Satoshi Nakamoto famously quoted the Times in the genesis block of Bitcoin. The message showed that the government was on the brink of a second bank bailout early in January 2009.

Nakamoto’s analysis had shown him that central bank meddling would leave entire nations without a trustworthy currency. Extensive ‘bailouts’ that massively increased federal balance sheets were, by Nakamoto’s standards, untenable.

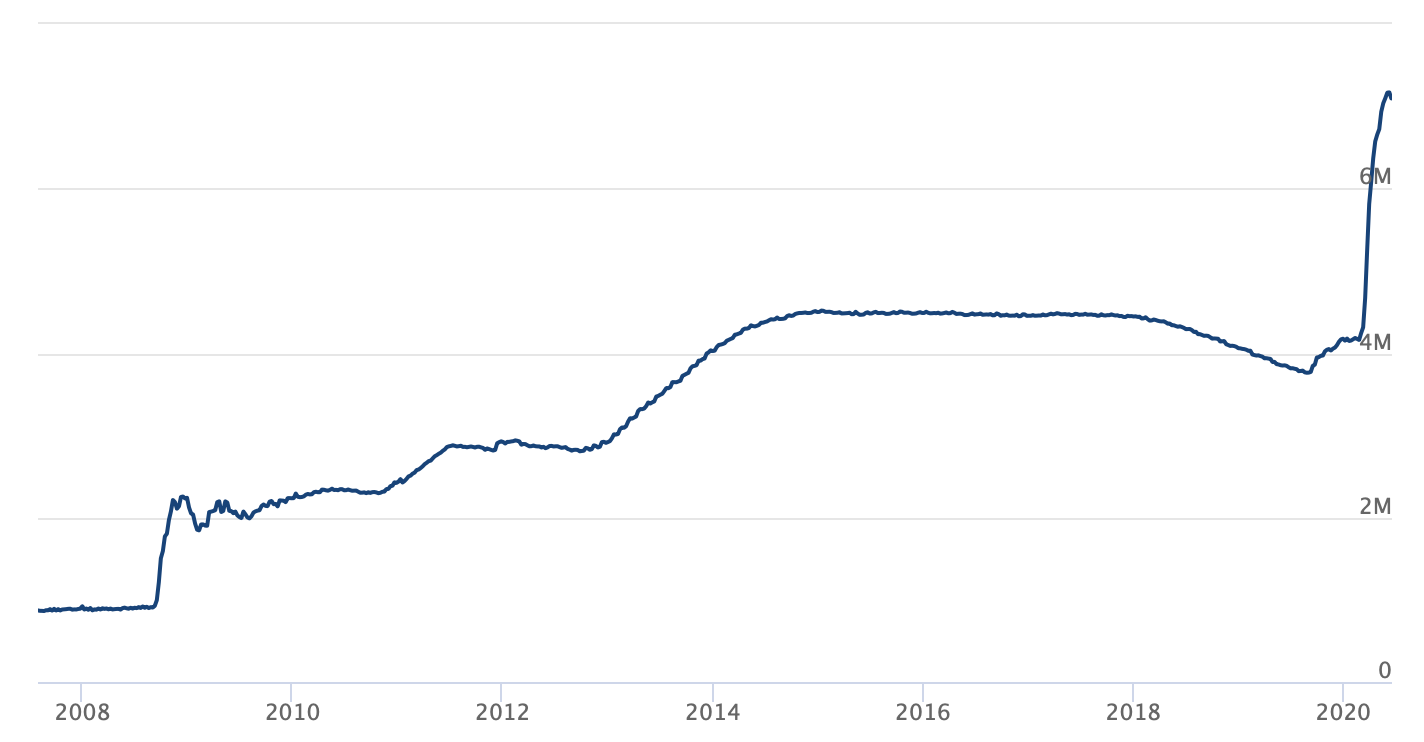

2008 and the Rise of QE

The change in policy was most keenly felt immediately after the financial crisis that shook the world in 2008. Caused by overconfidence in the stability of mortgage-backed securities, banks found themselves overextended on assets that suddenly became worthless. In a matter of days, banks that were once paragons of financial stability were closed. Others saw their balance sheets collapse. National governments feared a run on these banks. In the wake of the crisis, President George W. Bush signed the Emergency Economic Stabilization Act (EESA), with the full approval of Treasury Secretary Henry Paulson. The primary goal of the $700 billion bailout was to take the bad assets out of the balance sheets of the banks. This move protected their bottom line but shifted the burden of debt service into the lap of the Federal Reserve. This purchasing of assets to expand available funds is known as quantitative easing (QE). QE provides a way for the Fed to actively increase monetary supply in the economy. Before this bill, the vast majority of Fed activity was passive, focusing mainly on interest rate changes. The EESA began a balance sheet expansion that has continued to this day. The crisis caused the Fed to increase its asset purchases from $870 billion to $4.5 trillion. The FOMC’s balance sheet normalization program between October 2017 and August 2019 did, however, temporarily trim assets down to under $3.8 trillion.

