Retiring early to escape the 9–5 slug and ease into a more relaxed lifestyle — that’s the dream, right? But, the truth is, early retirement planning is no joke. Everybody fancies the idea of it, but only a few can master the meticulous planning and the strict financial and lifestyle discipline required to pull it off.

So, if you also frequently wonder how to retire early with enough retirement savings to cover your cost of living for the rest of your life (along with good health insurance and other essentials), you need to touch bases on a few important points. That is precisely what this guide is about.

In this guide:

What is early retirement?

Early retirement means retiring before the expected or usual age and date of retirement. The concept of retiring early is not particularly new, although it seems to have gained more traction in several places across the world in the last few years, including in the U.S.

The trend may have picked up steam from the so-called Financial Independence, Retire Early (FIRE) movement, which encourages focused savings strategies to make early retirement planning easier.

Additionally, the COVID-19 pandemic and looming economic uncertainty have now prompted many businesses to encourage workers to step away before reaching their full retirement age. In such cases, the early retirees usually receive benefit packages for their cooperation.

Despite its mass appeal, early retirement is not for everyone. In fact, it is not for the overwhelming majority of people — especially those living in developing and underdeveloped parts of the world, that score low on the Human Development Index.

Even in the U.S., you will not be eligible for full Social Security retirement benefits if you retire at even 62. For example, anyone born between 1943 and 1954 will only be eligible for full benefits from 66 onward. For those born after 1954, the full benefit age is even higher.

That said, with smart planning and strict lifestyle discipline, you could accumulate enough retirement savings anywhere in the world. But before we discuss some of these strategies, let’s first address what is considered a good early retirement age.

What is considered early retirement age?

The definition of early retirement generally varies from place to place.

For example, in the U.S., the average retirement ages for men and women are 65 and 62, respectively. It is worth noting here that in comparison, the corresponding figures in 1992 were 62 and 59, respectively.

The official retirement age for male and female workers in China has been 60 and 50, respectively (55 for women holding management positions) since 1951. Meanwhile, India has standardized the official retirement age for central government employees at 60. Some state governments have further increased (or are considering increasing) it to 62 for their employees.

Depending on where you live, retiring before the traditional age of retirement would be considered early retirement.

The ideal early retirement age is also different from person to person, depending on how they go about their early retirement planning. For example, if someone has already made enough retirement savings and passive income sources at 40 to last them through at least a few decades, they may opt to hang their proverbial boots right at that point.

Early retirement calculator

There are several online early retirement calculators out there that you can use to get a general idea of how much you have to save, invest, or diversify to have a steady retirement income. Most of these calculators are free and easy to use.

You just have to feed some basic info to the calculator. For example, your annual income, at what age you intend to retire, and such. The calculator then crunches these numbers to give you some ideas.

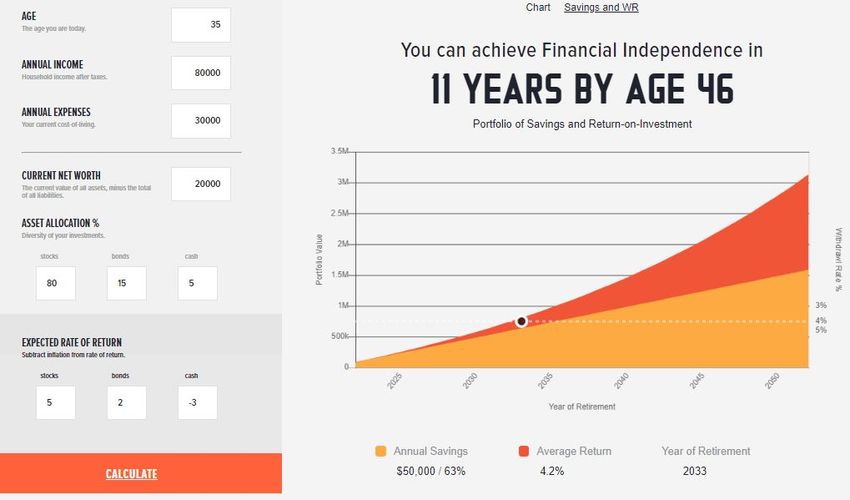

For example, the screenshot above shows a basic early retirement calculator by PlayingWithFire that helps you figure at what age you might achieve financial freedom.

