Over the past decade or so, we have seen money consistently moving from bank counters to mobile and app-based banking. An emerging class of neo banks, such as Revolut and N26, brought this evolution into the mainstream.

These services proved that people preferred simple apps, quick transfers, and multi-currency cards over anything tied to the archaic setup of a physical enterprise. And for a while, that felt like the end of the story.

Fast forward to the mid-2020s, and crypto has once again reopened the discussion. It is pushing people to think not just about convenience but about who controls their funds and what happens in crisis situations, such as during a freeze or infrastructure failure.

That is the gap web3 neo banks now address. They keep the ease of modern fintech but place self-custody, stablecoins, and global access at the center of the experience.

But what exactly is an ideal web3 neo bank today? That is what we explore in this comprehensive guide to the ongoing evolution of neo banks.

What exactly is a web3 neo bank?

Once you accept that money can live on a blockchain instead of a centralized bank ledger, a natural question comes up: what would a “bank” look like in that decentralized setup?

A web3 neo bank answers that question with a simple idea. It gives you tools that feel close to a modern fintech app, but the core balance and transactions sit on-chain under your own control.

In practice, a web3 neo bank usually starts with a self-custodial wallet. You hold the keys, you approve every move, and no support team can freeze or reroute funds behind the scenes. On top of that base, the app adds features you normally expect from a mobile bank: stablecoin balances for day-to-day value, card support in some cases, recurring payments, and quick transfers between contacts.

The difference lies in the rails under the interface. For instance, transfers settle on public networks instead of private bank systems. Similarly, stablecoins stand in for account balances in USD, EUR, or other currencies. DeFi hooks, meanwhile, allow swaps, yield options, and cross-chain transfers without a separate exchange account.

Some projects then connect those on-chain funds to fiat accounts or cards so you can pay bills, receive salaries, or spend in shops.

So, basically, if you zoom out, a web3 neo bank tries to answer three questions at once: how do you keep self-custody, how do you pay and save across borders, and how do you tap DeFi without a maze of extra apps? And that “mix” has now started to matter more as crypto and traditional finance move closer together.

Why web3 Neo banks matter now

Once you accept the idea of a self-custodial “bank app,” the next question is simple: why now?

Part of the answer sits in trust. After recurring instances of exchange failures, withdrawal pauses at the worst possible moments, and stablecoin scares, more people want control over keys and exit routes, not only a slick interface and cashback.

The other part comes from how money now moves. Stablecoins allow near-instant transfers across borders. Similarly, layer-2 networks can cut fees to a level that makes small payments practical.

At the same time, many traditional providers still rely on slow settlement, limited service hours, and strict local rules that block users in the wrong postcode.

That mismatch between new rails and old systems is now increasingly showing up in daily life for many users as the world becomes ever more connected.

For instance, a freelancer in one country might invoice in USDT, pay rent in local currency, and hold part of their reserves in Bitcoin or Ether. A saver in a high-inflation economy might prefer a dollar stablecoin over a weakening local unit. Similarly, a trader might want yield, swaps, and card use in one place without another custodial account.

Web3 neo banks attempt to tie all of those pieces together. They aim to give you one app where stablecoin balances, card rails, cross-chain swaps, and simple yield options sit on top of self-custody. And that shift sets the stage for a more obvious question: with so many teams chasing the same idea, how do their models differ in practice?

How web3 neo banks differ from fintech apps

At first glance, a web3 neo bank and a modern fintech app can look similar. You see balances, a card, a list of transfers, and maybe a section for savings or yield. The difference shows up once you ask two questions:

- Who exactly holds the assets?

- Which rails move the value?

Here are the differences in a nutshell:

| Aspect | Typical fintech app | web3 neo bank |

| Where funds sit | A regulated entity holds client funds on its own balance sheet or in pooled accounts. | The core balance sits on-chain under keys you control. |

| Who you trust | You trust the entity, its partners, and its local regulator to keep funds safe and available. | You rely on the security of your wallet, public blockchain infrastructure, and the protocols that hold your assets. |

| Ledger and transparency | The app provides a smooth front end, but the core ledger sits in a closed system that you never see. | Stablecoins, native coins, and DeFi positions all live in a wallet, not on a company balance sheet, and remain visible on-chain. |

| Role of regulation and rails | The provider operates under regulation and manages everything inside its own system and banking relationships. | The provider still complies with rules when it touches fiat or card networks, but digital assets sit in contracts or addresses on public chains. |

This significantly changes the risk profile. Failure at the company level no longer equals an automatic freeze of your coins, though you still face protocol, stablecoin, and smart contract risk. It also changes expectations around features.

Many users now want the same clarity and comfort they see in fintech apps, but with clear proof of custody, on-chain transfers, and direct access to DeFi rails.

Once you view the sector through that lens, the next useful step is to group the main models in play instead of treating all web3 neo banks as identical.

