair market value at the time of disposal minus any related fees. On the other hand, your “cost basis” is the cost you incurred to acquire the cryptocurrency, typically the fair market value at the time of receipt, plus any fees associated with the acquisition.

Once you’ve completed these calculations for each transaction, you can accurately report your gains and losses when filing your tax return. Proper recordkeeping will not only help you fulfill your tax obligations but also ensure you’re taking advantage of potential deductions and exemptions available to crypto investors.

Tax forms

When it comes to reporting your crypto taxes, you will need to identify the tax form used in your country. For instance, to fill out the U.S. crypto tax form, you have to use IRS Form 8949. This form is used to report the sales and disposals of various capital assets, including cryptocurrencies, along with stocks and bonds.

Here’s what to know before filling in the tax form:

Short-term vs. long-term disposals. Know exactly how long you keep that crypto. Short-term qualifies for under 12 months, and long term are those investments of over 12 months.

Reporting gains and losses. For each of your gains and losses.

Here are some of the details you need to know about each crypto transaction you are reporting:

- A description of the crypto you sold

- The date you originally acquired the crypto

- The date you sold or disposed of the crypto

- Proceeds from the sale (fair market value)

- Your cost basis for purchasing the crypto (fair market value)

- Your resulting gain or loss

Properly filling out the tax form ensures you accurately report your cryptocurrency transactions to the IRS. Keeping meticulous records of your crypto activities is essential, as it helps you complete this form correctly and meet your tax obligations. If you’re unsure about how to fill out the form, you can seek guidance from a tax professional or refer to instructional resources like video tutorials for assistance.

Filing deadlines

Understanding and meeting tax deadlines is crucial to ensure compliance with regulations and reap various benefits.

The consequences of missing tax deadlines can vary from one country to another. However, common penalties for late filing include late fees, forced fines, and, in severe cases, even legal repercussions such as potential jail time.

Benefits of filling your cryptocurrency tax on time:

- Avoid late fees and fines.

- Faster processing: Filing early can expedite the processing of your tax return.

- Strategic trading: Generating your tax report early lets you better plan your trading strategy for the new tax year. Some countries permit taxpayers to offset losses from crypto trading against future gains, so understanding your gains and losses early can help you adapt your trading strategy accordingly.

Staying informed about the specific deadlines and requirements in your country is essential to ensuring timely and accurate tax reporting.

Additional tips for reducing your crypto tax liability

Use a crypto tax software program

Utilize tax software to simplify the process of documenting and calculating your taxes related to cryptocurrency. Crypto tax software streamlines the reporting of your crypto transactions. It can also compute your tax obligations in accordance with your local tax laws.

Hire a tax professional

Hiring a tax professional is a wise decision regarding reducing your tax liability. One reason why it is recommended that you hire a tax expert is because tax laws are complex and constantly changing.

A tax professional has in-depth knowledge of these laws. They can easily navigate through the intricacies to help you take advantage of deductions and credits. You might not be aware of some of these strategies. This expertise can lead to significant savings on your tax bill.

Tax professionals are also skilled at identifying deductions that apply to your unique financial situation. They can help you maximize deductions, such as those related to investments, business expenses, or homeownership, which can ultimately lower your taxable income.

Filing taxes can be error-prone, and mistakes can lead to audits or penalties. Tax professionals have a keen eye for detail and can ensure that your tax return is accurate and compliant with current tax laws, reducing the risk of costly errors.

But don’t rely on the tax professionals just when it’s time to file your tax forms. They can assist in tax planning throughout the year, not just during tax season. They can also help you make financial decisions that minimize your tax liability, such as when to sell investments, how to structure business transactions, or when to contribute to retirement accounts.

Overall, handling taxes can be time-consuming and stressful. Hiring a tax professional frees you from this burden, allowing you to focus on your core activities. It also ensures that you meet all tax deadlines, avoiding potential penalties for late filing.

Please understand that every individual’s financial situation is unique. A tax professional can provide personalized advice and strategies tailored to your specific circumstances, ensuring that you’re taking advantage of every available opportunity to reduce your tax liability.

Stay up-to-date on crypto tax laws

Staying up-to-date on crypto tax laws means staying informed about the latest regulations and rules governing the taxation of cryptocurrencies.

