The ICO boom may be over, but the U.S. Securities and Exchange Commission appears to be just getting started.

Salt Lending has become the latest target of the regulator after the SEC issued a cease-and-desist letter to the crypto-backed lender, aka Salt Lending, on Sept. 30. In its letter, the securities watchdog stated that Salt “violated Section 5(a) of the Securities Act” with its 2017 token sale in which it raised $47 million.

The letter also outlines a settlement between Salt Lending and the SEC, the details of which Salt director of marketing communications, Kendra Staggs, shared with BeInCrypto, saying,

“Salt has cooperated with the SEC and has been working toward a settlement for many months. Under the terms of the SEC Settlement, the company will register SALT Tokens under Section 12(g) of the Securities Exchange Act of 1934 as a class of securities, maintain that registration and make timely filings as required by law and the SEC Settlement, and pay a civil monetary penalty of $250,000.”She went on to explain,

“In addition, under the terms of the SEC settlement, the company will administer a claims procedure available to those who purchased SALT Tokens directly from the Company before and including December 31, 2019.”

Hindsight Is 20/20

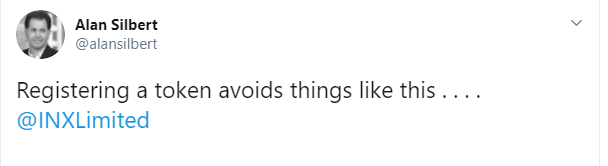

Alan Silbert, executive managing director at registered digital asset exchange INX, suggested the entire situation could have been avoided if Salt had just registered its token in the first place.

“The Company intends that bitcoin or ether received as payment will be sold promptly as the Company does not intend to hold bitcoin or ether as ongoing investments.”

Early DeFi Project?

Salt is a lending platform that issues crypto-backed loans. If that sounds familiar, it’s because that’s precisely the type of protocol that has flooded the DeFi space. One Reddit member took notice, suggesting it was an early DeFi idea that flopped:

“Kik” the Can

Salt Lending is the latest company to be on the radar of the securities watchdog, but it’s not the only one. Messaging app Kik has been battling it out in the courts for more than a year over a $100 million token sale. The regulator maintains that Kik failed to register its Kin token as a security, calling the ICO “illegal.” Kik CEO Ted Livingston vowed to fight the SEC in court, saying a year ago that “becoming a security would kill the usability of the coin and set a dangerous precedent for the industry.” Most recently, Bloomberg Law reported that a judge held Kik’s feet to the fire for not registering its token as a security.Disclaimer

In adherence to the Trust Project guidelines, BeInCrypto is committed to unbiased, transparent reporting. This news article aims to provide accurate, timely information. However, readers are advised to verify facts independently and consult with a professional before making any decisions based on this content. Please note that our Terms and Conditions, Privacy Policy, and Disclaimers have been updated.

Gerelyn Terzo

Gerelyn caught wind of bitcoin in mid-2017, and after becoming smitten by the peer-to-peer nature of crypto has never looked back. She has been covering the space ever since. Previously, she wrote about traditional financial services, Wall Street and institutional investing for much of her career. Gerelyn resides in Verona, N.J., just a hop, skip and a jump from New York City.

Gerelyn caught wind of bitcoin in mid-2017, and after becoming smitten by the peer-to-peer nature of crypto has never looked back. She has been covering the space ever since. Previously, she wrote about traditional financial services, Wall Street and institutional investing for much of her career. Gerelyn resides in Verona, N.J., just a hop, skip and a jump from New York City.

READ FULL BIO

Sponsored

Sponsored