Dive deep into the world of decentralized finance as we sit down with Georgy, the Co-Founder & Head of Partnerships at Wirex, for an enlightening AMA session!

From the revolutionary new Wirex Pay app to its integration with giants like Visa and Mastercard, we’re uncovering the nuances of next-gen payment systems. Ever wondered about the strategic choice behind adopting the Polygon CDK? Or how traditional and decentralized financial systems are merging for a more cohesive experience?

Stay with us as we explore these topics and delve into community-curated questions that tap into the heartbeat of the blockchain universe!

AMA Wirex and BeInCrypto

BIC: We’re getting ready for our AMA session! Take a comfortable seat and follow our conversation in few minutes 🛋

Today we welcome Georgy who is Co-Founder & Head of Partnerships at Wirex in our AMA today.

I’ll have 9 questions for Georgy. After that, he will answer the 5 (or more) most interesting questions from you.

BIC: Georgy, I’ve heard about your new app Wirex Pay. Please tell us about it. What is the Wirex Pay network? And what are its key features?

Georgy:

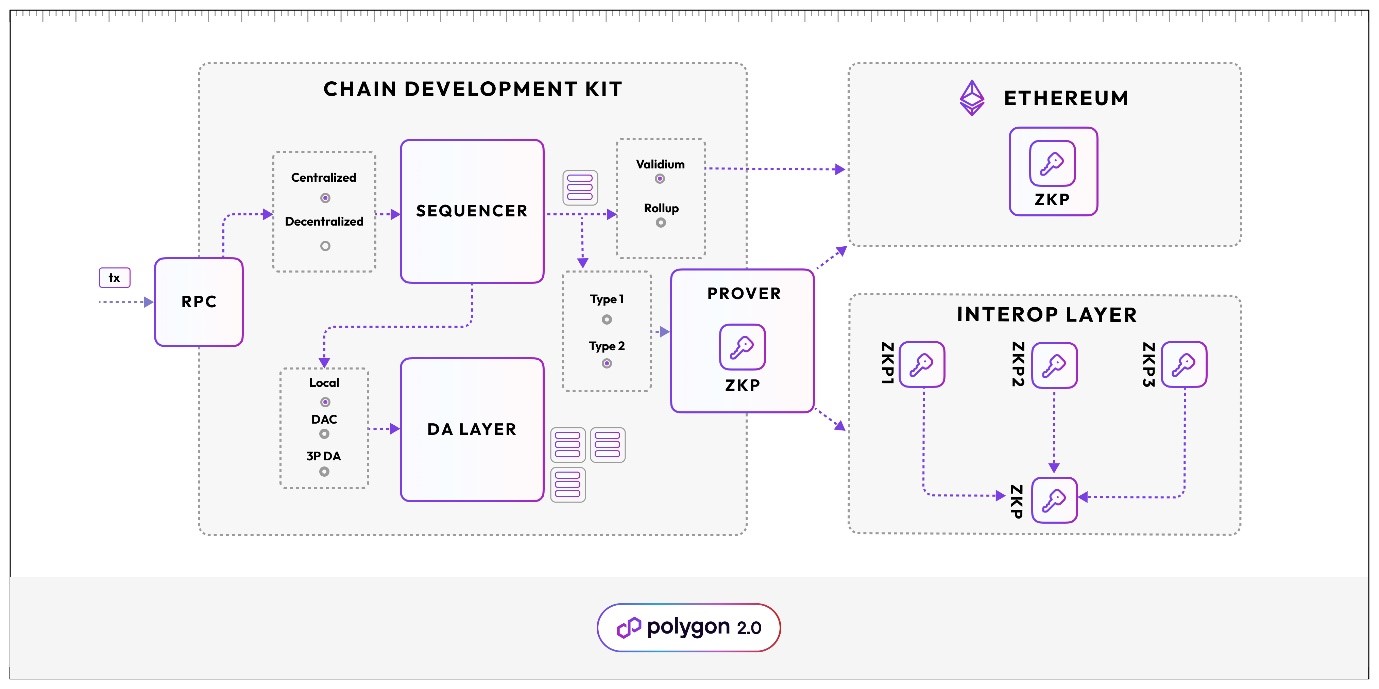

Wirex Pay network is a payment-focused app chain, developed with the Polygon ZK CDK (Chain Development Kit), and directly integrated with Visa/Mastercard through Wirex.

