A European Central Bank Executive has described key problems with the current cryptocurrency state that could potentially burst the “bubble.” However, crypto’s role in digital finance will likely continue to evolve.

In 2022, a growing debate over the rise and the subsequent crash of the crypto market was triggered by a number of unfortunate events. While some promising developments support the furtherance of crypto utility, the collapse of big players in the space has spooked the public.

This article discusses a range of topics, from crypto’s potential as the future of finance to some calling it a bubble about to burst. What does the future hold for digital finance as a whole?

Crypto and Finance

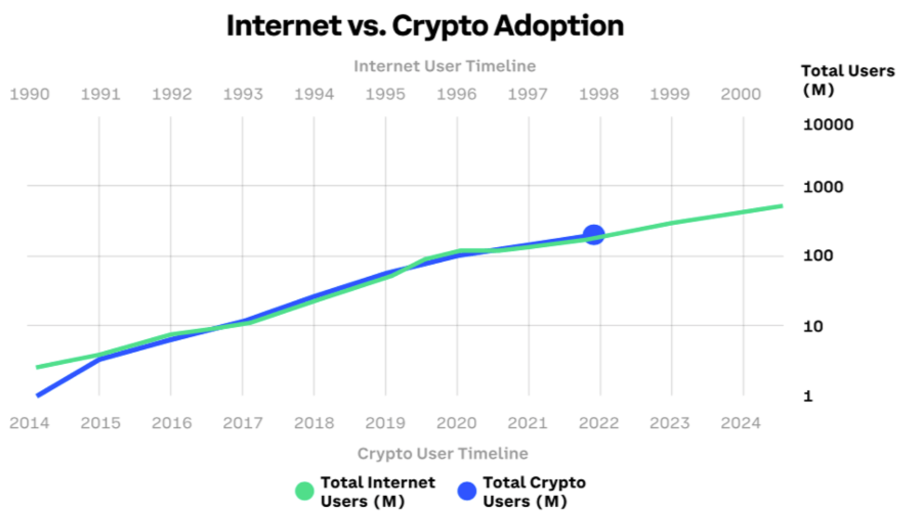

Why is cryptocurrency so exciting? Like any new technology, some see the potential, while others need a little more time to be convinced. Think about the internet in the 80s and the 90s. There was a time when people were scared to shop or bank online.

But now that technology drives everything. Most cryptocurrencies aim to be a fast, cheap, and easy-to-use digital currency that is accessible by anyone in the world with an internet connection.

Many cryptocurrencies are decentralized and thus less influenced by central governments. This can provide many people living in challenging jurisdictions with an alternate form of financial independence.

Many Fortune 500 companies such as Starbucks, Tesla, Burger king, Coca-Cola, and many more already accept crypto as a form of payment. Crypto is beginning to move into day-to-day lives as a payment mechanism.

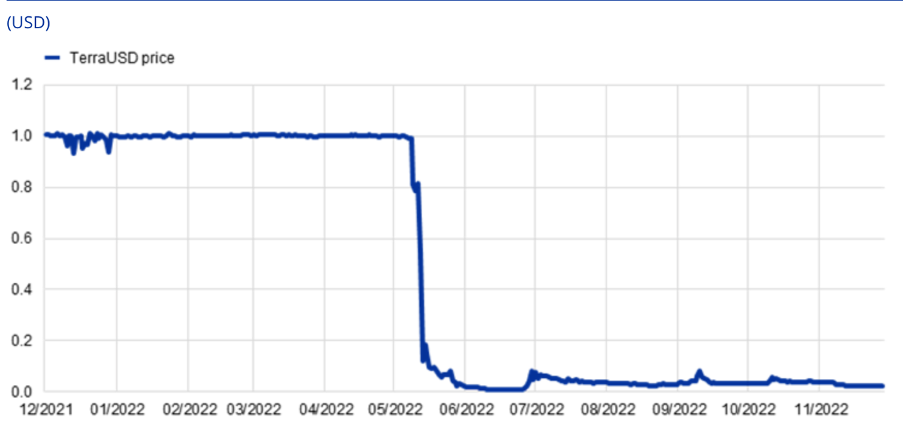

That said, it remains a niche sector that is evolving with time. But even evolution can bring about setbacks. 2022 saw a strong domino effect in play for cryptocurrencies. Big names caused widespread damage due to greed and shady business practices. These include Terra and its UST stablecoin and the FTX crypto exchange, which contaminated more than 100 other businesses after it went insolvent.

Crypto Domino effect: One Failure After Another

One of the main setbacks for the crypto market is the increasing connectivity and leverage pain points. Thus giving rise to a domino effect.

