On September 11, the UK Parliament introduced the Property (Digital Assets etc) Bill. This Bill designates digital assets, including cryptocurrencies, non-fungible tokens (NFTs), and carbon credits, as personal property under British law.

The legislative initiative fills previous legal voids and strategically places Britain at the forefront of the global crypto race. By legally recognizing these assets, the UK aims to solidify its leadership in the digital assets sector.

UK Moves Towards Clear Crypto Regulations

Previously, the absence of explicit recognition for digital assets in English and Welsh property law left owners and investors in a precarious position, especially during disputes.

The new law promises protection against fraud and scams, enhancing security for individual asset holders and companies. Additionally, the Bill might assist judges in resolving complex legal disputes involving digital assets, such as those in divorce settlements.

Read more: Crypto Regulation: What Are the Benefits and Drawbacks?

Justice Minister Heidi Alexander stressed the importance of adapting laws to keep pace with technological advancements.

“It is essential that the law keeps pace with evolving technologies, and this legislation will mean that the sector maintain its position as a global leader in crypto assets and bring clarity to complex property cases,” Alexander remarked.

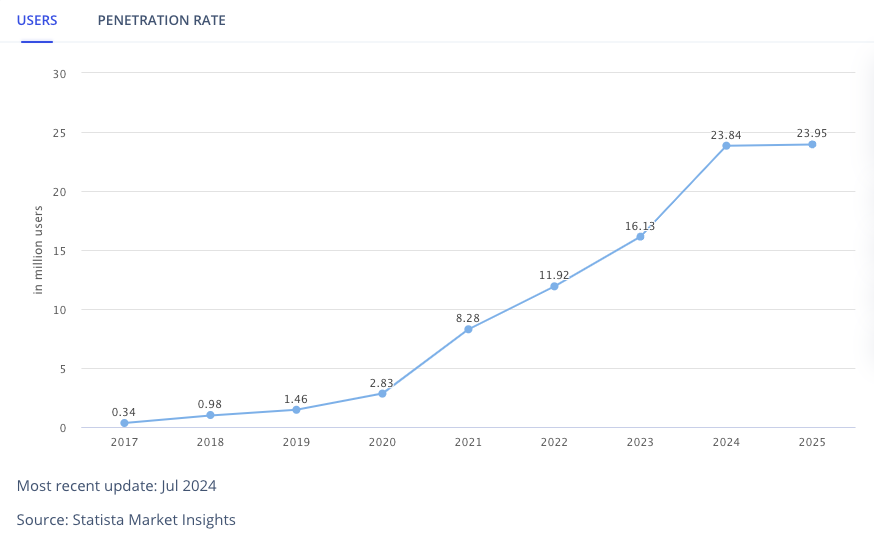

According to Statista, the UK has over 23.84 million crypto users as of July 2024. Hence, the need for a clear regulatory framework is more pressing than ever.

“This is a welcome development that is important for UK courts dealing with UK law contracts, a lot of which are struck overseas. Residents of the UK have had access to BTC and ETH ETFs for some time now – albeit not within their Pensions or ISAs – so we don’t foresee a large impact there,” Nicolas Streschinsky, Head of DeFi at Trilitech, told BeInCrypto.

Furthermore, the legal recognition of digital assets is anticipated to yield significant economic benefits. By fostering a more secure and legally sound environment, the UK is poised to attract more business and investment into its legal services sector.

Following the 2023 Law Commission report’s recommendations, this legislative development highlighted challenges in recognizing digital assets as property. The report clarified that digital assets, while not fitting traditional legal categories, can nonetheless be treated as personal property. This new category, termed “third category things,” includes digital objects and other intangible assets like certain carbon emissions allowances.

“We conclude that the common law is the better vehicle for determining those things that properly can (and should) be objects of personal property rights, and which fall within the third category: third category things,” the report mentioned.

Read more: Crypto Tax 2024: A Complete UK Guide

Although many have applauded this legislative step as progressive, others remain skeptical.

“This is simply so they can tax it easier,” an anonymous user on social media platform X, commented.