Key Features of Wirex Pay:

- ZK-Powered Technology: Ensuring swift and secure transactions through the integration of Zero-Knowledge technology.

- EVM Compatibility: Tailored for seamless integration with the Ethereum Virtual Machine, promoting diverse functionalities and interoperability.

- Account Abstraction (AA): Streamlining transaction processes by eliminating inherent complexities, enhancing user experience.

BIC: And why did Wirex choose Polygon CDK?

Georgy:

The decision to adopt Polygon CDK for the Wirex App Chain was influenced by the platform’s unique value propositions:

- Scalability and Security: Polygon’s ZK technology ensures that chains built using the CDK are not only scalable but also maintain the highest levels of security.

- Sovereignty with Interoperability: While each chain retains its sovereignty, the shared ZK bridge ensures seamless interoperability, connecting every chain to one another. This interconnectedness forms the value layer of the internet, allowing for fluid transactions and interactions across chains.

- Access to Massive Liquidity: Chains participating in the ecosystem benefit from the vast liquidity across all networks, ensuring users and developers have ample resources for their operations.

The selection of Polygon CDK for the Wirex App Chain was a strategic move to harness the power of ZK technology, ensuring scalability, security, and seamless interoperability.

There was a period in time (quite expectedly, during the bull run) when the choice of tech stack would often be determined by the various incentives and grants, rather than the technology itself.

Whereas this still exists, one of the unobvious benefits of being in the bear market is that with less money to burn, businesses focus more on the bottom line and ensuring the technology is fit for purpose, to make the product or offering fast, secure and appealing enough to users rather than choose the one offering the highest incentives/budgets.

BIC: As you said before, Wirex Pay is compatible with Visa and Mastercard. I am sure that this fact inspires confidence and arouses interest in cryptocurrency among “ordinary people”.

Georgy:

Yes, Wirex Pay is seamlessly integrated with both Visa and Mastercard, enhancing the universality and accessibility of our services. Utilising its near-instant transaction finality, Wirex Pay is engineered to process thousands of transactions per second efficiently. This integration not only strengthens the convergence of traditional and decentralised financial systems but also underscores our commitment to providing versatile, swift, and secure payment solutions to our esteemed users globally.

As one of the first crypto cards to have successfully launched at scale as early as 2015, and now Principal Member of both Mastercard and Visa (still the only crypto-native company in the world to get there!) Wirex is ideally positioned to make that connection.

BIC: Our usual question to speakers: What makes Wirex Pay secure and decentralized?

Georgy:

Wirex Pay, functioning as a Layer 2 on Ethereum, enhances security by facilitating gasless transactions and achieving almost instantaneous payment finality. It supports direct wallet-to-wallet transactions without the need for KYC, courtesy of its innovative AA (Account Abstraction) implementation, ensuring a trust-enhanced environment.

Wirex Pay’s open network design ensures seamless integration with various wallets, conventional financial systems, and diverse payment schemes, thanks to its unique features including ZK-Powered technology and EVM compatibility.

BIC: After our previous AMA-session, we received this question from our members, so I need to ask: Who is the Issuer of the Cards?

Georgy:

The cards are issued by Wirex – unlike many, or rather most, players in the space, we are able to issue cards directly, without relying on any intermediaries. Wirex made a significant mark in the industry by introducing the first crypto-enabled card as early as 2015.

To be more precise, it was a Bitcoin pre-paid card, not ‘crypto’, as even Ethereum didn’t exist yet. As a principal member of both Visa and Mastercard, Wirex is trusted and recognised for its innovation and reliability, and undergoes regular audits by multiple 3rd parties.

