Blockchain’s integration into real-world asset (RWA) management is reshaping the way we exchange value. However, regulatory bodies worldwide have strict requirements for managing RWAs and securities. But how do we enforce these guidelines while operating on a public blockchain infrastructure? The implementation of ERC3643 solves this problem.

KEY TAKEAWAYS

➤ ERC3643 enables compliant tokenization of real-world assets by enforcing regulatory rules through smart contracts.

➤ It offers over 120 functions, supporting lifecycle management, automated compliance, and post-issuance operations.

➤ ERC3643 unlocks liquidity for real-world assets on public blockchain networks by integrating verifiable identities and compliance.

What is ERC3643?

ERC3643 is a token standard designed for managing regulated assets on the blockchain, particularly real-world Assets (RWA) and securities.

It combines the flexibility of blockchain with compliance features, which allows issuers to enforce regulatory requirements directly within token smart contracts.

Unlike traditional tokens, ERC3643 enables control over who can hold or transfer tokens to ensure adherence to legal frameworks. This makes it ideal for industries that require strict compliance, such as finance and real estate, while still benefiting from the decentralized nature of public blockchains.

Complexities in private markets

Traditionally, investors in the private sector face significant challenges in addressing liquidity and finding markets for private investments. Despite the potential for higher returns, illiquid investments can be problematic without active markets or willing buyers.

The main reason for this issue is the outdated and fragmented infrastructure of the current framework. Due to this limited infrastructure, buying and selling private assets becomes inefficient.

This leads to significant liquidity discounts and sometimes even the avoidance of transactions.

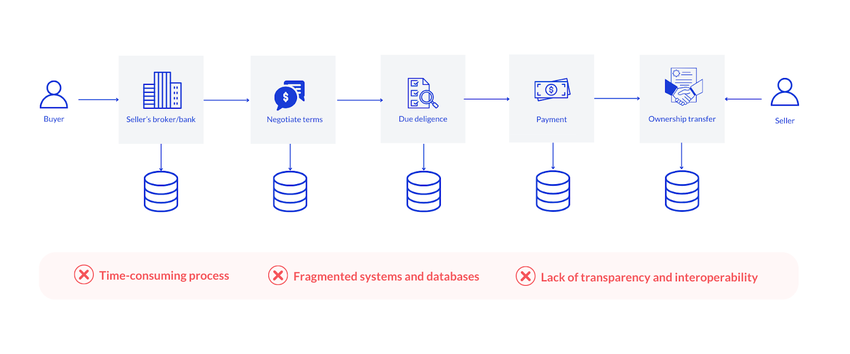

Whether you own real estate, a limited partner (LP) interest in a fund, or a stake in a private company, sellers must undertake arduous steps to find willing buyers.

The process includes:

- Sourcing a buyer: Using personal networks, word of mouth, or working with intermediaries such as broker-dealers or investment banks.

- Negotiating terms of the sale: Involves several rounds of discussions and revisions before both parties agree on the terms.

- Conducting due diligence: Requires reviewing financial statements, legal documents, contracts, and other records, as well as verifying the buyer’s eligibility. This process often involves sharing documents via mail, emails, and sometimes even fax.

- Transfer of ownership: The final step where ownership of the asset or security changes hands. In many cases, ownership records are maintained in spreadsheets. In other cases, a clearing process requires custodians of buyers and sellers to ensure payment has arrived before transferring ownership.

The duration of private market transactions can be prolonged, often spanning from several weeks to several months, and in some cases, even years. It is a high-cost and time-consuming process that can improve with the help of blockchain technology.

The good news is that every fragmented market presents room for innovation and disruption, which is where blockchain comes into play. A suitable blockchain standard must be specifically designed with smart contracts to meet regulatory needs and unlock the vast value of these assets.

When conducting these activities on a blockchain-based system, many of the previously mentioned steps are achieved in a much faster and more efficient manner.

