Bridge Liquidity Paradox: More often than not, TVL is just a vanity metric – bridges should revisit their approach to liquidity aggregation, laying greater emphasis on capital efficiency and dynamic rebalancing strategies, says Ramani Ramachandran and Vatsal Gupta of Router Protocol.

Recognizing the need for a mechanism to port liquidity across blockchains and increase capital efficiency in the system, various cross-chain protocols have come to the fore in the last year. Although the potential of cross-chain infrastructure extends far beyond liquidity migration across chains, it still remains one of their most critical use cases. In fact, several other use-cases of cross-chain bridges, including but not limited to cross-chain yield farming, cross-chain prediction markets, and cross-chain lending/borrowing, rely directly on the bridge’s ability to transfer funds across chains in a secure and efficient manner.

To facilitate fund transfers across chains, the bridges need to maintain sufficient liquidity. But a key question here is what qualifies as “sufficient?” The launch of Uniswap V3 has made it evident that TVL is not the most important metric for a DeFi protocol. The key to running a successful protocol lies not in the amount of liquidity it is able to accumulate but in how efficiently it uses its liquidity – mindlessly giving out millions of dollars in protocol tokens as rewards for attracting more-than-is-necessary TVL often proves to be counterproductive.

This article will explore the shortcomings of approaches to liquidity aggregation currently in vogue across many cross-chain protocols and make a case that TVL is merely a vanity metric, arguing that capital efficiency should be prioritized over TVL.

TVL is Not the Whole Story

The years 2020 and 2021 marked the “Liquidity Era of DeFi” – a time when protocols did not have to worry about anything other than securing liquidity, a time when TVL was regarded as the most crucial measure of a project’s success. During the bull run in the first half of 2021, for example, DEXs with over $200m in TVL were automatically labeled as “doing well” without taking into account other vital metrics such as daily active users, trading volume, and revenue generated, among other things. And while the “Let’s get all the liquidity we can” strategy gained legitimacy in the early days of DeFi, the emphasis on TVL soon became redundant; more and more people started to realize that deeming a protocol’s TVL as the sole indicator of its growth often backfired in the long run. After all, as fundamental as it may be, TVL only portrays a small part of the whole picture – TVL can track how much capital is stored in a contract, but it fails to capture how that capital is used.

Capital Efficiency: A Better Indicator of a Bridge

As the term suggests, capital efficiency is a measure of how efficiently a company utilizes its capital. In traditional finance, this term is often used interchangeably with Return on Capital Employed (ROCE), which estimates the profit generated by a company per $1 of capital employed. In the world of DeFi, however, there is no standard way of calculating capital efficiency; it varies from protocol to protocol. For example, many measure capital efficiency in a DEX via its utilization ratio, defined as the ratio of a DEX’s 24H trading volume to its TVL. Yet, the same metric cannot be extended to a lending/borrowing protocol. Even so, one thing that remains common across all protocols is that higher capital efficiency is indicative of a protocol that is putting its capital to good use.

For a bridge, not unlike a DEX, capital efficiency can be gauged using two key metrics –

- Utilization Ratio = Daily Trading Volume / TVL

- System Return on Investment (ROI) = Total Revenue Generated / Total Amount Spent in Sourcing the TVL

Since the advent of Uniswap v3, capital efficiency in DEXes has become a hot topic; however, the importance of capital efficiency in bridges has often been understated. Let us use an analogy to illustrate the significance of capital efficiency for cross-chain bridges. Consider a real-world bridge connecting two cities. There are cabs stationed at both ends of the bridge to transport users from one end to the other. As the number of cabs increases, more passengers can go from one end to the other simultaneously. However, if the maximum number of people who want to travel at any given time is less than 10, having 100 cabs sitting idle is pointless. Now imagine that these cabs also need to be paid some sort of “holding fee” even if they’re not being used; this will undoubtedly exacerbate the problem.

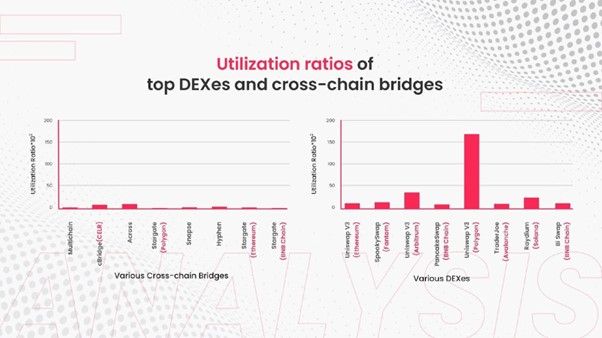

Regardless of this knowledge, most leading cross-chain bridges with high TVL narrate a similar story. Ideally, due to the nature of the application, the focus on augmenting the capital efficiency of a bridge should be much more pertinent than that of a DEX. But surprisingly, while conducting an in-depth analysis, we found that the utilization ratio of top cross-chain bridges was much less than that of DEXes, a clear indicator of their inability to utilize their capital efficiently.