One of the year’s first big crypto crashes was Terra. Many regarded it as one of the safest crypto ecosystems. But the price of its LUNA token crashed in tandem with its connected stablecoin, Terra USD (UST), after it lost its peg to the dollar.

This crash set forth a chain of dominoes that caused massive distrust in cryptocurrency as a whole.

Next came Celsius, a well-known crypto exchange and one of the biggest crypto lenders. But after the Terra fiasco, it too started seeing massive withdrawals. Celsius did not have enough collateral to back each loan, and the jig was up.

After Celsius, Three arrows Capital (3AC), another crypto lender, faced the same issues, which affected Voyager capital, a crypto company it had borrowed from. They have all now filed for bankruptcy, further reducing investor trust.

Similarly, the collapse of FTX in November caused a ‘contagion effect’ that caused more than 100 linked companies to file for bankruptcy or eat heavy losses.

Structural weakness

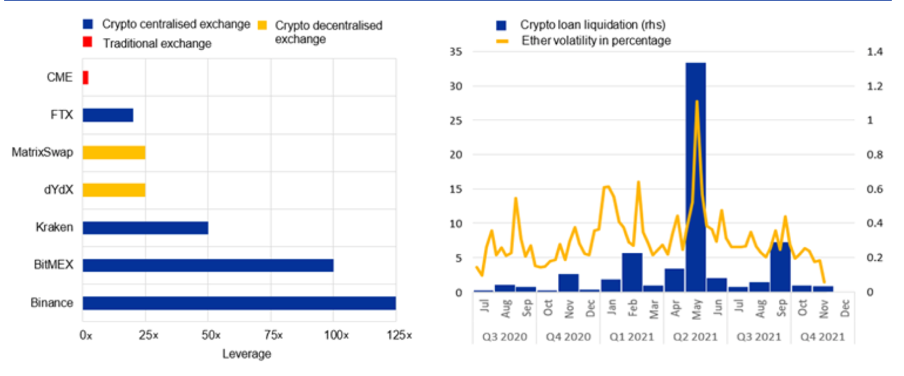

Crypto markets remain highly leveraged and interconnected leading to strong procyclical effects, given the lack of shock absorption. Here’s a practical example to support this scenario:

Some crypto exchanges allowed investors to increase their exposure by more than 100 times their actual investments. Ergo, when a fall/shock hits, deleveraging is required. Exchanges are required or forced to shed assets, putting intense pressure on crypto prices, as seen in the graph above.

Speaking on this matter is Fabio Panetta, a member of the executive board of the European Central Bank. Panetta’s quotes while speaking at the Insight Summit held at the London Business School on Dec. 7 were shared with BeInCrypto.

Panetta stated:

“Funds borrowed in one instance can be reused as collateral in subsequent transactions, allowing investors to build significant exposures. Shocks can propagate rapidly across collateral chains and are amplified by positions liquidated automatically using smart contracts.”

He further added that more support is needed for regulations within the crypto market:

Mitigating risks

European and U.S. politicians especially have called for urgent regulations, especially after the FTX fiasco.

In addition, Panetta also aired his thoughts regarding the taxation of cryptocurrencies. Specific to Europe, introducing tax could help facilitate the finance of goods and services.

For instance, leveraging tax measures could curb the high energy extensive costs related to crypto mining. He concluded his speech by saying that he wants to ban energy-extensive crypto assets with carbon footprints — hinting toward crypto assets with a proof-of-work consensus like Bitcoin.

A Balancing Act

These narratives from an executive at one of the world’s most important central banks have rightfully spooked those with significant portions of their wealth in cryptocurrency.

But at the same time, banking systems have no shortage of problems and drawbacks.

When discussing the future of digital finance and crypto, it’s essential to assess the status quo of traditional money systems. Banking might seem inexpensive if one is wealthy, but it’s pretty expensive for the average person.

A McKinsey report shows that the average U.S. household spends $2,700 per year on banking services, equal to about 3.5 weeks’ worth of pay a year.

So the average person in America spends more money or more time working to pay for the right to use banking than they’re paying for their state taxes in some cases.

Digital finance and cryptocurrency address two things in the financial system.

First, replacing the cost of trust from traditional financial institutions. That’s the bulk of why banking is so expensive. One uses a trusted intermediary between two parties, while blockchains decentralize that trust and drop the cost enormously.

They also help in optimizing working capital for businesses. Today, the average S&P company keeps roughly 14% of its cash on its balance sheet. Digital finance frees up this working capital since one no longer has to transact in currency, thereby improving the productivity of money.

But, as innovation progresses, can crypto play a significant role in the domain of digital finance?