Back in 2022, the crypto lending market nearly collapsed under its own weight. Platforms like Celsius, BlockFi, and Voyager that promised stability imploded within months. Billions in user funds vanished, and confidence in centralized lending evaporated. Many assumed the experiment was over.

Yet three years later, CeFi lending has made a quiet comeback. The players are fewer, their rules tighter, and their ambitions more measured. According to Galaxy Research, the sector now accounts for $17.78 billion in active loans, which is roughly 40% of the global crypto credit market.

On the surface, that looks like a return to form. But underneath, the same question that haunted the market before still lingers: when you hand over your crypto, how much of it do you really control?

KEY TAKEAWAYS

➤ CeFi lending rebounded to $17.78B in 2025, but transparency and rehypothecation risks still persist.

➤ Three major players — Tether, Nexo, and Galaxy Digital — now control up to 89% of CeFi lending.

➤ Institutions prefer CeFi for regulatory clarity and speed, but opacity keeps systemic risk alarmingly high.

➤ Platforms like CoinRabbit push for transparency by rejecting rehypothecation and keeping all client funds segregated.

Trust returns, but only partly

The recovery began slowly, then accelerated. Galaxy’s Q2 2025 data show combined outstanding loans of $44.25 billion, excluding CDPs, and $53.09 billion, including them. Those numbers are close to the all-time highs of 2021.

DeFi led the rebound as it captured almost 60% of the market with $26.47 billion in active loans and an impressive 42% quarter-over-quarter growth.

For instance, Aave’s surge says it all. By August 2025, the platform had surpassed $3 trillion in cumulative deposits, with more than $29 billion in active loans and a total value locked (TVL) above $40 billion. Users expectedly moved where visibility existed. On DeFi platforms, transactions and collateral movements are visible on-chain, so you can see risks instead of assuming them. That visibility helped DeFi rebuild the confidence CeFi once commanded (and still struggles to fully recover).

CeFi, meanwhile, rebuilt more cautiously. After the 2022 wipeout, only a handful of firms survived. They refocused on compliance, risk monitoring, and brand credibility. The result was a smaller but sturdier segment, growing at 14.66% quarter-over-quarter to reach that $17.78 billion mark.

However, even with stricter discipline, old weaknesses still persist.

Rehypothecation — the reuse of client collateral — remains widespread even today. When platforms redeploy user assets for their own strategies, they amplify exposure. And if markets crash, that same web of reuse turns into a chain reaction of liquidations. Trust may have been rebuilt, but transparency still hasn’t caught up.

