Ella Hough, a Cornell University senior and Bitcoin advocate, published an interactive calculator modeling Strategy’s STRC preferred stock as a retirement alternative to Social Security.

Among Ivy League and top-tier schools, Cornell stands out as one of the largest in terms of scale and student body size while maintaining elite academic prestige. This is why Ella Hough’s role there (founding the Bitcoin Club and pioneering a custom degree) carries weight in the Bitcoin community.

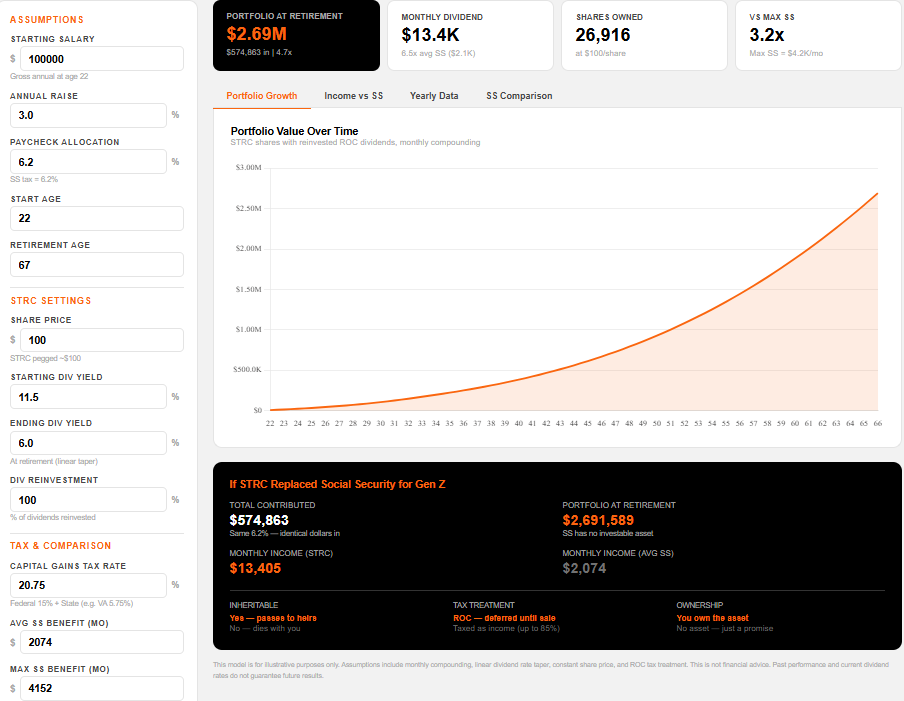

What If Gen Z Could Swap Social Security for MicroStrategy’s STRC?

Hough’s model assumes a 22-year-old earning $100,000 annually redirects their 6.2% employee payroll tax into Strategy’s (MSTR) Variable Rate Series A Perpetual Stretch Preferred Stock (STRC).

The instrument currently pays an 11.5% annualized dividend and trades near its $100 par value on Nasdaq.

With dividends reinvested monthly and a yield that tapers linearly to 6% by retirement age, the calculator projects a portfolio worth approximately $2.69 million by age 67. That translates to $13,405 in monthly dividend income.

By comparison, the average Social Security benefit sits at $2,074 per month. The 2025 SSA Trustees Report projects that the combined trust funds will be depleted by 2034, after which only 81% of scheduled benefits would remain payable.

Digital Social Security — What could happen if Gen Z had the choice to allocate their 6.2% payroll tax to STRC instead?. Source: Ella Hough / 21mmforthe21st.github.io

Risks and Reactions

However, multiple assumptions carry significant risk. STRC dividends are not guaranteed and can be adjusted monthly by MicroStrategy’s board.

The preferred shares are also not directly collateralized by Strategy’s 762,099 Bitcoin treasury.

“Weekend thought experiment: What if Social Security for Gen Z could look a little more like $STRC?” Ella Hough posed.

Critics in the replies flagged inflation-eroded returns over 45 years, dividend-cut scenarios, and the fact that redirecting FICA taxes would require an act of Congress.

Others argued that direct Bitcoin or MSTR common stock exposure would outperform a yield-focused instrument.

Still, the model highlights a growing generational disconnect. Many Gen Z workers already expect reduced or zero federal retirement benefits.

Hough’s tool gives that anxiety a concrete, numbers-driven framework, even if the political path to payroll-tax opt-outs remains distant.