BIC: Since the collapse of FTX, non-custodial crypto wallets have become even more popular among investors and traders. What are the main features of the non-custodial debit cards?

Georgy:

The key features include:

- Smart Contract Integration: Enables non-custodial use, providing users full control over their funds.

- Direct Spending: Allows for immediate crypto and stablecoin transactions without the need to pre-load the card.

- Zero FX Fees: No foreign exchange fees, ensuring cost-effective international usage.

- Crypto Cashback: Earn crypto rewards on every purchase made.

- Free ATM Withdrawals: Up to $300 free withdrawals monthly, enhancing cash accessibility.

BIC: What benefits does the Wirex Pay product suite extend to users?

Georgy:

The Wirex Pay Card facilitates self-custodial spending of cryptocurrencies globally, wherever Visa/Mastercard is accepted. Users are empowered with the ability to invest in and trade digital assets instantly and take advantage of decentralised lending and borrowing services. Wirex Pay is built on the robust ZK-powered App Chain, ensuring transactions are swift, secure, and user-centric.

By harnessing the capabilities of ZK (Zero-Knowledge) technology and EVM (Ethereum Virtual Machine compatibility), Wirex Pay integrates seamlessly with the traditional financial ecosystem while maintaining the decentralised, secure, and user-empowering principles of blockchain. Users retain full control over their assets, ensuring a secure and compliant interaction with the decentralised finance (DeFi) world and mainstream economy.

BIC: I believe it’s one of the most interesting questions for the Community: Is it possible for DAOs to utilize Wirex Pay cards for expense management and salary disbursements?

Georgy:

Certainly. Wirex Pay caters to both individual and corporate needs, including those of decentralised autonomous organisations (DAOs). Our non-custodial corporate cards streamline expense payments and payroll processes, ensuring efficiency and security in financial management for on-chain organisations.

We have been offering Wirex cards to employees and contributors of a number of partner projects in the space, such as Maker or 1inch, but that is the ‘ordinary’ crypto card, linked to the custodial Wirex payment app. Now we are about to take this to a whole new level.

BIC: The last question from me: How will the WXT token be integrated into the forthcoming Wirex Pay ecosystem?

Georgy:

WXT stands as a fundamental element within Wirex’s payment infrastructure. As we anticipate the integration of our 6 million customers into the blockchain through Wirex Pay, WXT’s role is set to be pivotal. We are committed to embedding WXT profoundly within the Wirex Pay network, and detailed use cases explaining its application in facilitating payments will be unveiled later this year as we approach the launch of Wirex Pay.

BIC: Now let’s move on to questions from our community that we collected in advance! The first one is by @Pepayacc:

Can you provide specific examples of use cases where Wirex anticipates Wirex Pay revolutionizing cross-border payments, and how does this align with Wirex’s vision of redefining the global financial landscape?

Georgy:

Absolutely – love specific examples 🙂

A few months ago we enabled our users in Brazil to top up their Wirex accounts, as well as buy, exchange and sell crypto and traditional currencies directly from/to their local bank accounts – in partnership with Transfero, utilising their fully backed Brazilian real BRZ stablecoin in the background.

So, as one possible use case, a Brazilian family sending their kid to study in Europe or Hong Kong, or US, etc. can seamlessly send money to the student’s Wirex account, and he or she can seamlessly spend it with their Wirex card that they order when settling down in Europe/Hong Kong/US/etc. Such transfers are virtually instant, and currencies are exchanged in the background at interbank rates, so there are minimal losses along the way, unlike using more traditional remittance methods.

Now, with Wirex Pay enabling cards linked to non-custodial wallets, this process will become possible for customers who want to maintain self-custody of their crypto funds..

BIC: @Anakbiskuat0006 asks:

In terms of user education and adoption, what strategies does Wirex have in place to ensure that users of varying technical expertise can effectively utilize the advanced features of Wirex Pay, and how will Wirex measure the success of these efforts?