The new hierarchy of lenders

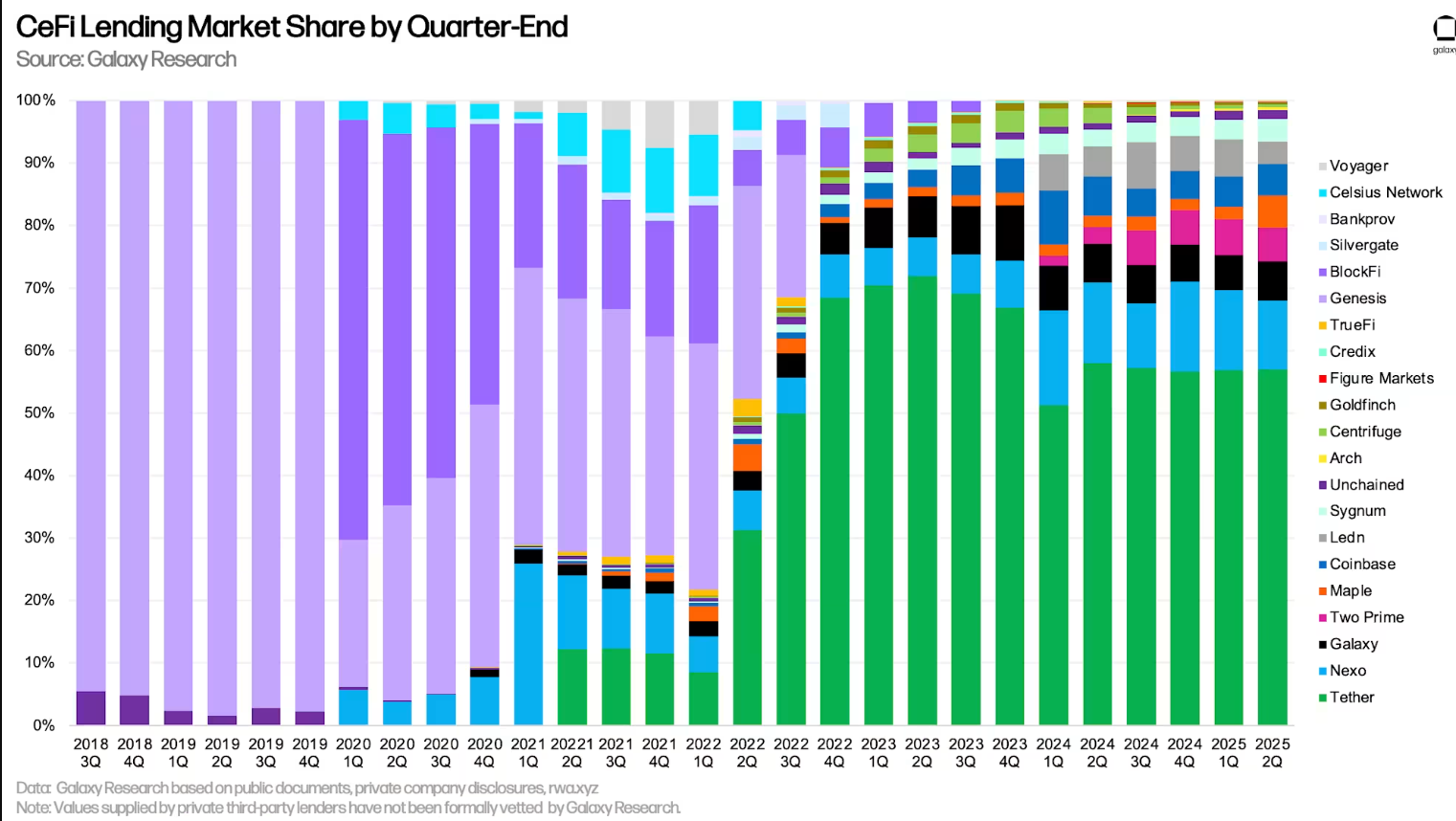

Today’s CeFi is dominated primarily by three names: Tether, Nexo, and Galaxy Digital. Together, they control 74–89% of all centralized lending, depending on the data source.

Tether alone accounts for 57.02%, or $10.14 billion, followed by Nexo at 11% ($1.96 billion) and Galaxy Digital at 6.23% (~$1.11 billion). A Herfindahl-Hirschman Index between 3,450 and 3,500 officially qualifies the market as an oligopoly.

This level of concentration comes with consequences. For instance, if a major player experiences a liquidity crunch, the rest of the market could freeze within days.

Moreover, because CeFi operates in the dark, users can’t even verify loan books, collateral ratios, or internal policies. And with so much power consolidated, these firms can effectively dictate lending and deposit rates, which could then limit competition and innovation across the board.

Smaller lenders, meanwhile, are caught in the middle. They can’t match the big players’ scale, so they compete on speed and experience rather than structure. Security slowly turns into a selling point instead of a baseline, which is a strange reversal for an industry born out of the promise of safety.

History’s warning still stands

When Celsius collapsed in June 2022, it managed $20 billion in assets across 1.7 million accounts. It failed for simple reasons: rehypothecation, reckless yield chasing, and zero liquidity preparation.

The firm lent customer deposits into long-term, illiquid projects while guaranteeing short-term withdrawals. When markets turned, the model imploded overnight.

What’s striking is how many of those same structural vulnerabilities still exist. CeFi lenders now speak the language of compliance and “prudence,” but rehypothecation hasn’t gone away. It’s just more quietly disclosed in the fine print.

High concentration means systemic risk hasn’t been reduced; it’s simply been redistributed among fewer players.

If a single large lender repeats Celsius’s mistakes, the fallout could be worse this time. There are fewer competitors left to absorb the shock.

Why institutions still choose CeFi

For all its risks, CeFi remains attractive to institutional money. The reason isn’t emotional, it’s operational. Institutions know how to deal with centralized counterparties.

They value regulatory clarity, with KYC and AML baked into every transaction. They rely on qualified custodians such as BitGo and Zodia/Fireblocks to safeguard assets under licensed frameworks.

They want flexible loan structures that DeFi’s rigid smart contracts can’t yet match. And most importantly, they want execution speed to ensure instant settlement across large volumes without waiting for block confirmations.

So, for corporate treasuries and hedge funds, CeFi feels familiar. It behaves like traditional finance, only faster and yield-generating. But that comfort can be misleading. The same opacity that retail users fled in 2022 still underpins institutional CeFi today.

What users demand from CeFi now

Based on the evolving market dynamics since the last crisis, user expectations appear to have shifted significantly. The focus now appears to have moved from chasing yield to securing access, speed, safety, and clarity above everything else.

Security and rehypothecation risks

Security sits at the core of user concerns. Rehypothecation remains the single biggest threat because it transforms user collateral into leverage for the platform. Lenders such as Nexo, Salt Lending, Strike, and Ledn continue to state openly that they may reuse deposited assets.

A few providers, however, seem keen on steering clear of that practice entirely. These platforms, CoinRabbit among them, have a stated policy of keeping client funds segregated and untouched.