Pros and cons of early retirement

Pros

- Free from the 9-to-5 slug. Becoming financially free and retiring early means you no longer have to report to a boss or slog in a job that you may not even enjoy anymore.

- You get enough time in your hand to spend time with friends and family, travel, pursue your passion, or tend to that side project you had been neglecting for ages.

- You will likely feel a lot better in the absence of all job-related stress and fatigue.

- Since you have enough time on your hands now, you can spend more time taking care of yourself — especially your health and physical fitness, which sometimes tend to take a backseat during working years.

Cons

- Years without any income. Now, that’s not necessarily going to be a problem if your early retirement planning involves starting new businesses (or passive income sources) where you can be your own boss and continue earning.

- If your job or profession is a big part of your identity, odds are there that you might have to confront a loss of meaning in life or an identity crisis. The best way to avoid this will be to plan a new post-retirement chapter in advance.

- You will no longer be covered by the healthcare benefits offered by your employer. In countries like the U.S., it may be a problem for some, as marketplace insurance policies can be very expensive. However, it is not generally a very big problem in many parts of the world, where insurance policies are a lot more affordable.

Early retirement planning: 7 tips that will help you

1. Focus on savings and don’t lose sight of your goal

If you are in your early-20s, that’s usually considered a very good time to start saving. If you are already past your 20s and do not have any significant retirement savings yet, now is the best time to start. Start small if you have to and try to gradually increase it over time. More importantly, devise a savings plan and stick to it (rather than saving whatever is left after monthly expenses). Your ultimate aim should be to achieve financial freedom.

2. Have clarity about your retirement needs

Retirement can be expensive. By some estimates, you might require almost 70% to 90% of your pre-retirement income to maintain a comparable lifestyle without having to make any major compromises. Therefore, it is advisable that you spend some time figuring out what your retirement needs are going to be. Do keep inflation in mind while planning your retirement.

3. Prepare for an unexpected rise in expenses

You might want to prepare for any eventual unplanned scenario wherein your expenses rise unexpectedly due to reasons beyond your control.

For example, consumer prices were up 9.1% in the U.S. over the year ending June 2022, as reported by the Bureau of Labor Statistics. That’s the highest in 40 years and if the inflation rate remains such a red-hot figure over a prolonged period, expect a substantial increase in your expenses too.

4. Leave your retirement fund alone

It is not uncommon to see people spending from their post-retirement fund on pre-retirement large purchases. Maybe the sizeable balance in their retirement savings is just too tempting for them to resist the urge. Avoid that mistake.

In addition to the obvious issue of the lack of financial discipline and any subsequent slippery slope, withdrawing from your retirement fund prematurely will lead to a loss of principal and interest. On top of that, you may even lose tax benefits and face penalties.

5. Invest regularly

Always try to save a portion of your regular monthly income to increase the size of your investment portfolio. Be it mutual funds, stocks, commodities, cryptocurrencies, or real estate investment — always plan meticulously and pick assets with good fundamentals and long-term potential. Make sure to diversify your portfolio for risk mitigation. And yes, do not hesitate to consult a financial advisor if need be.

6. Pay off all debts, avoid new

This probably needs no further explanation. Every loan you take from hereon — especially the long-term loans, will only create dents in your early retirement planning. Of course, some loans may be simply unavoidable, but your goal should be to pay all existing debts at the earliest and refrain from taking any further loans.

7. Set up passive income sources

You might also consider investing in assets that generate a regular stream of passive income. For example, investing in a small business or rental property is a good way to start. You might also take side-hustles in a profession/area that you have always had an interest in but never got enough time to pursue.

Act now, act smart

So, that was briefly an account of how you should ideally approach your early retirement planning. If you are just getting started and worry that it is already too late, don’t worry, it is never too late to start saving for your retirement. Just make sure to set up realistic goals and stick to those goals no matter what.

Broadly speaking, these are the five objectives you are aiming to achieve:

- You are debt-free.

- You have enough savings to maintain a comparable lifestyle post-retirement.

- All your present and future health expenses are planned and sorted.

- You are prepared to live on a budget.

- You are prepared to provide for your dependents.

And finally, never let your guards down and continue maintaining the kind of strict financial discipline that an endeavor like demands.

Good luck 🙂