Georgy:

From the outset, our big focus was on convenience and ease of use. However great a new technology, adoption will be slow and limited if it is too difficult for an average consumer.

That is why, back in 2015, when trying to tackle the problem of merchants not accepting Bitcoin as payment, we decided to give Bitcoin holders a familiar and convenient tool – a debit card that allowed them to spend their coins anywhere Visa or Mastercard are accepted.

Today, we still try to make using Wirex as easy and familiar to any ‘common’ fintech/banking app as possible. You can start using it without knowing about or touching crypto. Just use your Wirex card for your daily expenses, and earn CryptobackTM (cashback in crypto) on every transaction.

Your high street bank will not offer that. And then, at some point, those rewards will accumulate to a notable amount, and you will wonder, hm, what’s that WXT that I have earned? And what’s Ethereum? Etc, etc. We try to make the educational process natural, rather than imposed.

And, of course, we will always try to explain all the new features such as Wirex Pay, as well as address more general questions about blockchain and crypto in our blog, on Discord, etc.

A good measurement of success of the efforts to explain and promote Wirex Pay will be the number (or percentage) of the new non-custodial cards that customers order and use.

BIC: The next one… by @Algojali:

I’m interested in Wirex Pay’s role in the broader Web 3.0 ecosystem. Can you provide an example of how Wirex Pay might interact with other decentralized applications or platforms to create a holistic user experience?

Georgy:

In the interest of time, will give just one brief example, although there can be many more.

Let’s say, now you have ETH staked on Lido. Or some other asset locked in Maker vault to generate DAI. On Ethereum. You are earning your yield, but that’s about it – not much more you can do with those staked or locked funds, and transactions on Ethereum are slow and expensive.

Now, with Wirex Pay, linking liquidity on any EVM compatible chain to the ‘real world’ financial system (Visa, Mastercard, IBAN’s, etc) via the new app chain (with fast and cheap transactions) you would be able to use that DAI to pay your rent via SEPA, pretty much directly from your self-custody wallet. Or use those funds staked on Lido as collateral for a loan to take out on Wirex and spend it with your Wirex card.

This won’t come straight away upon launch, probably will be added in the 2nd or 3rd iteration of the product, but you get the idea.

BIC: @aerowoLfd wonders:

Can you tell me about KYC , Do I need KYC to deposite and withdraw from WIREX wallet? Also Do you accept KYC from all over world? Considering that you have a large number of opponents, can you share with us a few killing features that make you superior to them? What are strengths that enable you to look to the future with hope?” “

Georgy:

Firstly, let’s make a distinction between the custodial Wirex App (the neo-banking/payment app with the card, IBAN’s, etc.) and the non-custodial Wirex Wallet.

Obviously, the former would require 100% KYC to even start using the app. We accept users from over 130 countries, but the set of features will be different across those countries. The most advanced offering, including the card is available in Europe and UK (together with , IBAN’s, and various fiat on-ramps), several countries in the APAC and in the US.

The latter is available globally, and no KYC is required, as it is a self-custody wallet. What makes it different and easier to use than most competing products, is that you don’t have to remember or store your private keys or seed phrases. Using MPC-technology, it is possible to recover access to your wallet via a sophisticated face scan – should you lose your phone.

This non-custodial wallet will have a card linked to it soon, too – thanks to the new app chain we are building. But to get access to the card (or fiat overall), you would need to do KYC – there is just no way to get around that it today’s financial world. At least, not for a compliant and regulated business like Wirex.

BIC: The next question – @sallybyterin12 wants to know:

Given the expansion of virtual card availability to the UK, EEA, and Australia, can you provide specific adoption statistics or projections for each region? Are there any geographical variations in virtual card adoption rates or usage patterns that the Wirex team has observed, and how do you plan to address them?

Experienced team is the most vital thing in building company growth, a project will not develop without being managed by an experienced team, whatever it is good. so, how about project? does your team have good experience in the cryptocurrency world?” “

Georgy:

Historically, EEA and UK have been our strongest region. However, since the launch of the card in Asia Pacific about 3 years ago, it has grown from a subsidized region to about 30-35% of our user base and volumes.

