The allure of anonymity has always been a significant draw in the blockchain ecosystem. Early adopters touted the ability to conduct transactions in secrecy, far from the prying eyes of centralized institutions and regulators.

However, as blockchain evolves, the industry faces a critical question – Is anonymity still paramount, or is it a fading aspect amidst growing demands for transparency?

Why Blockchain Transparency is Important?

The blockchain sector is undergoing a transformation. Enhanced regulatory scrutiny and advancements in blockchain analytics are slowly demystifying the once-opaque crypto ecosystem.

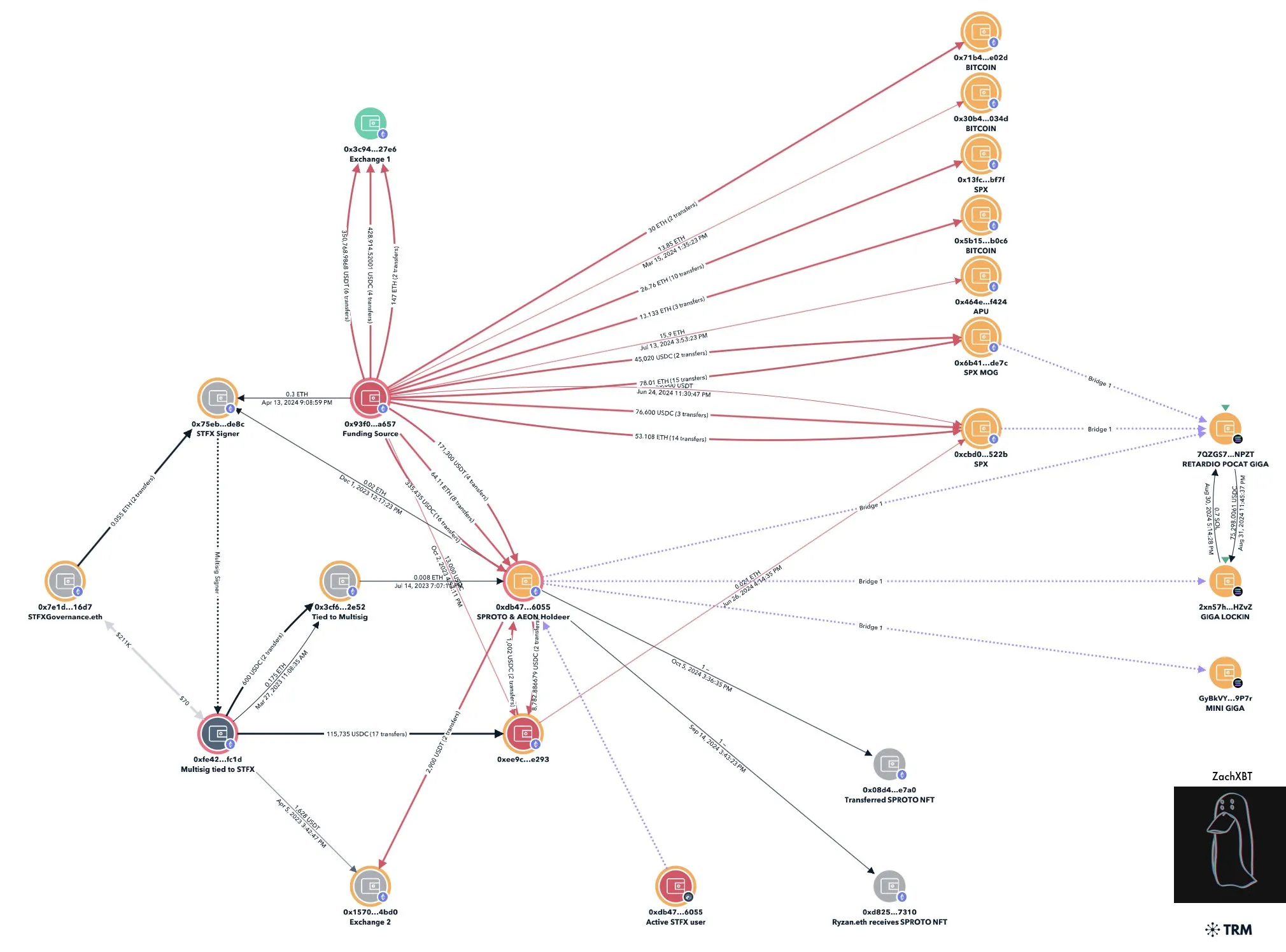

A revelation by the on-chain detective ZachXBT, who exposed the crypto holdings of a meme coin trader, Murad, highlights this shift. This exposure ignited debates about the ethics of revealing such information and whether such acts undermine the foundational privacy promised by blockchain.

Read more: Who Is ZachXBT, the Crypto Sleuth Exposing Scams?

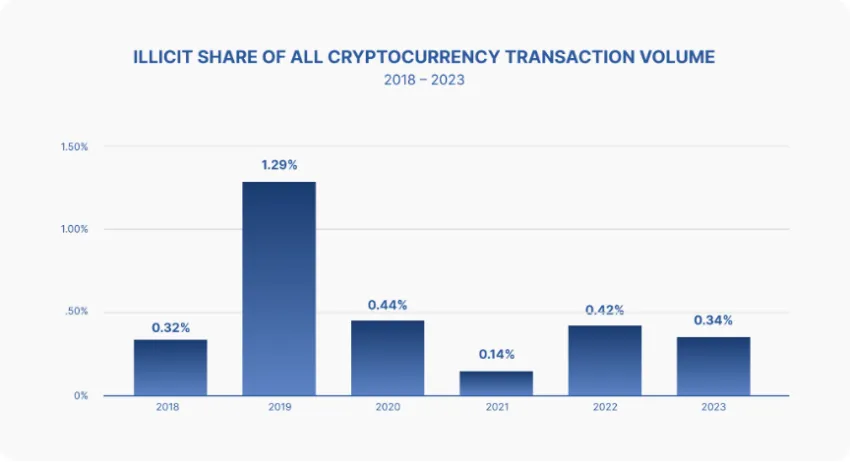

Despite concerns, many argue that transparency is crucial for combating fraud, money laundering, and other illicit activities within the crypto space.

