As the old saying goes, two things are certain in life — death and taxes. Crypto gaining mainstream legitimacy has come with the tradeoff of increased scrutiny, regulations, and, you guessed it, taxes. In the U.S., many people file crypto taxes using 1099 forms. This guide covers the various 1099 forms to be aware of in 2026.

KEY TAKEAWAYS

➤ 1099 forms are reports issued by platforms to the IRS and recipients to disclose non-employment income, including crypto-related activity.

➤ Different 1099 forms apply to crypto depending on the nature of the transaction, including 1099-MISC, 1099-B, and soon, 1099-DA for digital assets.

➤ Current 1099 forms often lack complete data fields, especially around cost basis and DeFi activity.

➤ The upcoming 1099-DA aims to standardize crypto tax reporting, but many gaps and complexities remain unresolved.

What are 1099 forms?

A 1099 is a tax form that reports income or transactions you receive outside of regular employment. For example, a W-2 form reports an employee’s income from the previous year and includes how much the employer withheld for taxes.

With a 1099, taxes are not withheld. It simply tells the IRS how much money you made or transacted so you can report it, and they can verify it.

There are over 20 types of 1099 forms, covering activities ranging from freelance income and interest earnings to real estate transactions and retirement distributions.

If you receive income outside of regular employment (e.g., freelancing, selling crypto, etc.), there is no automatic withholding, and it is the filer’s burden to report it.

1099 tax forms for crypto

When you go to do your taxes, you will notice that there are many 1099 forms for various activities. However, many will not apply to crypto. 1099 forms are divided based on the type of income or transaction they report. Some crypto users might receive multiple types of 1099s:

- 1099-K

- 1099-MISC

- 1099-B

- Soon: 1099-DA for everything digital asset-related

Each of these forms captures a different aspect of your crypto activity, but receiving one doesn’t always mean your tax reporting is complete. Due to a lack of clear guidance, businesses and filers have taken different approaches to which 1099 forms they issue for tax reporting.

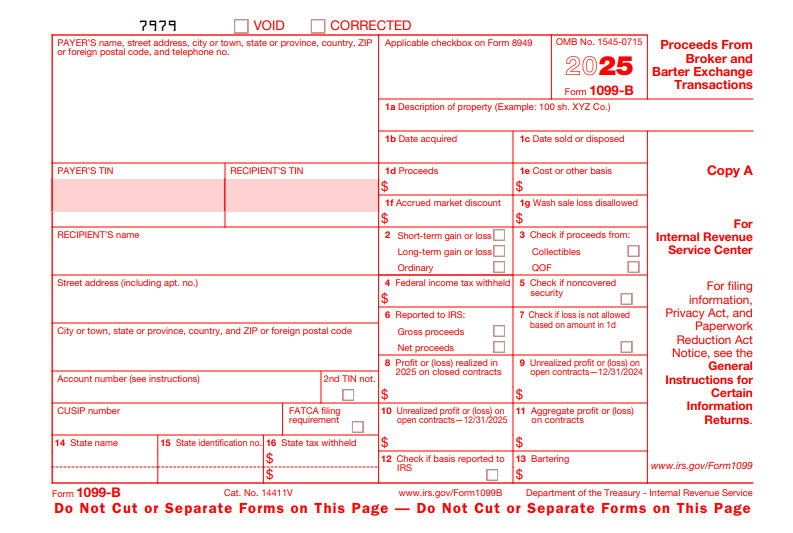

1099-B (Proceeds from broker and barter exchange transactions)

The 1099-B form reports transactions from brokerages or barter networks. It includes details such as your cost basis, the amount you received from the sale (gross proceeds), and any capital gains or losses.

It is designed for brokers to report proceeds from the sale of securities and other property, not typically for traders and investors to fill out themselves. Your broker should issue one of these to you.

For a while, it was debated whether crypto platforms counted as brokers under this definition. Despite the ambiguity, some U.S.-based exchanges (like Coinbase) choose to issue 1099-Bs for crypto sales anyway — in part to mirror traditional brokerage reporting.

However, these forms often contain missing or incomplete cost basis information, which has caused much confusion and resulted in mismatches with IRS records. For example, if users transferred crypto from other wallets or platforms, the exchange would not have the true cost basis information, and filers would not know to report it.

