There are many ways to value a blockchain, from total value locked to discounted cash flow. Another popular method — Realized Extractable Value — has been the subject of debate among crypto communities in 2026. This guide covers what Realized Extractable Value (REV) is, how it is measured, and whether it is a good valuation metric for blockchains.

KEY TAKEAWAYS

➤ Realized Extractable Value (REV) measures the actual profits from MEV strategies, including validator fees, and offers a more grounded view than theoretical MEV alone.

➤ REV is controversial because it’s increasingly used as a valuation metric, despite being originally designed as a measurement tool — not a predictor of long-term value.

➤ High REV may reflect inefficiencies, speculative activity, or immature infrastructure rather than sustainable economic strength.

➤ REV should be evaluated in context, alongside other valuation frameworks, as no single metric can fully capture a blockchain’s value.

What is Realized Extractable Value?

Realized Extractable Value (REV) is a metric used to quantify the total amount of value that users pay to a blockchain. It is the actual value extracted from MEV opportunities, as opposed to the value extracted by a MEV opportunity alone.

Quick definition: MEV — Maximal Extractable Value, sometimes called Miner Extractable Value — is the maximum amount of value miners or network validators can extract by rearranging and reordering network transactions waiting for confirmation.

REV includes the real-world factors that impact the profitability of MEV strategies. These include:

- Network conditions

- Priority fees to validators/miners

- Transaction costs

- Gas costs

If this sounds confusing, don’t worry; the concept, in reality, is actually really simple.

REV = MEV profit + profit made by validators/miners

or

REV = profit (MEV profit – costs (exchange trading fees/flash loan fees)) + validator fees (transaction priority fees + gas fees)

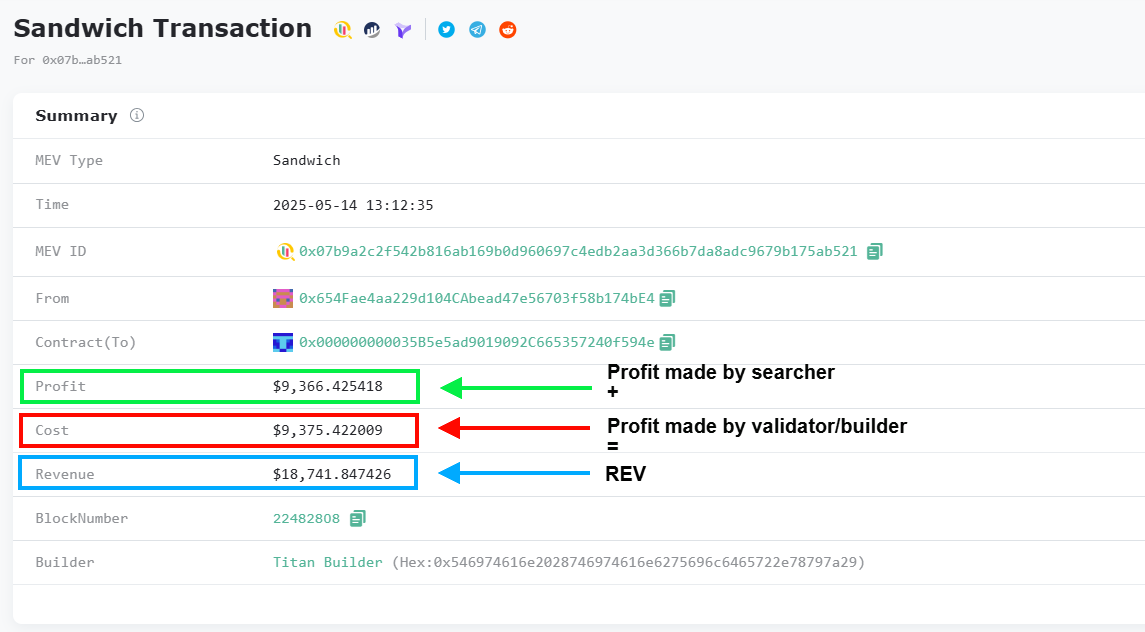

Let’s take a MEV sandwich attack as an example. In a sandwich attack, “searcher A” inserts a transaction before and after someone else’s transaction to make a profit. This is the MEV opportunity.

Hypothetically speaking, let’s say multiple searchers are competing for this same opportunity. The validator will have to decide who wins this opportunity.

Therefore, searcher A will send more value to the validator than is actually required, in order to execute the transaction by gas fees alone. This is sort of like a bribe from searcher A to ensure the validators includes their transaction into a block before the other transactions. If searcher A wins the bid, they make the MEV profit.

REV includes the “bribe” to the validator (gas fees + bid), plus the profit made by searcher A (the MEV opportunity). You can see this real-world example in the image above.

REV vs. MEV

Maximal extractable value (MEV) is any profit opportunity that someone extracts by reordering, inserting, or censoring transactions or blocks, without hacking or breaking the rules of the protocol or application.

Searchers create these opportunities through clever strategies. They are not just limited to classic examples like arbitrage or sandwiching, but potentially new methods that emerge from the structure of the system itself.