These platforms take the opposite stance. They do not use client funds for any purpose.

CoinRabbit, for example, explains that avoiding rehypothecation isn’t just a choice but a principle that defines trust itself.

“The absence of rehypothecation is vital for the entire market,” its team notes. “User assets must remain secure.”

“CoinRabbit’s top priority is user security. We clearly understand that the absence of rehypothecation is vital for the entire market, which is why we openly state that we do not use client funds. We believe that as the market grows, more CeFi platforms will follow this simple rule – user assets must remain secure.”

— Irene Afanaseva, CMO at CoinRabbit

Clients increasingly agree. Across surveys, users highlight asset segregation and transparent custody as non-negotiable. Without those, CeFi’s reputation can unravel with every negative headline.

Speed and user experience

DeFi protocols like Aave and Compound issue loans in seconds. CeFi still lags behind, with average processing times between 24 and 48 hours because of manual KYC checks and liquidity reviews.

That delay matters. In fast-moving markets, even an hour can separate profit from loss. CoinRabbit, for instance, claims to have cut issuance time to around ten minutes, offering near-instant liquidity without compromising verification.

Strike has also improved its processing flow, but most competitors remain stuck in slower frameworks.

Efficiency is no longer a luxury in CeFi, it’s survival. Users now equate response time with credibility.

Opacity and lending clarity

Transparency, or the lack of it, remains CeFi’s defining weakness. Few platforms share loan-to-value ratios, liquidation logic, or fee formulas. Before its collapse, BlockFi became the textbook example of what happens when platforms change rates without explanation.

DeFi flipped that standard. Everything is on-chain, public, and auditable. In CeFi, however, users must trust press releases instead of code. The contrast grows starker each quarter, and with it, user patience wears thinner.

Without open reporting, even minor volatility can trigger panic withdrawals. People don’t flee because they expect losses — they flee because they can’t see what’s happening.

Predictability of liquidations

Liquidation rules differ widely across CeFi platforms, and that inconsistency often leaves users unprepared. Many borrowers have faced losses after abrupt margin calls with little or no advance notice.

Thresholds differ dramatically — for example, 12 hours on some platforms, 48 hours on others, which ends up creating uncertainty during volatile market swings.

Platforms like CoinRabbit approach the issue with more active communication. They use multi-channel alerts across email, SMS, and Telegram, alongside real-time monitoring for larger accounts.

They also promise to contact clients directly when positions approach risk thresholds to reduce the chance of avoidable liquidations. That kind of proactive oversight is still uncommon in CeFi, but it’s increasingly what users expect.

Jurisdictional and regulatory risks

Regulation remains the final hurdle between CeFi and full recovery. The sector operates across fragmented frameworks. For instance, MiCA in Europe, SEC oversight in the US — each with its own interpretation of custody, lending, and digital assets.

Complying with multiple jurisdictions is expensive and complex. Larger firms can handle it; smaller ones can’t. As a result, consolidation deepens. Some players, meanwhile, still fail to disclose critical details about their rehypothecation policies, leaving clients uncertain about the true status of their assets.

This mix of opaque disclosure and inconsistent rules makes CeFi’s promise of stability conditional at best. For global users, it means risk now depends as much on geography as on the platform itself.

When scale becomes a liability

CeFi’s concentration doesn’t just limit choice; it reshapes the entire market. Fewer players mean fewer incentives to innovate, slower product cycles, and little pressure to improve transparency.

Limited innovation: Giants like Tether and Nexo have no reason to overhaul systems that already generate reliable profit. Smaller firms lack the capital to challenge them.

Risk homogenization: Similar business models across top lenders create correlated vulnerabilities. If one faces a liquidity crunch, others are likely exposed to the same triggers.

High entry barriers: The cost of regulation and capital reserves discourages newcomers, reducing diversity in models and risk tolerance.

Restricted credit supply: Institutions needing large-scale liquidity have no real alternatives. They must go to the same three providers, which can adjust rates unilaterally.

The road to safer CeFi

To cut a long story short, CeFi’s rebound is real. However, resilience is not the same as safety. The market looks healthier because it’s smaller, more regulated, and numerically growing again. But those metrics mask unresolved structural flaws.

Ultimately, the right approach for CeFi would be to rebuild trust from the ground up. Even if that means abandoning rehypothecation, enforcing strict segregation of user assets, and publishing transparent lending metrics that mirror the clarity of DeFi. It also means designing liquidation systems that protect clients rather than surprise them.

CoinRabbit illustrates what that future could look like: funds kept offline in cold storage with multisig access, no collateral reuse, and real-time withdrawal access. Its model shows that security and accessibility can coexist without compromise.

The broader industry, however, remains split. Many platforms still see rehypothecation as necessary for profitability. Until that changes, every market rally carries the risk of another unwinding.

CeFi has proven it can survive. The next step is proving it deserves to.