In the digital finance sector, the discussion around Central Bank Digital Currencies (CBDCs) has taken center stage. Ashok Venkateswaran, Mastercard’s blockchain and digital assets lead for Asia-Pacific, recently voiced skepticism about the widespread adoption of CBDCs, especially in regions with robust payment systems, at the Singapore FinTech Festival.

His comments reflect a cautious approach to the adoption of these digital assets.

Mastercard Executive: CBDC Adoption a Complex Issue

Retail CBDCs, the digital counterparts of traditional fiat currencies, are designed to cater to the daily transactional needs of individuals and businesses. Wholesale CBDCs contrast this concept, as financial institutions intend them for high-value transactions.

Despite the International Monetary Fund’s (IMF) endorsement of CBDCs as a safe, low-cost alternative to cash, widespread adoption remains a complex issue.

“The difficult part is adoption. So if you have CBDCs in your wallet, you should have the ability for you to spend it anywhere you want – very similar to cash today.”

Read more: Digital Rupee (e-Rupee): A Comprehensive Guide to India’s CBDC

The IMF reports that about 60% of countries globally are exploring the concept of CBDCs. However, only 11 have fully adopted them. Venkateswaran highlights the significant time and effort required to build the necessary infrastructure for CBDCs despite many central banks becoming increasingly innovative and collaborating with private companies like Mastercard.

Venkateswaran also noted consumer preference for traditional forms of money like paper and coins. He also suggested that there isn’t enough justification for CBDCs in places where existing payment systems are efficient.

Citing Singapore as an example, he stated,

“There isn’t a reason for a retail CBDC [in Singapore] but there is a case for a wholesale CBDC for interbank settlements.”

A Balancing Act Between Privacy and Convenience

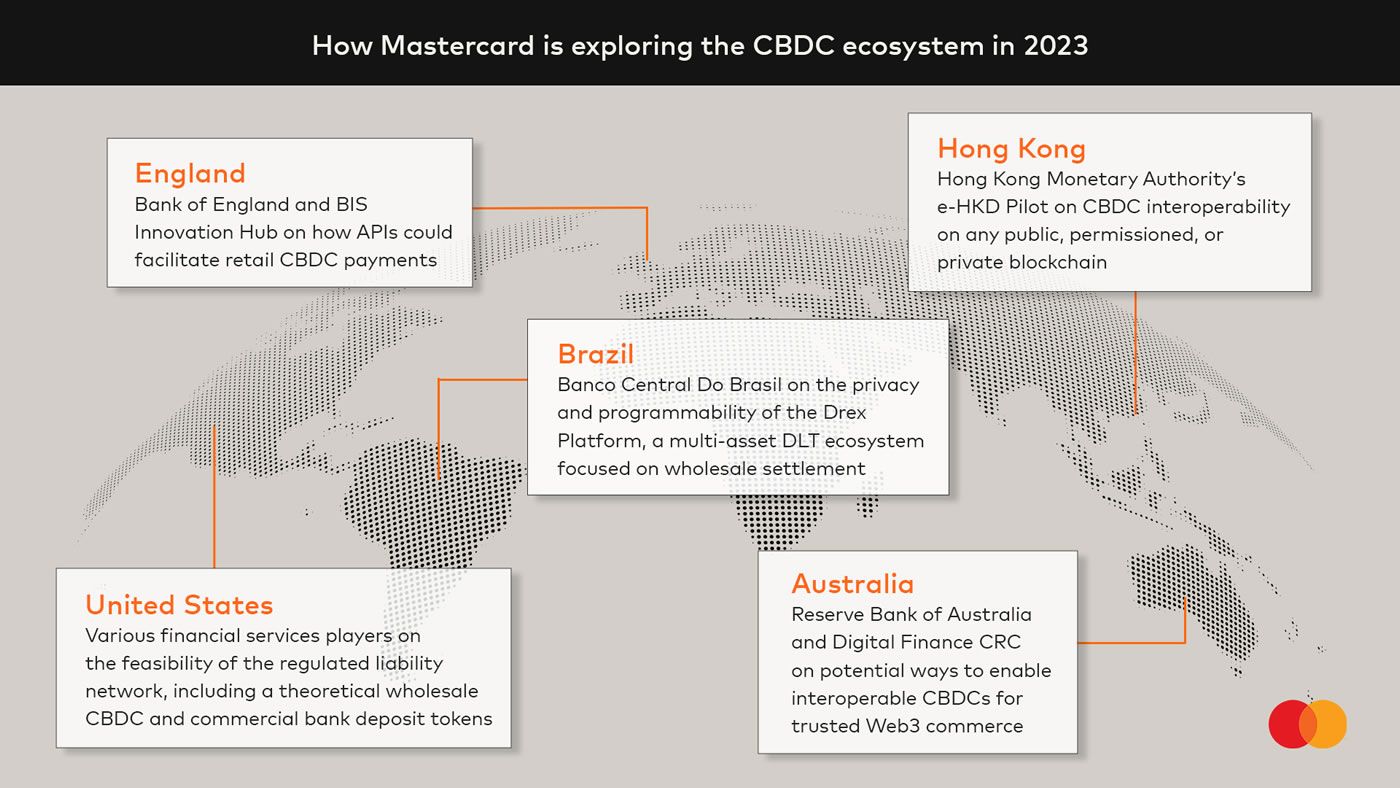

Mastercard itself is actively involved in the CBDC space. The company has completed testing its solution in the Hong Kong Monetary Authority’s e-HKD pilot program and is working to foster collaborations through its CBDC Partner Program.

The program aims to bring together blockchain technology and payment service providers, focusing on developing blockchain-based money.

The CBDC industry continues to evolve, with various countries at different stages of exploration and adoption. Some view CBDCs as a step forward in the digital evolution of money. However, others raise concerns over privacy and the extent of state control over financial transactions.

A delicate balance between innovation, consumer preference, regulatory considerations, and the specific financial needs of each country will likely shape the future of CBDCs.