The Infrastructure Investment and Jobs Act of 2021 clarified that digital asset platforms can be treated as brokers under tax reporting rules. This act expanded the definition of a broker to include those providing services to effectuate transfers of digital assets. However, the actual enforcement requirement (like a standardized 1099 form for crypto) was delayed.

Most exchanges do not issue a 1099-B. Some, like Coinbase and Crypto.com, will issue a 1099-B, but only for contract trading. Coinbase will also provide you with a raw transaction report and your gains/losses report so that you can file your taxes on your own.

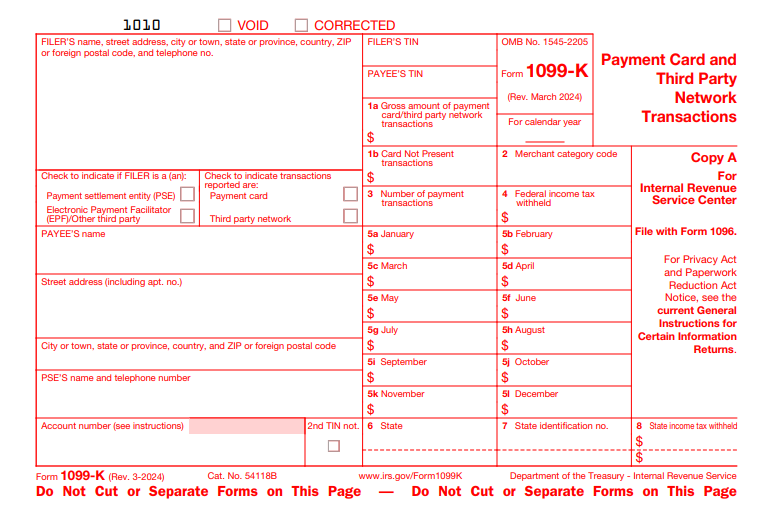

1099-K (Payment card and third-party network transactions)

Payment processors (like PayPal, Venmo, and sometimes crypto exchanges) issue the 1099-K form when payments for goods or services exceed certain thresholds. It was originally designed for platforms like eBay or Etsy.

Previously, the threshold for reporting payments accumulated over a calendar year was $20,000. The American Rescue Plan Act (ARPA) lowered this threshold to $600 to capture income from online platforms and the emerging gig economy in the U.S. This implementation has faced multiple delays, so the original threshold is still in effect.

The ARPA’s $600 threshold was extremely unpopular at the time, as it had the potential to sweep everyday people into complex tax reporting. While not stated outright, concerns about adding financial strain to everyday Americans during a period of economic uncertainty likely played a role in the decision to delay implementation.

If you’re accepting crypto payments as a business or for services through platforms like BitPay, or even NFT marketplaces, you might be issued with a 1099-K. Some centralized exchanges used to issue the 1099-K to high-volume users, even if the activity was just trading. This has caused many tax mismatches.

For instance, you’d get a form showing gross proceeds (the total amount you received) but not the cost basis (what you originally paid) because the 1099-K does not track that.

Since the IRS also receives the 1099-K, when they review the form, it may show (for example) $100,000 in proceeds and $5,000 in net gain (gross proceeds – income). The IRS would then question where the other $95,000 is. Therefore, your tax return can raise a red flag and potentially lead to an audit — even if your reporting is correct.

Coinbase used to issue a 1099-K to its users but stopped after 2020 because it caused confusion. The forms reported the total amount of crypto traded but not the profits. As a result, many customers received IRS CP2000 notices accusing them of underreporting income. As of 2026, Coinbase issues the 1099-MISC in place of the 1099-K.