The call for greater oversight is partly driven by the increasing incidents of crypto-related frauds and hacks. According to an Immunefi report, over $412 million was lost to such incidents in the third quarter of 2024 alone. Moreover, year-to-date, the total reached $1.3 billion across 169 incidents by September 2024.

These security breaches and the utilization of cryptocurrency in illegal activities fuel the debate over blockchain’s dual nature—offering freedom yet potentially facilitating unlawful acts.

Need For a Balanced Approach

In an interview with BeInCrypto, Alex Pruden, Executive Director at Aleo Foundation, countered this perspective. He highlighted the misuse of traditional financial systems in crimes.

“The traditional financial system is used for illegal activities all the time. 99% of money laundering and sanctions evasion actually happens through large financial institutions (who don’t catch it until after the crime has been perpetrated). Does that mean we should ban banks and payment processors? Of course not, because these institutions provide benefits to everyone else. The key is finding the right balance,” Pruden told BeInCrypto.

Supporting this, a Crypto Information Sharing and Analysis Center (ISAC) report notes that cash is used far more frequently than crypto in illegal activities. The report challenged the notion that crypto is predominantly the currency of criminals.

Read more: Anonymity vs. Pseudonymity: Understanding the Key Differences

Moreover, purists and privacy advocates contend that an extreme move towards openness erodes the core values of blockchain. Pruden emphasized the importance of privacy.

“Real-world financial transactions between parties are often predicated on a notion of confidentiality. And this confidentiality/privacy is essential for businesses to function. For example, businesses transacting with one another may not want the contents of that transaction public to competitors. Likewise, individual financial transactions on public blockchains are at risk from surveillance, data mining, and cyberattacks,” Pruden stated.

Contrary to Pruden’s view, Adrian Brink, co-founder of Namada, argues that blockchain was never truly about privacy.

“I don’t think that blockchain was built on the promise of privacy at all. Bitcoin doesn’t offer any privacy guarantees. The potential for de-anonymization was there from the beginning,” Brink told BeInCrypto.

Read more: Top 7 Privacy Coins in 2024

Experts Claim Zero Knowledge Proof is the Solution

This tension between privacy and transparency raises pivotal questions about the future of blockchain. Can it remain decentralized and secure while compromising on anonymity? Or is privacy still essential to protect users and uphold the technology’s principles?

William Wendt, Head of Ecosystem at Oasis, told BeInCrypto that privacy isn’t a binary choice.

“Often, this issue of privacy vs. transparency is looked at through a binary lens. Either a blockchain is fully transparent or fully anonymous. However, this is not the case. Privacy is a spectrum, and different dApps and users will have different preferences for what level of privacy/transparency they will need,” Wendt said.

According to experts, a promising solution lies in zero-knowledge technology, which offers a way for transparency and privacy to coexist. Zero-knowledge proofs (ZKPs) allow for the verification of transactions without revealing underlying data, thus maintaining user privacy while ensuring compliance with laws.

“Historically, transparency was seen as a mechanism to enforce compliance, but it doesn’t have to come at the cost of user privacy. Cryptographic solutions like ZK proofs (ZKP) enable a system where transactions can be “correct by construction” in terms of the law, without revealing the underlying data. This protects user privacy and creates a user interface closer to a bank account/payment app than most Web3 applications today,” Pruden noted.

Brink also supports this nuanced approach, emphasizing that the need for privacy varies by context.

“What you need to share with your local government is going to be different from what you want to share with the world. The key issue is primarily self-sovereignty. We’re moving towards a world where technologies like zero-knowledge cryptography empower users with the choice of what to share. Privacy can coexist with transparency, but the architecture must be thoughtfully designed,” Brink told BeInCrypto.

Read more: What are Zero-Knowledge Proofs? Securing Growth for Web3 Apps

Zero-knowledge cryptography addresses privacy concerns and also meets regulatory requirements, offering a balanced solution that protects individual privacy and fulfills transparency obligations. This technology proves compliance with anti-money laundering (AML) and Know Your Customer (KYC) regulations without disclosing personal information, providing a win-win scenario for all stakeholders.

Due to heightened interest, the zero-knowledge sector is growing. According to data from CoinGecko, the total market capitalization of zero-knowledge coins stands at nearly $13.5 billion.

In conclusion, while blockchain was initially celebrated for its privacy features, the changing environment suggests that both transparency and privacy are necessary for its future. The ongoing development of zero-knowledge cryptography and similar technologies may hold the key to maintaining blockchain’s founding principles while adapting to new regulatory environments.

Disclaimer

Following the Trust Project guidelines, this feature article presents opinions and perspectives from industry experts or individuals. BeInCrypto is dedicated to transparent reporting, but the views expressed in this article do not necessarily reflect those of BeInCrypto or its staff. Readers should verify information independently and consult with a professional before making decisions based on this content. Please note that our Terms and Conditions, Privacy Policy, and Disclaimers have been updated.