Wirex has a diverse team with decades of experienced in traditional finance, fintech and crypto – you can check out the LinkedIn profiles for yourself.

BIC: Georgy, we’re done, but we still have time – you can answer other questions from the community!

Georgy: …

BIC: @amirzakirr asks:

Many Wallets currently offering referral program Is there any referral system offered by Wirex wallet where we can invite our friends and get trading fees refferal bonus or any discount ? ”

Georgy:

We do offer a referral programme with unlimited bonuses. Check it out here.

BIC: @aby717:

Has there been a security audit done on wirex? Is there a report we can check out? “

Georgy:

Firstly, let’s get things straight with the definitions. There are blockchain / token / smart contract audits done by the firms like CertiK, PeckShield, etc. WXT has been audited by CertiK, which you can check here.

Then if we talk about the Wirex app, being a regulated financial institution, we are being evaluated and regularly audited by multiple parties: regulators themselves, appointed certified auditors on the financial side, on the tech side, PCI-DSS, etc, etc. You don’t want to know how much effort and resources are devoted to those – obtaining and maintaining licenses does not come easy or cheap.

Those auditor reports are generally not public and only shared with relevant and qualified 3rd parties.

BIC: @AbiBR6:

The elimination of upfront prepayment in payments using Wirex Pay is intriguing. Could you delve deeper into how this process works and what it means for user control and transaction security?

Georgy:

For the user it means that you won’t have to pre-fund the card, neither will you have to worry about giving up custody of your funds, except for the amount used for the actual transaction.

Security is enabled by the EVM compatible ZK-powered app chain.

BIC: @Hand2003 :

Can you list 1-3 attractive features of Wirex that make it superior to its competitors? What competitive advantage does your platform have that you are most confident about?” “

Georgy:

- Multi-currency card, helping you save on fx. Wirex is the direct issuer, being a principal member of both Visa and Mastercard (the only crypto native company globally to have both)

- Wirex combines the best of both worlds – pretty much a fully functional personal banking app (although technically we cannot call ourselves a bank, rather an e-money licensed institution) offering a variety of traditional payment rails (card, individual IBAN’s, etc) combined with the fully functional crypto wallets, allowing you to deposit, withdraw, store, exchange, buy and sell crypto.

- Now, with Wirex Pay we will be able to combine that versatile neo-banking offering with self-custody wallets

BIC: Let’s choose the last question. @Dev2023:

In light of the standard criticism that the cryptocurrency market is more speculative and unstable compared to established financial markets, what is your company’s stance on this issue? Additionally, does your company have a dedicated core team to oversee the constant upgrading process of the UI of the Wallet app?

Georgy:

Couldn’t agree more. That is why we have always been focused on the real world use cases. Payments. Remittances. High yield accounts and loans. And, of course, the exchange and trading functionality, which you just have to offer in this space.

90%+ of our platform is built in-house, and we have a core team of 100+ developers, testers, designers, etc. to maintain it and constantly improve.

BIC: Great! Thank you, Georgy for having time today!

Conclusion

From our deep dive into the world of NFTs to exploring the nuances of modern tokenomics and unpacking the challenges and opportunities of regulatory changes, this AMA session with Georgy has now come to an end. In our journey through the insights of Georgy, we’ve glimpsed the horizon of a financial world in transition. Wirex isn’t just observing this change; it’s actively shaping it.

Are you ready to be part of this new wave? Dive into the Wirex universe yourself via this link and be part of the financial revolution!

Disclaimer

In compliance with the Trust Project guidelines, this guest expert article presents the author’s perspective and may not necessarily reflect the views of BeInCrypto. BeInCrypto remains committed to transparent reporting and upholding the highest standards of journalism. Readers are advised to verify information independently and consult with a professional before making decisions based on this content. Please note that our Terms and Conditions, Privacy Policy, and Disclaimers have been updated.