Although DeFi is often termed the TradFi disruptor, TradFi still plays a significant role in our daily lives in 2026. This covers everything you need to know about traditional finance, discussing its advantages and disadvantages as well as the sector’s growing appetite for crypto (in the form of ETFs and other regulated instruments). Here’s what you need to know.

KEY TAKEAWAYS

➤ Traditional finance (TradFi) is built on centralized institutions like banks, credit unions, and asset managers.

➤ Central banks play a foundational role in TradFi by setting monetary policy and regulating currency and interest rates.

➤ Financial instruments in TradFi include stocks, bonds, derivatives, and mutual funds used for saving, investing, and lending.

➤ In 2026, TradFi still dominates global finance due to its established infrastructure and regulatory trust.

- What is traditional finance (TradFi)?

- Financial institutions in TradFi and their roles

- TradFi’s meets crypto: ETFs and institutional adoption

- Importance of regulation in TradFi

- Pros and cons of TradFi

- Understanding the banking system in TradFi

- Exploring key financial instruments in TradFi

- Risk management in TradFi

- The future of TradFi in a digital economy

- Frequently asked questions

What is traditional finance (TradFi)?

Traditional finance, TradFi in short, refers to the established financial system that has been in place for many years.

It consists of financial institutions, such as central banks, commercial banks, brokerage firms, investment banks, credit unions, pension funds, retail banks, insurance companies, mortgage companies, savings and loans associations, and mutual funds. These institutions often serve as intermediaries, facilitating transactions between parties involved in financial activities.

If you possess a savings or checking account with a bank, you have already engaged with TradFi. Insurance services, financial assets trading, bank loans, mortgages, and investment services are all part of the TradFi world.

The term TradFi often comes up in relation to DeFi, a relatively new financial system that aims to be decentralized, thus, intermediary-free.

Financial institutions in TradFi and their roles

Traditional finance relies on a broad range of institutions, each with a specific function in maintaining the stability and flow of capital in the economy. From setting monetary policy to managing your personal savings, these institutions form the backbone of the financial system you interact with daily.

Central banks

Central banks oversee and regulate all licensed banks operating within a country. They are responsible for implementing monetary policy, setting interest rates, financing commercial banks, and ensuring the overall stability of the financial system.

Although central banks do not serve individual customers directly, they act as the “bank for banks.” Basically, they provide liquidity and guidance to the broader banking system.

One of their primary roles includes regulating the circulation of fiat currency — the official legal tender of a country.

Each country operates its own central bank. For instance, in the U.S., it’s the Federal Reserve (the Fed). The U.K. has the Bank of England. Switzerland is served by the Swiss National Bank, while China operates through the People’s Bank of China.

Commercial and retail banks

Retail banks deal directly with consumers. They offer services such as savings and checking accounts, debit and credit cards, and personal loans.

Commercial banks, on the other hand, cater to businesses — both small and large — by offering loans, cash flow management, trade financing, and corporate banking products.

Investment banks

Investment banks help raise capital for corporations, governments, and individuals. They underwrite securities, manage IPOs, advise on mergers and acquisitions, and offer portfolio strategies to help clients optimize their returns.

Credit unions

Credit unions are nonprofit organizations that return profits to members through lower fees and higher interest on deposits. They serve people who share a common bond — such as a workplace, community, or geographic location — and operate democratically, with members having a say in how the union is run.

Brokerage firms

Brokerage firms act as intermediaries, allowing individuals and institutions to buy and sell financial instruments.

These include stocks, bonds, ETFs, and mutual funds. Brokerages also offer research tools, investment advice, and portfolio management services.

Savings and loan (S&L) associations

Also known as thrifts, S&L associations primarily focus on residential mortgages. They also provide checking accounts and personal loans. Ownership often lies with the account holders, who may benefit from more personalized service and competitive rates.

Mortgage companies

Mortgage companies specialize in originating and funding mortgage loans. While many serve individual homebuyers, some focus exclusively on commercial property loans. They may sell loans to larger financial institutions or retain them for servicing.