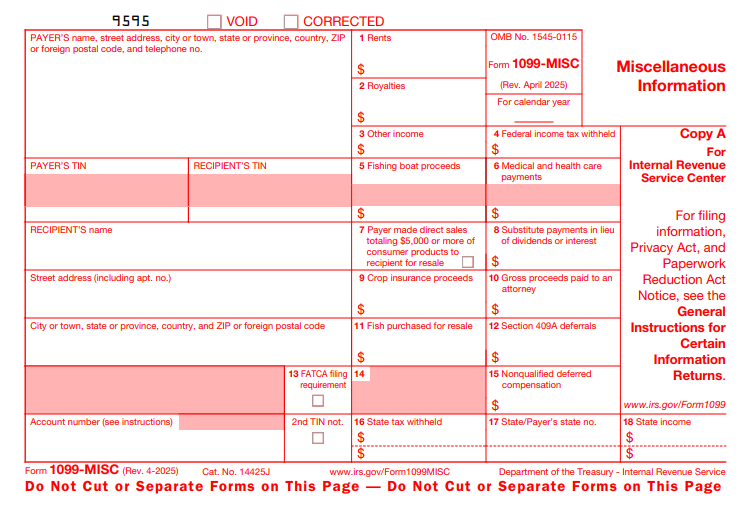

1099-MISC (Miscellaneous information)

The 1099-MISC reports various types of non-employee income. It is sort of a catch-all for “miscellaneous” types of income that don’t fit neatly into other 1099 categories. You’ll see it used for things like rent payments, prizes, royalties, and legal settlements.

If a type of income doesn’t have its own 1099 form and is not paid to an employee, it will most likely end up on a 1099-MISC. In crypto, you might get a 1099-MISC if you:

- Earn staking rewards

- Receive airdrops

- Get referral bonuses or incentive rewards

All income reported on 1099-MISC is generally taxable as ordinary income at the time of receipt, based on the fair market value of the crypto on that date. Again, the IRS gets a copy, so you want to make sure it’s on your return (even if small). You will receive a 1099-MISC if:

- You receive at least $10 in royalty payments or broker payments made in lieu of dividends or tax-exempt interest.

- You receive at least $600 in rent, prizes and rewards, staking, etc.

- You made direct sales of at least $5,000 of products to a buyer for resale anywhere other than a retail establishment.

Receiving a 1099-MISC just means the IRS is being notified of the transaction. How and when it’s taxed will still depend on legal interpretations, guidance, or future IRS rulings.

Other 1099 forms that may apply

While 1099-MISC and 1099-B are the most common in crypto, other forms can apply. Forms like the 1099-NEC, 1099-R, and 1099-INT are less common for crypto activities but may apply in specific scenarios:

1099-NEC (Non-employee compensation): Used when you’re paid in crypto for freelance work or services. This typically applies if you’re classified as an independent contractor. Some platforms may use this form instead of the 1099-MISC.

1099-R (Retirement): Issued if you take a distribution from a retirement account (like a self-directed IRA or 401(k)) that holds crypto. The form reports withdrawals, rollovers, or conversions that may be taxable.

1099-INT (Interest): Rare, but possible if you earn interest through certain platforms that treat DeFi lending returns as traditional interest. The income is reported as interest even though it may come from crypto activity.

In some cases, the form you receive depends on how the income is classified and reported by the platform — not just the nature of the crypto itself.

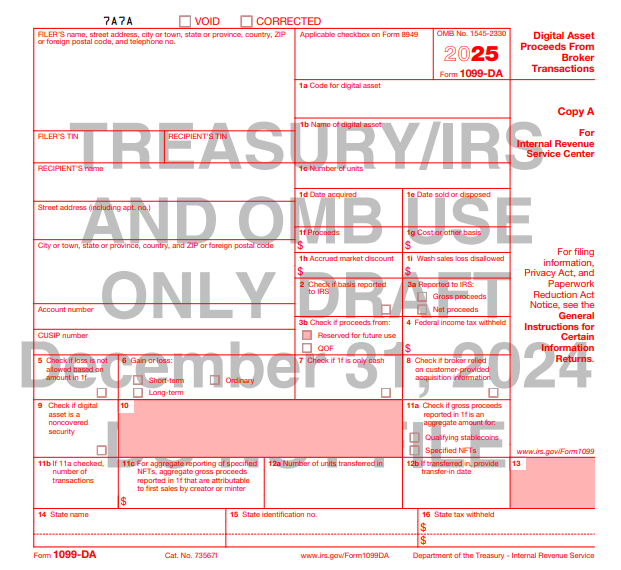

1099-DA (Digital assets)

This guide would be remiss if it did not mention the 1099-DA. The 1099 “Digital Asset Proceeds From Broker Transactions” is the IRS’s first tax form with the express purpose of reporting digital assets.

