American banks are well positioned for a severe catastrophe at the time of writing. A mix of interest rate hikes, unrealized losses, and uninsured depositors contribute to the chaotic situation. So, can crypto like Bitcoin help?

The demise of Silicon Valley Bank (SVB) initiated a crisis of trust in the U.S. banking sector. Americans, especially uninsured depositors, are scrambling to determine if their deposits are at risk. Per a recent study, 186 banks representing five percent of all U.S.-based banks, face a high risk of succumbing to a similar fate.

What are some of the key risks involved as the crisis unfolds, and what will the effects be across the globe?

Fragile Banking Situation

A few economists published a study titled ‘Monetary Tightening and U.S Bank Fragility in 2023: Mark to Market Losses and Uninsured Depositor Runs.’ Some of the key highlights were shared with BeInCrypto.

U.S. banks are at risk of going under, given the assets banks hold on their balance sheets, namely U.S. bonds. They are also known as U.S. government debt and mortgage-backed securities (MBS) bundles of mortgages. According to regulators, these bonds and MBS are the safest assets a bank can hold. Banks invest most of their customer deposits in U.S. bonds and MBS. These assets earn interest for the banks and thus make it possible for institutions to offer services with low or no fees.

However, when interest rates rise, the value of U.S. bonds and MBS goes down. Notably, higher interest rates result in the U.S. bonds and MBS crashing. Banks can become temporarily insolvent if these assets’ value falls too much. This insolvency is temporary because when U.S bonds and MBS mature, the bank receives the total value of the underlying asset at the end of loan terms.

This temporary insolvency is why banks don’t report the losses on U.S. bonds and MBS when interest rates rise. This is simply because it’s a loss once they sell, and in the case of U.S. bonds and MBS, banks will only lose something if they hold them to maturity.

Why Did Silicon Valley Bank Fall?

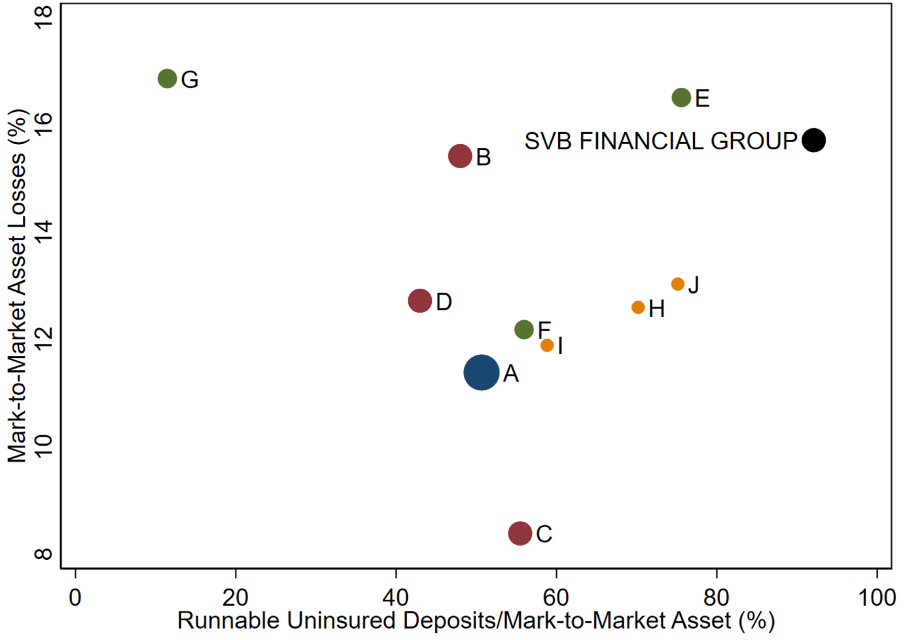

However, these so-called unrealized losses are acceptable as long as the bank isn’t forced to sell any assets at a loss on customer withdrawals. Unfortunately, the fall of SVB proved otherwise. 92.50% of SVB’s deposits were uninsured by the Federal Deposit Insurance Corporation or FDIC. For context, the FDIC only ensures bank deposits up to $250,000 per account; any amount above that is considered uninsured. The bankrupt bank experienced a bank run because its uninsured depositors could see that it had many unrealized losses. This led to speculation that SVB didn’t have enough money to honor all withdrawals.

