The euro is one of the world’s most renowned and stable fiat currencies, competing only with the US dollar if at all.

In 2020, France and other EU countries are preparing to take the union’s dominance one step further by introducing a CBDC version of the euro.

Used by 19 different countries in the Eurozone, the euro is incredibly resistant to geopolitical issues at a macro level. Instead, its value is often tied to the strength of the entire European economy and the debt levels of individual countries.

In turbulent times, investors flock to the U.S. dollar instead of the euro due to the greenback’s perceived stability.

Over the past five years, euro strength has remained roughly the same when compared with the U.S. dollar. Its strength notably benefits other countries outside the E.U. Certain currencies such as the African CFA franc have their prices pegged to the euro.

Central banks throughout Europe are looking to exploit the euro’s stability by embracing the merits of digital currency technology. To understand this in greater detail, let’s explore how the E.U. is preparing for a crypto-enabled future.

France’s First Foray Into Digital Currency Technology

In April, the Bank of France invited applications from all over Europe for central bank-issued crypto solutions. While these projects would not be used for real-world CBDC implementations, the central bank said that it was looking to better understand the risks and opportunities associated with the underlying technology.

In its follow up document, the bank explained that it was looking for innovative solutions that tackled common challenges related to security and performance, regardless of the underlying technology. Ultimately, this meant it gave applicants the flexibility to work outside the constraints of blockchain technology.

Since then, the French central bank has already conducted tests on blockchain-based CBDC implementations. In May 2020, it partnered with French investment bank Société Générale (SocGen) for a limited trial involving the issuance of security tokens.

As part of the experiment, Societe Generale issued bonds to the tune of €40 million. The payment was settled in ‘digital euro form’ (i.e. CBDC), issued by the Bank of France. SocGen said that the collaboration highlighted the feasibility of using blockchain-based assets for wholesale, inter-bank settlements.

With the inclusion of smart contracts, the cost and time savings could motivate financial institutions to adopt the technology in the near future. The test also presents a key distinction between the CBDCs proposed by France and other countries.

While most state-backed digital currencies are meant for use by individual citizens, France has mostly focused on wholesale use. In other words, the country wants to bring tokens to banks and financial institutions before it considers rolling out a retail-based solution.

No other public tests have been conducted yet, and the Bank of France is expected to shortlist as many as ten applicants by July 10, 2020. The selection will largely be based on the ‘innovative’ merit of each application.

CBDC Efforts Elsewhere in the EU

Interestingly, France is not the only country in the European Union, advocating for a Central Bank Digital Currency. The Netherlands, Germany, and Sweden are among the few member nations that have spoken favorably about state-backed digital currencies of late.

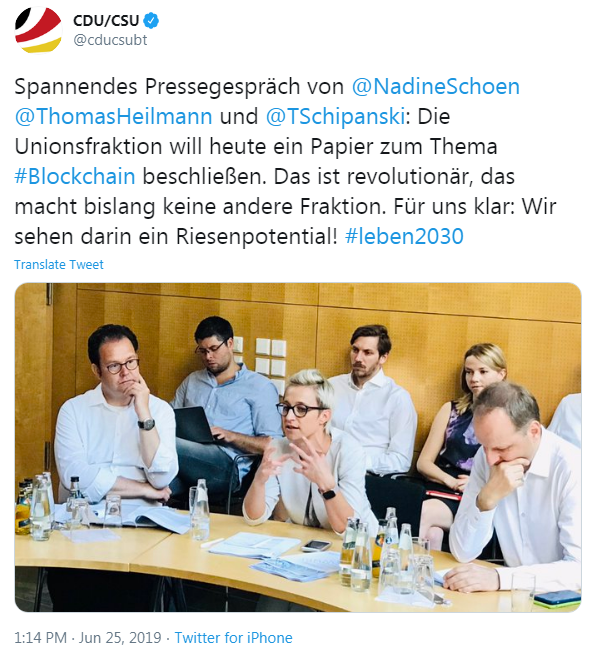

To the surprise of many, the CDU and CSU Unions in Germany recently spoke out in favor of implementing blockchain technology at all levels of government. In its announcement, the political duo also proposed an ‘e-Euro.’ The CBDC that would digitize a small portion of the existing euro supply and:

“make it accessible to a global infrastructure.”

The Union went on to explain that the central bank-issued token would not replace existing fiat currency. This would prevent the institution of a parallel economy and allow authorities to monitor each unit of the currency.

Furthermore, they could freeze e-Euro tokens involved in any criminal activity and confiscate them if necessary. It also pitched the e-Euro as a disruptor in the cross-border payment ecosystem. Decentralized cryptocurrencies already settle international transactions in a timely and cost-efficient manner, particularly when compared with traditional alternatives such as SWIFT.

