Blockchain technology has emerged as a revolutionary technology, offering a distributed and immutable ledger for tracking transactions across the internet. The pressing question remains: what tangible value does blockchain bring to the real world? Innovative technologies can usher in transformative changes, some of which are immediately evident, like cryptocurrencies and generative AI. Other promising changes require time to gain widespread adoption. This article delves into real-world asset (RWA) tokenization, its advantages, potential hurdles, and the implications it may bring to the financial landscape.

- What is tokenization?

- What are Real Estate Investment Trusts (REITs)

- Real-world asset tokenization

- Some words of caution around tokenization and RWAs

- Real estate tokenization projects in Singapore and Korea

- Transaction of RWAs

- RWA tokenization will be transformative

- Frequently asked questions

- About the author

What is tokenization?

Tokenization involves the conversion of indivisible and often illiquid physical or virtual assets into digital units (tokens) that can be bought, sold, and transferred using blockchain technology. The tokenization of RWAs is a good example of blockchain technology addressing real-world issues by making RWAs more accessible, liquid, and efficient.

While the concept of tokenization applies to various types of assets, let’s begin by considering a more concrete application – Real Estate Assets (REAs).

What are Real Estate Investment Trusts (REITs)

Real estate investment has long been popular for investors seeking capital appreciation and a stable income stream through rental earnings.

To better understand the tokenization of REAs, let us start with a more familiar concept of Real Estate Investment Trusts or REITs. By investing in shares of a specific REIT, individuals can gain exposure to income-generating real estate assets without the burden of owning the physical properties themselves. This brings better liquidity to a class of illiquid assets (i.e., real estate properties). REITs also enable an investor to better manage risks through exposure to multiple properties and/or types of properties (e.g., residential, commercial, and industrial properties).

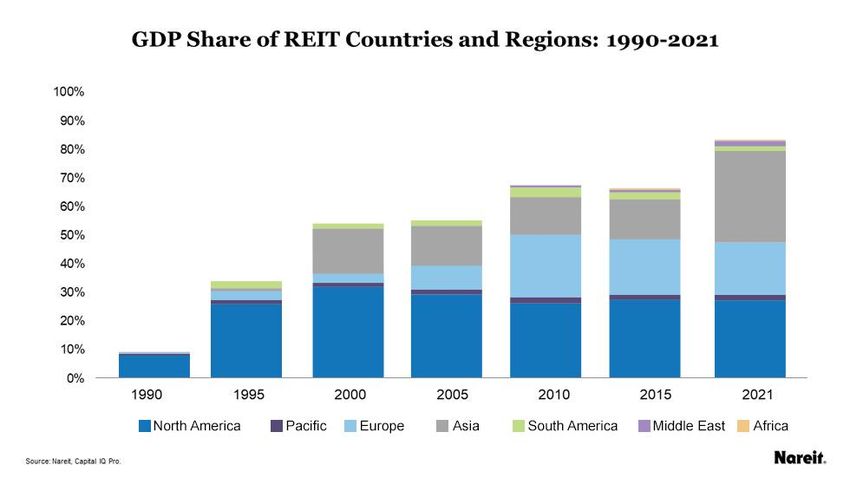

Real estate is a huge sector full of investment opportunities. According to the Statista Research Department, North America’s listed real estate market boasts a staggering value of USD 1.3 trillion, with the largest global REIT commanding a market capitalization of USD 117.2 billion. Although North America dominates the REIT market, the Asia Pacific region is witnessing a notable surge in momentum. Nareit data indicates that North America represents 57% of global market capitalization, with Asia Pacific at 25% and Europe, the Middle East, and Africa (EMEA) at 18%.

Traditionally, the Asia Pacific region has seen robust REIT markets in countries like Australia, Singapore, and Japan. Notably, Indonesia has had REIT regulations in place since 2007. However, the market has been slow to gain momentum due to high transaction taxes incurred by sponsors when adding assets to REITs.

Real-world asset tokenization

REITs and the tokenization of real estate represent two distinct approaches to real estate investment, each with its own characteristics, advantages, and challenges. The following points are essential to note:

1. REITs are companies that own, manage, or finance income-generating real estate. When you invest in a REIT, you are essentially acquiring shares in the company, which holds a diverse portfolio of properties. In contrast, tokenization entails the transformation of ownership of a real estate asset into digital tokens recorded on a blockchain. Investors participating in tokenized real estate directly possess a fractional stake in the underlying asset.

2. Publicly traded REITs offer better liquidity of real estate properties since the shares of the REIT can be readily bought and sold on established stock exchanges. In the case of tokenized real estate, enhanced liquidity is possible, contingent upon the presence of a well-functioning secondary market for trading these tokens.

3. The manner in which capital gains are realized upon divesting real estate varies for REIT investors and tokenization investors. REIT investors who do not have direct ownership of the properties generally do not partake in the direct capital gains generated from property sales. Conversely, tokenization investors, being fractional owners of the real estate, have the potential to benefit from capital gains.

4. REITs are subject to specific laws and regulations that vary across jurisdictions. In contrast, the regulatory framework for tokenized real estate is still evolving, with varying requirements in different jurisdictions regarding real estate ownership.

Some words of caution around tokenization and RWAs

Singapore has been a trailblazer in embracing blockchain and fintech innovation, including real estate tokenization. The regulatory environment in Singapore is conducive to blockchain and cryptocurrencies, fostering experimentation and growth in the field. Companies have been exploring the creation of platforms to facilitate the tokenization of real estate assets, offering investors opportunities to invest in specific properties or portfolios.