This is crucial because cryptocurrency tax laws can change frequently, and being aware of these changes helps you stay compliant and make informed financial decisions.

While this effort might seem considerable, you need to be aware of the crypto tax law to be able to take advantage of deductions, credits, and strategies that can lower your tax liability, potentially saving you money. Knowledge of tax laws helps you make informed financial decisions related to cryptocurrencies, such as when to buy, sell, or hold, considering the tax implications of each action.

At the same time, being well-informed about tax laws provides peace of mind, knowing that you are acting within the legal framework and fulfilling your tax obligations.

Is it legal to use offshore accounts for crypto tax evasion?

Using offshore accounts for the purpose of crypto tax evasion is not legal and can have serious consequences.

Offshore banking itself is not illegal if it is done for legitimate reasons, such as diversifying investments, accessing foreign interest rates, or managing finances while living or working abroad. However, it becomes illegal when the intent is to evade taxes or engage in illicit activities.

Here’s why using offshore accounts for crypto tax evasion is not legal:

- Tax evasion: The primary reason for hiding assets or income offshore is often to evade taxes in one’s home country. This is illegal and can result in penalties, fines, and even criminal charges.

- Money laundering: Offshore accounts can be used for money laundering or other illicit financial activities. Concealing funds offshore can make it easier to engage in such activities, which are illegal and subject to prosecution.

- Reporting requirements: Many countries, including the United States, have reporting requirements for offshore accounts. Failure to report these accounts to tax authorities can lead to legal consequences.

- International agreements: International agreements like the Foreign Account Tax Compliance Act (FATCA) require banks worldwide to report foreign customers’ account information to their home country’s tax authorities, including the IRS.

- Declaration obligation: If you have an overseas bank account, you are generally obligated to declare its existence. And provide necessary information to tax authorities. Failure to do so can result in legal issues.

It’s essential to comply with tax laws and report cryptocurrency income accurately to avoid legal troubles.

How can I avoid tax on cryptocurrency?

To reduce or potentially avoid taxes on cryptocurrency, consider these strategies:

- Buy crypto in an IRA: Invest in cryptocurrency through a self-directed IRA, which can provide tax advantages depending on your chosen IRA type (traditional or Roth).

- Move to a country with no tax on crypto gains: If you have substantial crypto wealth, relocating to a new country that offers tax benefits like a 100% exemption on capital gains might help reduce your tax liability. However, this strategy is complex and requires proper consultation.

- Declare crypto as income: If you receive cryptocurrency as income for goods, services, mining, or staking, it’s treated as income and taxed at ordinary income rates. Keep records of received cryptocurrency and report it accurately.

- Hold for the long term: Avoid immediate taxes by holding onto your cryptocurrency for more than a year. This can qualify you for lower long-term capital gains tax rates.

- Offset gains with losses: Use tax-loss harvesting to offset crypto gains with losses.

- Sell during low-income years: Consider selling cryptocurrency in years when your taxable income is lower, as it can lead to lower tax rates on your gains.

- Donate to charity: Donating cryptocurrency to qualified charities can be tax-deductible, potentially reducing your overall tax liability.

- Gift to family: Gifting cryptocurrency to family members may help avoid taxation on your gains. There are gift tax limits, but this strategy can transfer wealth with potential tax advantages.

- Hold until inheritance: If you believe in the long-term value of cryptocurrency, holding it until your death can provide a step-up basis for your heirs, potentially allowing them to sell it without incurring income tax.

Remember that tax laws can change, and it’s crucial to consult a tax professional or financial advisor to develop a tax-efficient cryptocurrency strategy tailored to your specific situation.

How will you reduce your crypto tax liability?

Smart tax planning is essential to reducing crypto taxes and maximizing your returns. By leveraging cryptocurrency tax deductions, capital gains strategies, and crypto tax software, you can navigate the complex landscape of IRS guidelines for crypto taxes.

Whether you’re considering NFT tax considerations, crypto donation deductions, or offshore tax implications, staying compliant with crypto taxes is crucial. Consulting with a financial advisor or tax professional can help you devise a tailored investment strategy that minimizes your crypto tax liability. With the right knowledge and tools, you can reduce crypto tax and make the most of your digital assets.