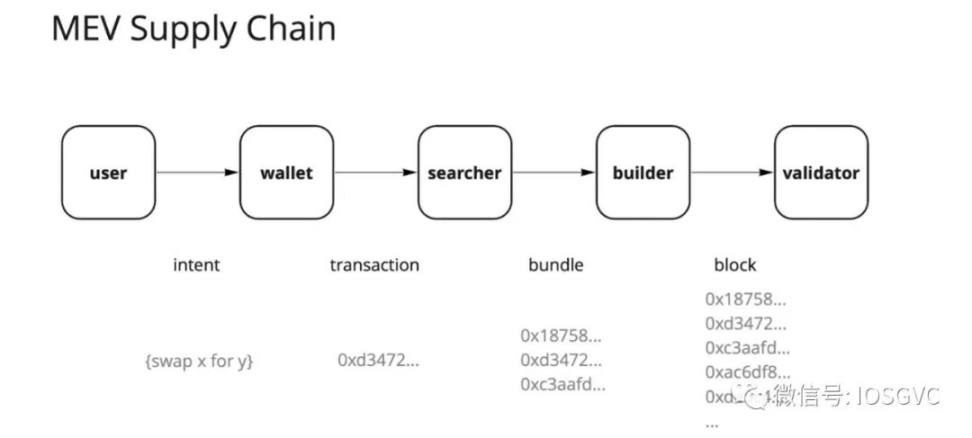

To properly understand REV, it is important to be aware of the life cycle of a MEV transaction on a blockchain. A searcher is someone (usually a bot) that captures profitable MEV opportunities (e.g., arbitrage, liquidations, sandwich attacks).

Once the searcher generates a transaction to capture this opportunity, they must get it included in a block on the blockchain. A validator picks up this transaction for a fee. In this scenario, there are two fees: the cost for actually executing the transaction and the cost for including the transaction in a block.

Think of it this way. You have a very popular product or service (block space), but its quantity is limited. If you accept a customer’s business (a transaction), it will cost you to accommodate them (the cost to execute the transaction). However, you have more customers than you can accommodate (multiple searchers competing for the same MEV opportunity). If someone wants this product or service (inclusion into the block), they must pay a priority fee (the cost for including the transaction in the block).

REV includes the profit made from the MEV opportunity, plus the costs they paid to the validator to execute the transaction. Many people extrapolate this to mean the costs borne by users, as MEV typically comes at the expense of users, and the searchers are technically users themselves (paying for block space).

Why is Realized Extractable Value controversial?

The article “Quantifying Realized Extractable Value” by Flashbots, published on May 15, 2021, is the earliest comprehensive and formal account of the concept of REV. The topic has gained traction in recent years and has sparked debate on X (formerly Twitter) — technically and politically.

Many question whether:

- REV is a value driver for the layer-1 (L1)?

- Is it the best way to measure value accrual to an L1 token?

- Is it the blockchain equivalent of discounted cash flow (DCF)?

REV is no longer just a technical metric — it’s become a battleground for competing narratives about what makes a blockchain valuable.

Those in favor of using REV as a valuation tool argue that it reflects the economic intensity of a blockchain — the real, dollar-denominated cash flow generated by activity like trading, liquidations, and arbitrage.

However, critics argue that REV is a poor proxy for long-term value, as it often spikes during periods of speculation (like meme coin bubbles) or volatility (wealth effect of the L1 coin/volatility of assets on the chain). Some also note that chains like Bitcoin (with zero REV by design) are still considered extremely valuable.

Should we use REV to value blockchains?

In reality, valuation is a controversial topic, not just for blockchains. As explained by Professor of Finance, Aswath Damodaran:

“Valuation is simple; we choose to make it complex. The second is that every valuation — even though it’s about numbers — has a story, a narrative behind it. A good valuation is more about the story than about the numbers. And third, when valuations go bad, it’s not because of the numbers; it’s because of three big problems I see in valuation.”

Many investors may use REV to value a blockchain; however, this ignores the reason REV initially created. Flashbots developed REV because MEV is a metric that is difficult to measure precisely, given the evolving and unpredictable nature of extraction methods.

When evaluating REV as a valuation metric, several considerations must be kept in mind:

- Mature MEV infrastructure — including order flow auctions (OFA) and app-specific sequencing (ASS) — can compress extractable value and drive fees toward zero. In such environments, high REV might indicate inefficiency, not economic strength.

- Internalized MEV at the application layer (via ASS) can make blockchain-level REV appear lower even when economic activity is robust.

- Most MEV opportunities are highly competitive. In reality, multiple searchers often compete for the same opportunity via priority gas auctions (PGAs) or spamming backrun attempts. In these cases, miners or validators may still profit from gas fees, even when no MEV is actually extracted. Additionally, searchers often run preflights (on-chain checks) that may fail.

The last point, as highlighted in Flashbots’ foundational article “Quantifying Realized Extractable Value” (2021), underscores a key weakness: REV excludes preflight checks, failed attempts, or losses from gas fees on unprofitable MEV strategies. These costs are very real for searchers but are not reflected in REV.

REV, but with context

REV is a way to more accurately measure MEV activity on a blockchain. Before you jump into a project based on its REV, take a minute to understand how we calculate the metric and how it is appropriate to apply it to fundamentals. Because, while REV isn’t necessarily useless, there are many ways to value a blockchain, each of which may provide critical information depending on the context.

Disclaimer: This article is for informational purposes only and should not be considered investment advice. Always do your own research (DYOR).