How ERC3643 makes a difference

ERC3643 not only addresses regulatory compliance but also enhances various aspects of the transaction process for real-world assets on the blockchain. It streamlines operations and opens up new opportunities for asset holders and investors. Here are the key ways in which ERC3643 improves traditional procedures:

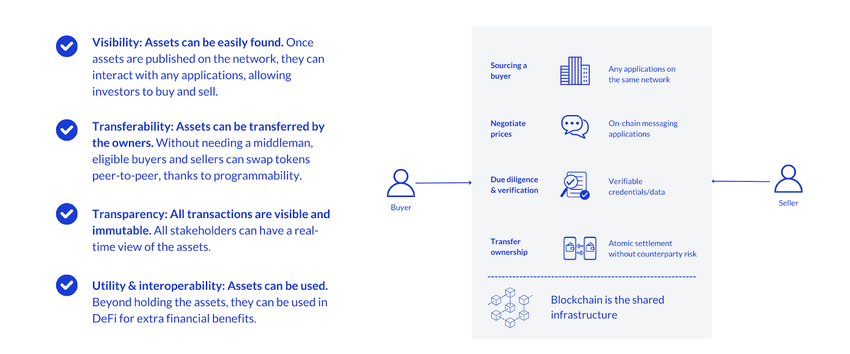

1. Sourcing a buyer

Once assets are published on the blockchain network, they become available to interact with any applications on the same network. This allows asset holders direct access to a vastly larger pool of potential counterparties.

Assets could be listed on multiple marketplaces, including centralized exchanges, decentralized exchanges, or used for staking and collateralized loans.

2. Negotiating terms of the sale

Market supply and demand influence negotiation on trading platforms. Investors seek counterparties and streamline the process by avoiding individual buyer negotiations.

For peer-to-peer trading, on-chain or off-chain negotiations can take place to reach an agreement.

3. Conducting due diligence

Smart contracts can embed a verifiable due diligence certificate into the tokens. Additionally, they can verify counterparties’ eligibility directly through verifiable credentials. This streamlines the entire process, improving efficiency while ensuring compliance.

4. Transfer of ownership

When using tokens as a payment method (stablecoins, tokenized cash, or crypto), the transfer or swap is instant and free of counterparty risk.

The ERC3643 smart contract ensures transfers happen only when both investor and offering rules are satisfied, which enables peer-to-peer transfers — a feature that wasn’t possible in the traditional financial system.

How RWA tokenization works

Compliance is crucial since tokenized RWAs are securities. In most jurisdictions, RWAs must be owned by an investment vehicle, and investors will invest in financial products that this vehicle structures, such as shares or debt.

These financial products are securities that require enforced compliance based on existing regulations.

This means that only certain investors can become asset owners (e.g., KYC-verified European citizens). In Europe, the MiCA regulation clearly defines security tokens as securities, necessitating adherence to MiFID, the existing securities regulations.

Comparing and contrasting the major token standards

A “standard” refers to a predefined set of rules or guidelines tailored for a specific purpose. Standards ensure consistency and uniformity, thus making it possible for diverse applications and assets to interact smoothly.

However, standards can bring certain limitations when trying to utilize them for a specific purpose or use case.

For RWAs, a standard is needed that can potentially deal with various jurisdictional securities laws for multiple parties, all automatically executable on-chain. That is no easy task.

Now that we understand what a standard is, let’s break down some commonly utilized standards like ERC20 and ERC721.

ERC20:

ERC20 is a permissionless token standard, widely used for creating fungible tokens on the Ethereum blockchain or any EVM-compatible blockchain.

It defines simple rules for tokens that are identical in type and value, thereby enabling easy exchange on trading platforms and other functions.

Key aspects:

- Fungibility: ERC20 tokens are interchangeable.

- Interoperability: Any ERC20 token can work on any platform that supports this standard.

Common examples:

- Tokens: WETH, BAT, USDC

- Exchanges: Uniswap, Sushiswap (compatible with all ERC20 tokens)

- DeFi Governance Tokens: Aave, Compound

ERC721:

What is it?

ERC721 is a token standard for non-fungible tokens (NFTs), meaning each token is unique and represents ownership of a specific digital asset. This makes ERC721 ideal for applications like collectibles and other items requiring distinct representation.

Key aspects:

- Uniqueness: Every ERC721 token is unique and non-interchangeable.

- Use Cases: Primarily used in NFTs for digital ownership and collectibles.

Common examples:

- NFTs: Bored Apes, Cryptopunks

- Marketplaces: Opensea, LooksRare

Important to understand: ERC721 is the specific standard utilized for innately unique assets on any EVM-compatible blockchain.

ERC3643

ERC3643 is a permissioned token standard designed for securities tokenization, Web3 loyalty programs, and digital payment systems. It allows issuers to track token ownership, enforce compliance, and manage the token’s lifecycle with over 120 built-in functions. This standard ensures compliance with regulatory requirements for tokenizing Real-World Assets (RWAs).