Insurance companies

Insurance companies help individuals and businesses manage financial risks linked to accidents, illness, property damage, and other unforeseen events. In exchange for premium payments, they provide coverage through policies tailored to each client’s needs.

Asset management firms

Asset management firms pool capital from individuals, institutions, or pension funds and invest it across assets such as equities, bonds, or real estate.

They manage mutual funds, ETFs, and portfolios for both small investors and high-net-worth clients, aiming to grow wealth based on each client’s investment objectives and risk tolerance.

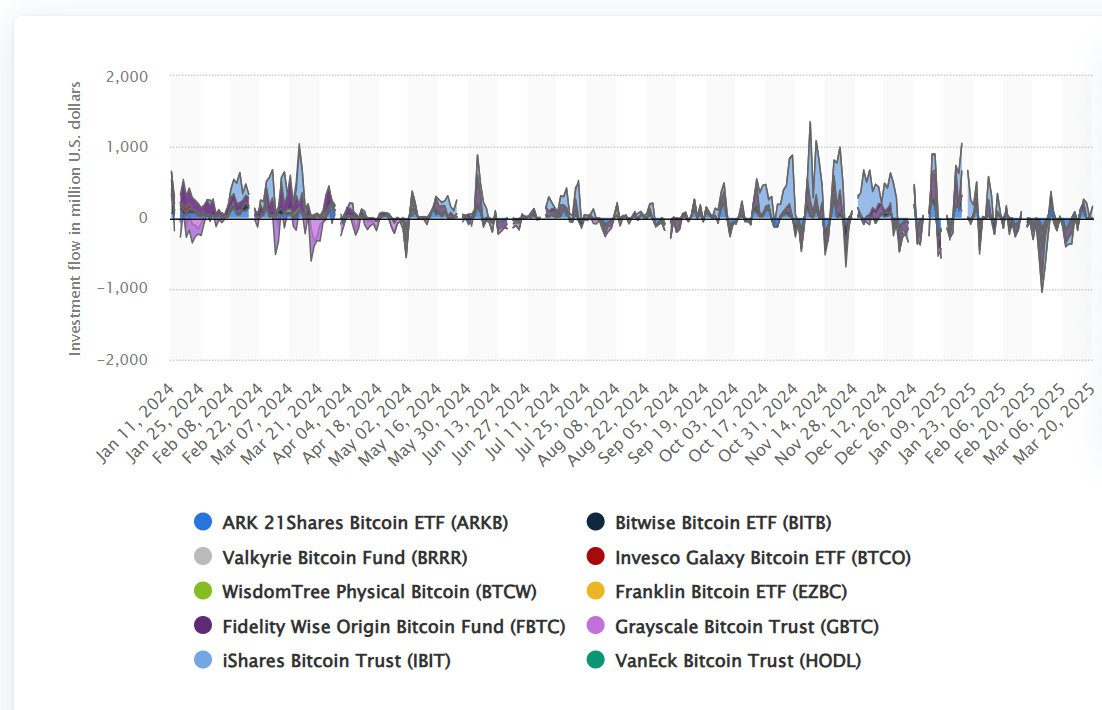

TradFi’s meets crypto: ETFs and institutional adoption

Traditional finance (TradFi) is no longer sitting on the sidelines when it comes to crypto. Major asset managers like BlackRock, Fidelity, and Grayscale have launched spot Bitcoin and Ethereum ETFs to bring you a regulated pathway to gain exposure to digital assets without the complexities of direct ownership.

For instance, BlackRock’s iShares Bitcoin Trust (IBIT) alone has attracted over $63 billion in assets as of May 13, 2025. That makes it among the largest Bitcoin funds globally.

This surge in ETF activity reflects a broader institutional shift. Firms such as 21Shares and WisdomTree have introduced crypto-backed exchange-traded products (ETPs) across Europe, while Grayscale has expanded its offerings to include Ethereum and AI-focused crypto funds.

These developments provide you with more avenues to incorporate digital assets into your investment strategies.