Around $9 trillion of bank deposits in the United States are uninsured, which equates to roughly 50% of all bank deposits. Banks have been happily investing uninsured deposits into U.S. bonds and MBSs. The problem is that interest rates have risen, and their unrealized losses have been piling up. In fact, at the end of 2022, U.S. banks collectively had unrealized losses totaling more than $600 billion. Interest rates have risen more since then, so these losses are likely even more extensive.

In the study, the economists examined around four thousand banks to see which ones were most at risk and why. They found that 42% of all bank deposits have been invested into regular MBSs, with another 24% invested into commercial MBSs, such as commercial real estate loans, U.S bonds, and other asset-backed securities (ABS).

Zooming in on unrealized losses on these assets after crunching the numbers, the researchers stated:

“The median value of banks’ unrealized losses is around 9% after marking to market. The 5% of banks with the worst unrealized losses experience asset declines of about 20%. We note that these losses amount to a stunning 96% of the pre-tightening aggregate bank capitalization.”

What’s At Stake Here?

Global systemically important banks or GSIBs like JP Morgan and Bank of America have less than five percent of unrealized losses. The average non-GSIBs have 10% unrealized losses, and SVB wasn’t even the worst. Surprisingly, more than 11% of U.S banks have more considerable unrealized losses than SVB did when it went down.

While SVB’s collapse came as a reminder of the fragility of the traditional financial system, many banks are at risk from uninsured deposit withdrawals, it read:

“Even if only half of uninsured depositors decide to withdraw, almost 190 banks are at a potential risk of impairment to insured depositors, with potentially $300 billion of insured deposits at risk.”

The researchers concluded that assets held by U.S banks are more than two trillion dollars lower than reported, thanks to unrealized losses-based accounting.

Further, it reiterated that hundreds of banks are at risk of going under if uninsured depositors withdraw. To worsen the situation, the latest hike in interest rates raised uncertainty.

Rising Interest Rates Raise Red Flags

Rising interest rates can indeed impact banks’ asset market value and threaten their stability. When interest rates rise, the value of existing fixed-rate assets held by banks, such as mortgages, bonds, and other loans, can decline as these assets become less attractive to investors who can get higher returns elsewhere. Additionally, as interest rates rise, borrowing costs for banks increase, which can reduce their profitability and make it harder for them to generate sufficient returns to meet their obligations.

If the decline in asset values is significant enough, it can erode a bank’s capital, making it more vulnerable to potential losses or a sudden increase in withdrawals by depositors. In the worst-case scenario, this can lead to a run on the bank, which could further destabilize the banking system.

The situation can be exacerbated if a bank has a large share of uninsured deposits. When depositors’ funds are not insured by the Federal Deposit Insurance Corporation (FDIC), they are not protected in case of a bank failure. This can create a situation where depositors rush to withdraw their funds at the first sign of trouble, which can further undermine the bank’s stability and potentially trigger a broader crisis in the financial system.

Is the Grass Greener on the Crypto Side?

Andrew Lokenauth, a writer with over 15 years of experience in finance, spoke to BeInCrypto on the matter. Taking a different perspective, he opined:

“It’s equally important to remember the cyclical nature of interest rate fluctuations (for a balanced perspective). Losses may be reversed if interest rates start to fall, so banks may no longer experience these losses on their bond holdings. It’s important to note that these losses are only on paper, and banks will not lose any money until they sell their bond holdings.”

Also, the federal government stepped in to protect the depositors of SVB and Signature Bank.

Nevertheless, the banking system’s chaos harms its credibility. On the other hand, cryptocurrencies come in handy, given the brewing situation. The primary issue with cryptocurrencies is their price volatility. But the largest and most established cryptocurrencies, like Bitcoin, have been battle tested for over a decade. Aside from that, cryptocurrencies are one of the best hedges against the banking system.

But again, the rapid CBDC development could risk the decentralization aspect, giving the government control over the usage.