Unsustainable Yield Mining Campaigns

As noted previously, most bridges, even now, are engaged in an imaginary race to aggregate as much liquidity as possible. To do that, they are forced to employ unsustainable liquidity mining campaigns – the brunt of which ultimately falls on the protocol itself.

a. Token emissions lead to diminished token prices, thereby reducing the yield on offer, which causes the yield farmers to inevitably withdraw capital from the protocol to pursue higher-yielding opportunities.

b. The revenue metrics of most asset-transfer bridges do not justify the costs incurred by them for running liquidity mining schemes. In the previous section, we briefly touched upon the topic of System ROI – the amount of revenue generated by a protocol per $1 spent to source liquidity, which is a rather good indicator of a protocol’s growth. Incessant liquidity mining campaigns with excessive emissions and very little revenue can be an indication of a protocol’s poor health.

To address these issues, we believe that asset-transfer bridges can spend a fraction of the cost incurred on liquidity mining campaigns to incentivize crowdsourced rebalancing instead. By imposing a negative fee, bridges can encourage users to initiate transfers from chains where liquidity is low to chains where liquidity is high.

For example, suppose at any given instance, the liquidity on Polygon is much higher than required while the liquidity on Fantom is below the threshold. In such a case, bridges can reward users for moving funds from Fantom to Polygon (which will lead to the locking of more funds on Fantom and the release of excess funds on Polygon). To ensure that no one takes undue advantage of this system, the rebalancing reward has to be decided carefully – it shouldn’t be too low so that no one is interested in rebalancing the bridge. Still, it also shouldn’t be too high so as to entice users to create a liquidity imbalance themselves.

The Honey Pot Problem

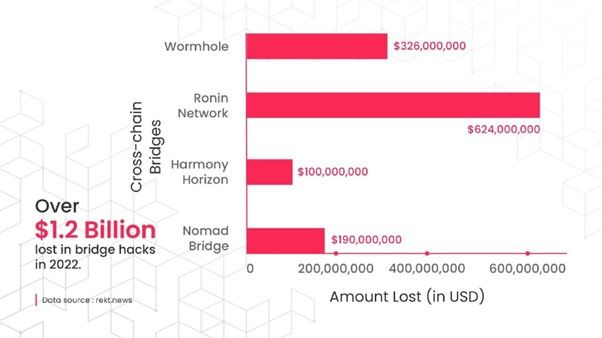

Cross-chain bridges have unwittingly proved to be the world’s most extensive bug bounty program of 2022, accounting for more than 70% of the hacks by volume in the DeFi/crypto space. The bridge TVL acts as a honey pot for the black hat hackers scouting for high-value vulnerabilities. The anonymous nature of the ecosystem makes it even more lucrative for hackers, unlike the banking system, where accounts are always subject to KYC.

The fact remains that, even now, most bridges are not mature enough to accommodate extremely large TVL; not only do they risk being compromised themselves, but they also run the risk of having their entire liquidity base compromised if there’s a potential security issue in the codebase of any of the other bridges to the same blockchains. We saw this case earlier this year when a hacker was able to drain around $100m of liquidity stored in Harmony’s Horizon bridge.

As a consequence, USDC on Harmony lost all its backing, which led to its de-pegging from the $1 mark. Like most exploits, the loss was eventually borne by the liquidity providers and not by the protocol itself; liquidity providers lost the redeemability of their 1USDC on Harmony.

Our thesis is that bridges need to have just-enough or sufficient liquidity, as irrationally large liquidities serve no good to the community or the project except perhaps appeal to those who want to build a convenient narrative around TVL. As we all know, bridges are complex pieces of technology. By focusing on increasing efficiency rather than increasing liquidity, protocols can ensure the same volume while limiting the amount of liquidity exposed to potential vulnerabilities. After all, the bridges will be valued on how much traffic flows through them, not just how wide they are.

Bridge Liquidity Paradox: Concluding Remarks

Throughput is a more relevant measure of bridge efficiency. Volume transacted as opposed to volume locked up; The efficiency of a bridge in the real world is measured in traffic flowing across the bridge. Current approaches to bridges, by putting too much emphasis on TVL, distract from the true purpose that they were originally designed for, which is to get tokens across chains in a fast and secure manner.

Bridge Liquidity Paradox: About the authors

Ramani Ramachandran is CEO & Co-Founder of Router Protocol and Dfyn Network. An MIT alum, Ramachandran has been a serial entrepreneur in the fintech and digital assets space for the better part of a decade. He built and ran Asia’s earliest crypto fund returning 4x; built Fordex, the world’s first stable coin DEX; and Qume, an institutional-grade crypto exchange. He also launched Asia’s first crypto-index token.

Vatsal Gupta is a DeFi/Research Analyst at Router Protocol and Dfyn Network. Prior to working in the DeFi domain, Vatsal has worked extensively as an undergraduate researcher in the field of blockchain applications, IoT and federated learning. He has co-authored 6 publications in peer-reviewed conferences and journals such as IEEE T-ITS, IEEE IoT Journal, and ACM MobiHoc.

Got something to say about bridge liquidity or anything else? Write to us or join the discussion in our Telegram channel. You can also catch us on Tik Tok, Facebook, or Twitter.

Opinions seen on this website should not drive any financial decisions from readers.

Disclaimer

In compliance with the Trust Project guidelines, this opinion article presents the author’s perspective and may not necessarily reflect the views of BeInCrypto. BeInCrypto remains committed to transparent reporting and upholding the highest standards of journalism. Readers are advised to verify information independently and consult with a professional before making decisions based on this content. Please note that our Terms and Conditions, Privacy Policy, and Disclaimers have been updated.