Governments are also taking note. States like New Hampshire have passed legislation to allocate up to 5% of their reserves into Bitcoin. The move signifies a growing acceptance of crypto in public finance.

Additionally, the launch of regulated crypto derivatives platforms like GFO-X in London indicates a move towards integrating crypto into mainstream financial markets.

For you, this means that crypto is becoming an increasingly viable component of a diversified portfolio.

In other words, the barriers to entry are lowering with the backing of established financial institutions and evolving regulatory frameworks. And that makes it even easier to explore crypto investments within the TradFi ecosystem.

Importance of regulation in TradFi

Regulations govern the operations of financial institutions in TradFi. Among the most common regulatory requirements are KYC and AML. Know your customer (KYC) entails a mandatory process to identify and verify a customer’s identity.

For example, when opening a bank account, you’re typically required to submit personal details such as your full name, a government-issued ID, phone number, and a recent photograph. On the other hand, anti-money laundering (AML) regulations are in place to prevent criminals from disguising illegal money as legitimate income.

In some countries and for some regulations, the central banks ensure that financial institutions comply with the financial regulations in place. In other countries, there are specific regulators for different markets. Without oversight authorities, economies would be at risk of instability.

“Regulatory compliance is critical to managing risk.”

CEO of Mayflower-Plymouth, Hendrith Vanlon Smith Jr

Therefore, regulations in TradFi are essential since they not only keep financial systems stable but also protect consumers and the economy from harm and prevent unauthorized firms from offering financial services.

Pros and cons of TradFi

| Pros | Cons |

|---|---|

| Deeply rooted system with strong public trust | Cases of front-running, insider trading, and unequal access still occur |

| Comprehensive regulatory oversight helps protect consumers | Money laundering can still happen despite AML frameworks |

| Wide range of financial services and tailored products | Transactions are often slow and can take days to settle |

| Focus on consumer protection and responsible financial conduct | High transaction fees due to multiple intermediaries |

| Deposit insurance schemes protect consumers from bank failures | Access often requires extensive documentation, excluding those without proper identification |

| Credit scoring systems help individuals access loans based on financial history |

Understanding the banking system in TradFi

Banks accept deposits from clients who hold savings and checking accounts with them. Additionally, they acquire funds from the government, merging these resources with deposits to provide loans to borrowers.

That means banks act as financial intermediaries, facilitating the transfer of funds from depositors with excess capital to individuals and businesses needing financial resources.

Banks generate profits by charging interest rates on loans that exceed the interest they pay on the funds borrowed from the government (via the central bank). As a result, the government becomes the primary depositor and creditor for banks.

Overview of financial intermediaries in TradFi

Banks, credit unions, financial advisors, insurance companies, and other financial intermediaries play vital roles in TradFi. Here are some of the advantages of financial intermediaries:

- Reducing risk: Banks allow individuals or businesses with excess funds to distribute their loans among multiple vetted borrowers. This approach carries lower risk compared to lending money to a single individual. Furthermore, insurance companies minimize the risk of financial loss by providing policy benefits in the event of accidents or catastrophes experienced by their clients.

- Economies of scope: Financial intermediaries can provide specialized services and products to fit various customer needs. For example, commercial banks can create different products for small and large corporations.

- Economies of scale: Financial intermediaries have access to large amounts of cash from depositors that they can loan to multiple borrowers with solid credit ratings. This practice minimizes the overall operational costs.

Exploring key financial instruments in TradFi

A financial instrument is a contractual agreement that holds value and can be traded. The following are key financial instruments commonly found in TradFi.

Stocks

Stocks or equities represent fractional ownership in a company. Shareholders are entitled to a portion of the company’s assets and profits based on the amount of shares they hold. Stocks are equity-based financial instruments.

Mutual funds

A mutual fund is an investment vehicle that pools funds from many investors. It then invests the money in stocks, short-term debt, and other securities.

Investors who buy shares in mutual funds receive part ownership in the fund and are entitled to a portion of the fund’s income based on the number of shares they hold. Mutual funds are equity-based financial instruments, with money market funds being a prime example.