Key aspects:

- Compliance: Ensures transfers meet KYC/AML and other regulatory rules.

- Lifecycle Management: Includes advanced features for post-issuance operations, such as blocking or recovering tokens.

Common examples:

- Validator: Tokeny

- Use Cases: Securities tokenization, regulated digital assets

ERC20 vs. ERC721 vs. ERC3643 in a nutshell

Here’s a copyable table summarizing the differences between ERC20, ERC721, and ERC3643:

| Standard | ERC20 | ERC721 | ERC3643 |

|---|---|---|---|

| Type | Fungible tokens | Non-fungible tokens (NFTs) | Permissioned tokens for regulated assets |

| Transferability | Permissionless, transferable to anyone | Unique, transferable to anyone | Restricted, transfers only to verified investors |

| Use cases | Cryptocurrencies, DeFi tokens | Collectibles, digital assets | Securities, RWAs, digital payment systems |

| Compliance | No compliance features | No compliance features | Enforces KYC/AML and regulatory checks |

| Functionality | Simple rules for token transfers | Unique ownership representation | 120+ functions for lifecycle management |

| Key examples | WETH, USDC, Aave | Bored Apes, Cryptopunks | Tokeny, ONCHAINID integration |

Verifiable on-chain digital IDs and ERC3643

What is ONCHAINID?

ONCHAINID is an open-source self-sovereign identity smart contract that allows tokens and applications to verify individuals and organizations.

It enforces automated compliance and enables access to digital assets on-chain, without intermediaries.

How does ERC3643 use ONCHAINID?

- ERC3643 tokens verify user eligibility based on preset rules.

- Tokens link ownership to users’ ONCHAINID instead of wallet addresses.

- Issuers decide which identifiers (e.g., KYC providers) verify credentials.

Verification process:

- A KYC provider verifies off-chain documents.

- A hashed/anonymous credential is issued as proof of eligibility.

- ERC3643 tokens verify on-chain credentials to determine permissions.

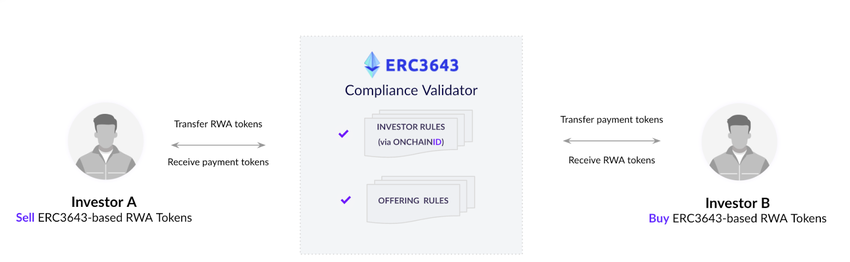

Example scenarios

Investor-A: Completed KYC/AML and invested in security X.

Investor-B: Same as Investor A.

Investor–C: Has a self-custody wallet but hasn’t completed onboarding.

- Scenario 1: Investor A attempts to sell to Investor C. The transaction is declined because Investor C isn’t verified.

- Scenario 2: Investor A sells to Investor B. The transaction is authorized, as both meet the smart contract’s rules.

Interoperable securities unlock liquidity

When RWA tokens function like any ERC20 token while complying with regulations, they can enable global distribution, peer-to-peer transfers, and participation in DeFi. This unlocks liquidity for RWAs, promoting financial inclusion and allowing assets to earn extra yields or be used for borrowing.

ERC3643 and the future of blockchain

Overall, ERC3643 is promising to revolutionize blockchain tech by integrating compliance and security into RWA tokenization. It opens access to global markets by enabling peer-to-peer transactions while enforcing regulatory rules through smart contracts and digital identities. This approach ensures investors can confidently manage assets within a secure, compliant framework, which further advances blockchain’s role in the global financial system.

Frequently asked questions

What are real-world assets (RWA) in the context of blockchain?

How does ERC3643 differ from other Ethereum standards like ERC20 or ERC721?

Why is regulatory compliance so important in the context of tokenizing RWA?

What is ONCHAINID and how does it fit into the ERC3643 standard?

How do digital identities protect user privacy while ensuring compliance?

About the author

Joachim Lebrun is the Head of Blockchain at Tokeny, a leading tokenization platform backed by Euronext. The company has tokenized $28B in assets over the past six years. He is also the creator of ERC3643 and the chairman of the technical working group at ERC3643 Association, helping developers implement ERC3643 easily with the necessary tools.