The EUROchain Experiment and Controversy

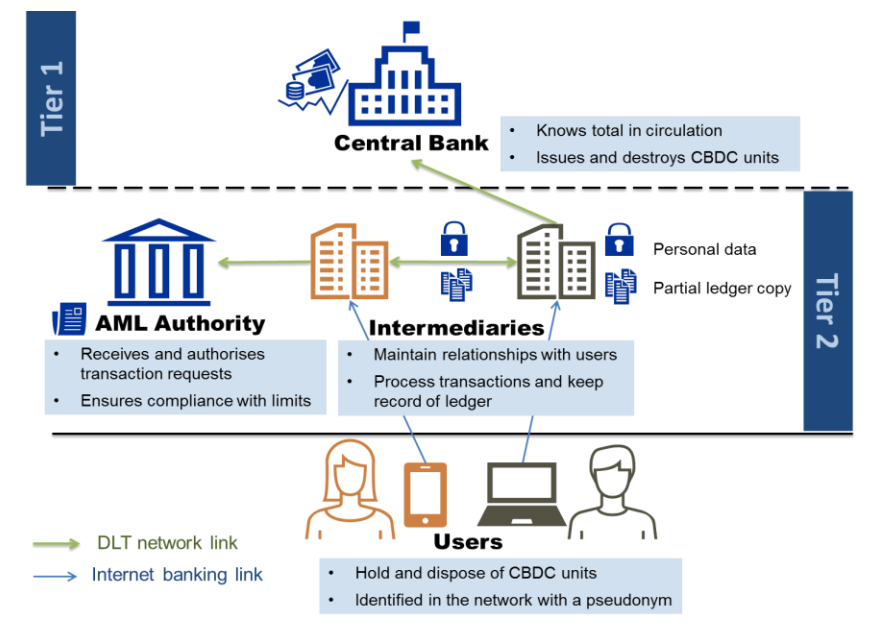

Towards the end of 2019, Christine Lagarde, President of the European Central Bank (ECB), announced the creation of a task force dedicated to CBDCs. After committing to accelerate its development, the ECB published a research paper outlining anonymity in blockchain-based digital currencies.

Unlike decentralized alternatives like Bitcoin, CBDCs will likely require users to maintain a digital identity to stay compliant with anti-money laundering (AML) regulations. However, these identities may be linked to purchasing and shopping behavior, compromising privacy.

To combat this, ECB researchers explained that they could use blockchain tech to issue single-use, low denomination vouchers intended for anonymous use. The researchers theorized they could build a blockchain-based payment system with ‘cash-like features’ dubbed EUROchain.

Where EUROchain Fell Short

EUROchain critics quickly pointed out that the blockchain and resulting tokens would be highly centralized, neutralizing most of the advantages afforded by the technology. Under the research assumptions, the ECB would be the sole controller of EUROchain. It could dictate its own terms on issuance, supply, and even wallet generation.

This leaves no scope for peer-to-peer transactions, requiring all funds to go through a trusted intermediary such as a bank. Furthermore, the system borrows heavily from Bitcoin’s UTXO model, which is not capable of providing complete anonymity.

Nevertheless, EUROchain represents a major stepping stone for central bank-issued digital currencies in Europe. The ECB will likely need to devote several years of iteration and R&D before it finally settles on a mass-market solution.

The paper’s authors also emphasize this fact, stating that EUROchain is only intended to serve as a proof-of-concept implementation. It’s entirely possible that privacy will still be an afterthought for the ECB’s planned token.

In such a scenario, privacy vouchers are better than having no recourse at all. During her address last year, the ECB President noted that the main advantages of a CBDC would be cost reduction, elimination of intermediaries, and financial inclusion.

With digital currencies offering these features and others such as automated contracts and programmability, the loss of privacy is often overlooked by governments and users alike. This is an unfortunate reality that many CBDC users around the world will have to grapple with. Thankfully, decentralized solutions like Zcash and Monero will always be available for those that prefer private transactions.

Why European Central Banks Are Pushing for a CBDC

Ever since Facebook announced its Libra project, governments around the world have started to pay more attention to the cryptocurrency ecosystem. Over the years, Facebook has garnered its fair share of criticism. This ranges from regulatory pushback to breaches of privacy and lapses in security.

Now that the social media giant has entered the financial domain, many nations realize the need for a competing solution. Federal Reserve Chairman Jerome Powell has warned that Libra could lead to global financial instability.

To that end, governments are stepping up their efforts to design and launch their own CBDCs before the private sector takes control of the market. The European market is no different. Most countries are accelerating their research into CBDCs.

In 2019, Governor of the French Central Bank, François Villeroy de Galhau, spoke about this issue at length. He explained:

“The creation of a central bank digital currency … is neither a precondition for nor a guarantee of more efficient payments. However, we as central banks must and want to take up this call for innovation at a time when private initiatives – especially payments between financial players – and technologies are accelerating, and public and political demand is increasing. Other countries have paved the way; it is now up to us to play our part, both ambitiously and methodically.”

Digital Currencies in a Cashless World

Private tokens are not the only threat governments have to contend with. Worldwide, physical cash is rapidly going out of fashion. While banknotes are currently still legal tender, companies like PayPal in the West and WeChat in the East are becoming commonplace.

This is especially true in certain countries like China and Sweden, where the overwhelming majority of transactions are cashless. In fact, cash usage has declined so significantly that the Chinese central bank had to warn businesses against refusing cash payments.

For central banks, a completely cashless society could lead to a public losing faith in its financial institutions. If money becomes synonymous with names such as Libra, PayPal, and Stripe, the central bank’s perceived importance diminishes.

With its members dead-set on making CBDCs a reality, it’s likely that the European Union will come up with a ‘digital euro’ solution sooner rather than later. However, given the euro’s renown and credibility, the ECB must tread carefully. Any missteps could negatively affect its prized fiat currency.

Do you think European central banks will adequately address the complex issues surrounding future CBDC design?