Bonds

Bonds are long-term debt-based financial instruments that governments and corporations use to raise money. Therefore, bond buyers give issuers a loan for a certain period of time.

Bond issuers are responsible for paying back the loan at face value at a set date (principal), plus a few interest payments.

Treasury bills (T-bills)

Treasury bills, also known as T-bills, are financial instruments based on short-term debt. They are issued by governments and have a predetermined interest rate and a maturity period of 365 days or less.

Investors who hold T-bills receive their initial investment plus interest at the end of the specified term. These instruments are considered low-risk as they are backed by the Treasury of the issuing country.

Bank deposits

Bank deposits are funds that customers place at a banking institution through checking, money market, or savings accounts. A bank deposit is a liability that the bank owes to the depositor.

As a result, bank deposits are debt-based cash instruments. Moreover, checks and loans are cash instruments since they can transmit payments between bank accounts. Deposit insurance ensures that customer funds are protected up to a certain amount.

Certificates of deposit (CD)

A certificate of deposit is a type of savings bank account that holds money for a certain period of time. Investors collect their initial investment plus interest when they redeem their CD.

Commercial papers

Commercial papers are unsecured short-term debt obligations that banks and large corporations issue to fund operations. This instrument pays a fixed interest rate and has a maturity of up to 270 days.

ETFs

Exchange-traded funds are investment vehicles that allow investors to pool their money together and earn interest. The fund then invests in stocks, bonds, and other securities.

ETFs are more flexible than mutual funds because investors can trade them at exchanges throughout the day. This stands in contrast to mutual funds, which investors can only purchase or redeem at the end of a trading day.

Derivatives

Derivatives are financial contracts between two or more people. They derive their value from the performance of an underlying asset. Stocks, market indexes, bonds, digital assets, interest rates, and commodities are examples of possible underlying assets. The four main types of derivatives are futures, forwards, swaps, and options.

Mortgage-backed securities (MBS)

Mortgage-backed securities are debt-based financial instruments. Financial intermediaries create mortgage-backed securities by pooling together mortgages.

So, when you buy an MBS, you are lending home buyers money. In return, you earn regular payments on your investment.

Real estate investment trusts (REITs)

REITs are investment vehicles that permit collective investment in real estate. A REIT allows individuals to invest in real estate assets like hotels, shopping malls, and apartments and earn interest.

Pension funds

Pension funds are investment schemes that provide retirement benefits to retirees. Both employees and employers can contribute money to a pension fund. Fund managers invest the contributions, allowing the fund to pay employees an income after retirement.

Credit cards

Credit cards are generally unsecured debt-based financial instruments that enable customers to borrow money within a pre-set limit. Cardholders must pay off the balance plus interest each billing cycle.

Risk management in TradFi

Governments typically implement deposit insurance systems to protect depositors in the event of a bank’s inability to facilitate withdrawals. The financial instruments that a deposit insurance body covers may vary from country to country. Also, deposit insurance agencies may not cover all financial institutions.

To illustrate, the U.S. Federal Deposit Insurance Commission (FDIC) only covers bank deposits up to $250,000 per customer “for each account ownership category.” This cover only applies to FDIC-insured banks.

The FDIC doesn’t insure stocks, bonds, T-bills, crypto assets, mutual funds, safe deposit boxes, and other financial products. That means investors must use risk management strategies like diversification to minimize portfolio risk.

The future of TradFi in a digital economy

Decentralized finance is already disrupting TradFi by offering benefits like more financial freedom and increased financial inclusion. These benefits are much needed, especially because the current financial system is restrictive, and 1.4 billion people remain unbanked. Therefore, TradFi businesses could start adopting decentralized structures as more and more people demand financial inclusion and freedom.

However, DeFi can also borrow TradFi’s good practices, like protecting consumers and curbing illicit activities. Ultimately, the two sectors are already beginning to merge as each borrows from the other, with TradFi dipping a toe into DeFi investments and decentralized protocols looking to improve customer protections and usability.