Reporting for the 1099-DA is currently in effect as of Jan. 1, 2025. This means that all trades performed through digital asset brokers will be reported to the IRS in 2026 (not for filing in 2025).

This image is a preliminary draft of the 1099-DA and should not be used for actual filing.

The IRS designed the 1099-DA to standardize tax reporting for digital asset transactions. Brokers must report:

- Purchase and sale price

- Acquisition and sales date

- Other transaction details (to calculate gains/losses)

Anyone who qualifies as a digital asset broker must file. As mentioned earlier, the definition of a digital asset broker has been debated due to a lack of regulatory clarity. However, under the final IRS rules, a broker is a person or entity that facilitates digital asset transactions for customers and has access to or verifies the identity of counterparties.

Despite the benefits, complexities still exist, as crypto transactions are often diverse and complex. Taxpayers will still need good records and professional help. Per IRS Notice 2024-57, certain DeFi activities are not currently subject to 1099-DA reporting, including:

- Wrapping/unwrapping tokens

- Liquidity providing

- Staking and lending

- Short sales

- Notional principal contracts

The IRS and Treasury Department have resolved that these types of transactions require further study to determine how to report them correctly. Therefore, brokers are not required to report them until a determination is made.

A brief history of crypto taxes in the US

As crypto adoption grew in the U.S., people were buying, selling, staking, swapping, and earning without clear reporting. This was often done without realizing they were creating taxable events. The U.S. government saw this as a growing problem.

The first major policy mandate came in 2014, when the IRS issued Notice 2014-21, declaring that virtual currencies like Bitcoin would be treated as property, not currency, for tax purposes. However, without a formal reporting framework in place, the rule left many users unsure of how to comply.

For several years, the IRS issued no further guidance. Eventually, the IRS added a digital assets question to the 1040 form. It flagged to the IRS whether you were involved in crypto, even if you didn’t get a 1099 or owe tax. It first appeared on Schedule 1 in 2019 and moved to the front of the 1040 in 2020.

From there, exchanges started experimenting with different 1099 forms. Some issued 1099-Ks, while others issued 1099-Bs or 1099-MISCs. This created a lot of confusion due to mismatched reporting standards and incomplete cost-basis data.

These circumstances led to the Infrastructure Investment and Jobs Act of 2021, which laid the groundwork for the 1099-DA form.

To learn more about cryptocurrency taxes in the U.S., check out BeInCrypto’s U.S. Crypto Tax Guide for 2026.

Consult an expert for tax filings

Crypto 1099 forms are primarily used by businesses, platforms, or payers to report transactions to the IRS. Recipients use them to help file accurate tax returns. They are informational, not tax filings themselves. The most common forms that you will receive in the U.S. are the 1099-B, 1099-K, or 1099-MISC. Though the 1099 forms are helpful, they are not comprehensive and have led to some miscommunication due to complexities in blockchain and DeFi transactions and the lack of dedicated fields to report necessary information.

Although the 1099-DA is set to provide a more uniform framework for reporting digital asset transactions, limitations still exist, which will require further study. To avoid any IRS notices or audits, always consult a tax preparer or certified public accountant (CPA).

Frequently asked questions

Most crypto transactions that don’t fall under employment in the U.S. will be reported using 1099 forms. The forms are meant for businesses to report transactions to the IRS. 1099 forms are not meant for filing, but aiding in tax preparation filings.

The most common forms used for reporting crypto activities are the 1099-MISC, 1099-K, and 1099-B. There are many other forms that may apply to select crypto transactions, but are rarely used, as there is a lack of regulatory clarity. Most people tend to use the 1099-MISC; however, using this form does not guarantee compliance.

The 1099-DA is the first 1099 form that was made specifically for digital assets. The form went into effect on Jan. 1, 2025. Although the form is comprehensive, it does not cover all crypto activities due to the complexity of crypto transactions.

Cryptocurrencies like Bitcoin are considered property in the U.S. Therefore, they are subject to capital gains taxes. Depending on the types of activities, certain cryptocurrency transactions may also fall under income taxes. The U.S. tax codes for cryptocurrencies and related transactions are not distinct and require further study for clarity.

Yes, you must pay taxes on cryptocurrencies and related transactions in the U.S. Failure to do so could result in significant penalties. It is advised to consult a tax preparer or certified public accountant (CPA) for proper tax filings.