Some real estate tokens are considered security tokens and are regulated under the Securities and Futures Act. Firms offering such security tokens require a Capital Markets Services (CMS) license from the Monetary Authority of Singapore (MAS). Therefore, one should check if the tokenization platform we are investing through is properly licensed to offer such services.

Token holders should exercise caution and be aware if the token represents fractional ownership of the underlying real estate properties. If so, they should ensure to check their eligibility as fractional owners of the real estate within a particular jurisdiction.

Investors should also check what digital exchanges the tokens are listed in and assess if there is good token liquidity.

Real estate tokenization projects in Singapore and Korea

The tokenization of REAs has gained traction worldwide, including in countries like Singapore and Korea. Here are two examples, one from each country:

In the Singaporean market, Fraxtor is one of the more established players. Fraxtor is a MAS-regulated real estate investment platform that offers investment opportunities in bite-sized amounts for as little as $20,000.

South Korea’s government took an innovative step by introducing a regulatory sandbox called the Financial Regulatory Sandbox to test-bed fintech-based products. Among the pioneers in this space is Kasa, which also holds a MAS license to offer its services in Singapore. Kasa is a platform for tokenizing real estate securities, with investment options starting from $20,000. Kasa reported that investors exited their first asset in Gangnam with a profit rate of 26% before taxes and fees.

Transaction of RWAs

Let us now explore the broader realm of RWAs. Tokenized assets offer broader market participation and liquidity, especially in the presence of a secondary market for trading such tokens. Such tokenized RWAs should always be offered on highly stable and trustworthy blockchain platforms with reasonable gas fees to foster lower transaction costs and more efficient market dynamics. There are some exciting developments in this field.

Case study: Elysia

As an example, Elysia is a global real-world asset tokenization project that leverages blockchain to provide innovative financial services. Elysia tokenizes various RWAs — including residential and commercial real estate — as well as the ability to invest crypto assets in financial derivative products like accounts receivables and U.S. Treasury bonds. Elysia operates the DeFi platform Elyfi, promoting liquidity for RWAs and building a decentralized financial ecosystem based on RWAs on Ethereum, BSC, and the Klaytn network, a layer-1 public blockchain mainnet developed by Kakao. Klaytn’s low gas fees further reduce barriers to entry, allowing even small-scale investors to participate.

Tokenizing commodities such as gold

Up to this point, we’ve primarily discussed tokenization as an effective means to fractionalize substantial investment opportunities, making them accessible to a broader spectrum of investors. Tokenizing real-world assets (RWAs) can also extend to commodities, including precious metals like gold. Given the substantial cost of gold, we can link one token or coin to a specific quantity of gold, such as one token equating to one gram of gold. The gold will be held in reserve, typically by a third party.

Gold-pegged digital currencies offer a unique advantage: they establish a stable minimum token value, one that can potentially surpass the actual value of gold if the digital currency gains widespread popularity. This dynamic safeguards against any potential decrease in the value of the digital currency, further enhancing its appeal and stability.

Consider the Gold Pegged Coin ($GPC) as an illustrative example. Similar to Paxos Gold ($PAXG) and Tether Gold ($XAUt) on the Ethereum chain, $GPC represents a tokenized form of physical gold, fully backed by the Korea Gold Exchange, the largest gold exchange in South Korea. As the newest entrant to the tokenized gold market, $GPC further innovates on tokenized gold by making its debut on Klayswap, the largest decentralized exchange (DEX) within the Klaytn ecosystem.

In doing so, $GPC allows users to integrate gold into their investment portfolios seamlessly. Further, it empowers them to earn returns on their gold holdings through the DeFi ecosystem and swiftly and economically swap between their cryptocurrency holdings. These might also encompass synthetic tokenized equities, thus enabling them to capitalize on various market opportunities.

RWA tokenization will be transformative

The tokenization of RWAs is here already. Fractional real estate investing shares similarities with the established REIT market. Both require careful scrutiny of assets and structuring investments within prevailing regulations. The rise of fractional ownership of real estate, financial derivative products like accounts receivables and U.S. Treasury bonds, and gold-backed digital currencies connects the virtual world to real-world assets. This makes big-ticket RWAs more accessible, liquid, and efficient.

The digital tokenization of RWAs appears poised to reshape the landscape of capital markets in the long term. It welcomes more retail investors into a sphere that was previously the domain of institutional investors and ultra-high-net-worth individuals.

Frequently asked questions

How will the tokenization of RWAs affect the financial landscape

How does tokenized real estate differ from REITs?

What is the advantage of tokenizing gold?

What is the social impact of RWA tokenization?

About the author

Khoong Hock Yun is a managing partner (Blockchain Fund 1 and 2) at Tembusu Partners and a Board Member of the Klaytn Foundation.

He was the Chief Digital Evangelist and Assistant Chief Executive Officer (Development) at the Infocomm Media Development Authority (IMDA) of Singapore, where he was responsible for all Infocomm Communications Technology (ICT) development activities in industry, infrastructure, and manpower as well as Singapore’s adoption and use of ICT. Under Khoong Hock Yun’s tenure, Singapore grew strongly as Asia’s leading dynamic and vibrant ICT hub with ICT industrial revenue growth from S$20B in 2000 to $70B in 2015. Before IDA/IMDA, Mr. Khoong managed a global business in Mentor Graphics Corporation (USA). He is a Harvard Business School alumnus.