A New Normal

This QE practice has continued from 2008 until the present day. During this time, the economy has continued to expand at unprecedented rates. Before the COVID-19 crisis, the vast majority of indices were at all-time highs. Some economists argued that the economic growth was nowhere near related to fundamental economic expansion as it was to the extremely cheap money supply. These analysts saw the economic growth as effectively hollow due to increased government debt. Even during the decade of growth following the crisis, the Fed balance sheet ballooned from $2.2 trillion to $4.5 trillion. While the increases were touted as necessary for continued growth, the overall movement of the economy now appears to be driven by this new QE standard.Crisis, Collapse, and Collateral

The COVID-19 crisis hit markets like a freight train in early 2020. As news of the virus spread and global governments debated how to best respond, the stock market wobbled in anticipation. After several hasty judgments regarding the severity of the virus had been shelved, the U.S. government decided to follow its global counterparts. Everything except essential services was shut down, and the economy ground to a halt. Almost immediately, unemployment exploded, as businesses, now unable to operate, were forced to furlough employees. Additionally, many companies were utterly incapable of continuing their business activities. The DJIA went from nearly 30,000 at the end of February to 18,000 by March 23 – a drop of almost 50%. The collapse kicked off what most saw as an inevitable recession. However, as the crisis worsened, the Trump administration followed the example of the previous crisis and proposed a massive liquidity increase. The need was primarily due to the fact that, according to Fed estimates, nearly 40% of Americans could not cover a one-time $400 crisis.

Treasury Secretary Steven Mnuchin, Fed chair Jerome Powell, and both houses of Congress pushed and passed a $2 trillion stimulus package. The bill pressed funds into nearly every corner of the economy, from individuals to small business, and banks.

This bill took the Fed balance sheet into orbit, with funds moving from just over $4 trillion to well over $7 trillion in a matter of days. Many saw the actions as necessary to protect American well-being. Others, though, saw the payout as an act of political collateral during an election year.

However, as the crisis worsened, the Trump administration followed the example of the previous crisis and proposed a massive liquidity increase. The need was primarily due to the fact that, according to Fed estimates, nearly 40% of Americans could not cover a one-time $400 crisis.

Treasury Secretary Steven Mnuchin, Fed chair Jerome Powell, and both houses of Congress pushed and passed a $2 trillion stimulus package. The bill pressed funds into nearly every corner of the economy, from individuals to small business, and banks.

This bill took the Fed balance sheet into orbit, with funds moving from just over $4 trillion to well over $7 trillion in a matter of days. Many saw the actions as necessary to protect American well-being. Others, though, saw the payout as an act of political collateral during an election year.

Explosive Supply and Inflation

The overarching concern regarding the Fed’s balance sheet is not actually related to the debt, however. The Fed can hold the liability and could ostensibly begin reducing it. However, the funds that appear as debt on the Fed ledger are actually liquidity in the marketplace. More than $7 trillion dollars have entered the US economy in the last ten years, while US GDP only amounts to $20 trillion. More than one-third of the GDP has been effectively leveraged using the Fed. The danger of this policy is that these massive liquidity increases are addictive. Even Secretary Mnuchin has stated that the market is now addicted to stimulus. Stock price increases during times of absolute crisis reveal that the market is moving not based on fundamentals but based on free money. As investors drink the stimulus Kool-Aid, the concept of value becomes effectively meaningless. Nevertheless, real assets have real value and are therefore in grave danger of substantial inflationary pressure.No Change Coming

Nevertheless, despite the profound dangers, Fed Chair Jerome Powell has continued to urge Congress to stay the course. His statements this week included an appeal for continued fiscal support.“I do think it would be appropriate to think about continuing support for people who are newly out of work and for smaller businesses who are struggling. The economy is just now beginning to recover. It’s a critical phase and I think that support would be well-placed at this time.”While the longterm effects of the stimulus remain unknown, the policies reveal that Satoshi’s understanding of the crisis in 2009 was spot-on. The federal bailout program shows no signs of letting up anytime soon.

Disclaimer

In adherence to the Trust Project guidelines, BeInCrypto is committed to unbiased, transparent reporting. This news article aims to provide accurate, timely information. However, readers are advised to verify facts independently and consult with a professional before making any decisions based on this content. Please note that our Terms and Conditions, Privacy Policy, and Disclaimers have been updated.

Jon Buck

With a background in science and writing, Jon's cryptophile days started in 2011 when he first heard about Bitcoin. Since then he's been learning, investing, and writing about cryptocurrencies and blockchain technology for some of the biggest publications and ICOs in the industry. After a brief stint in India, he and his family live in southern CA.

With a background in science and writing, Jon's cryptophile days started in 2011 when he first heard about Bitcoin. Since then he's been learning, investing, and writing about cryptocurrencies and blockchain technology for some of the biggest publications and ICOs in the industry. After a brief stint in India, he and his family live in southern CA.

READ FULL BIO

Sponsored

Sponsored