Where web3 neo banks stand today

As of late 2025, most web3 neo banks out there focus on narrow functions rather than a full banking stack. The space now includes several types of apps that solve specific needs but rarely cover everything a modern user expects:

- Card-oriented self-custodial apps provide a wallet with debit-card support and simple fiat rails, but limited multi-chain or DeFi depth.

- Stake-backed spending models let users spend against staked assets. Useful for yield plus liquidity, but not a full multi-currency banking setup.

- Network-specific neo banks offer multi-asset accounts and yield features within one ecosystem. These are strong internally, but less effective across chains.

- Stablecoin-first payment apps focus on transfers, regional payment rails, or basic card use. Good for everyday payments, but not full banking.

To cut a long story short, the way this segmentation has shaped up tells you that most teams cover just one or two layers. It could be payments, yield, or card utility, but they do not yet offer a complete, self-custodial web3 banking stack.

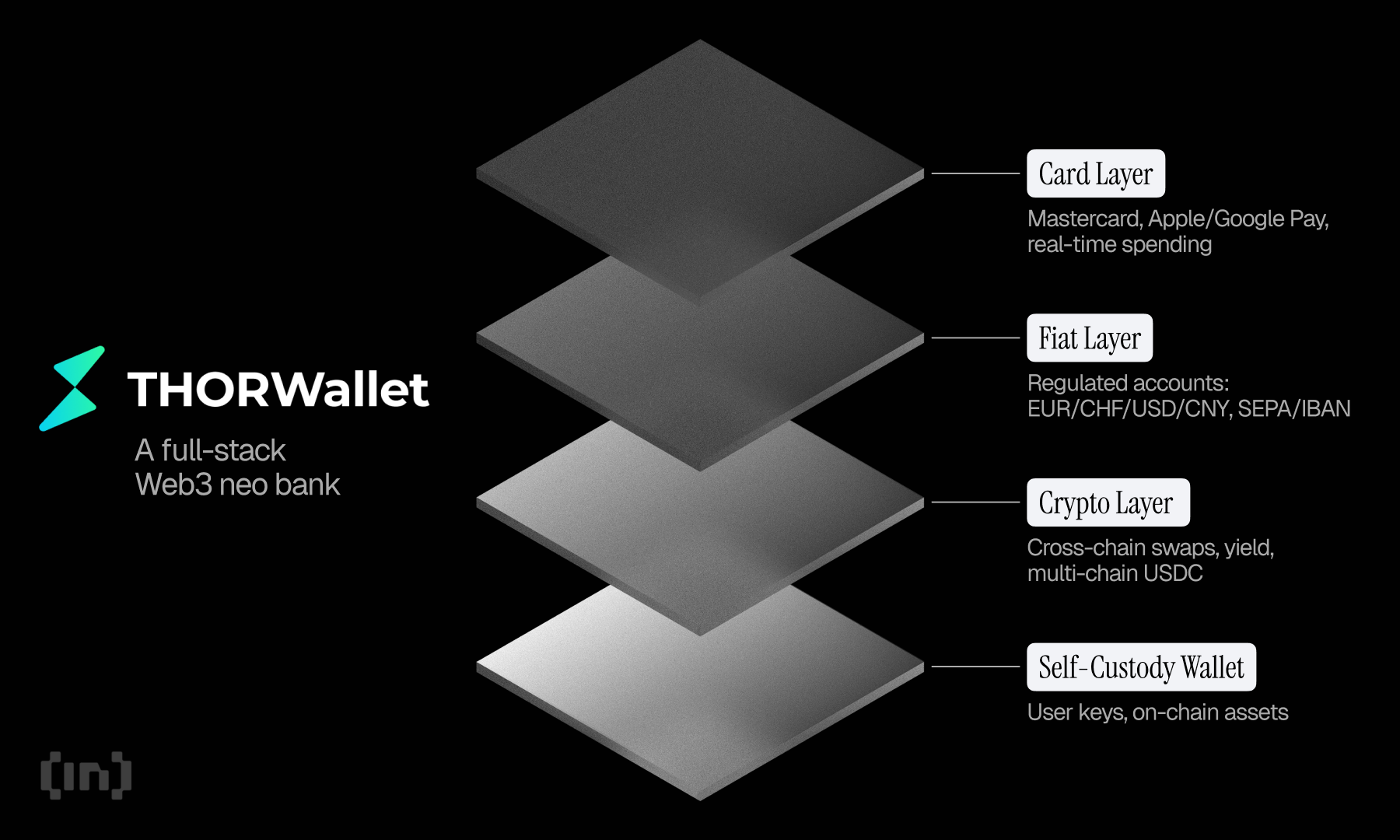

THORWallet as a full-stack example

Once you see that most web3 neo banks still cover only narrow use cases, it helps to study one project that aims to pioneer a model with more layers in a single system.

THORWallet fits that role as a case study.

We use ThorWallet as an example here to show how new, more practical solutions are emerging in the web3 neo banking space. In this quick review, we look at how THORWallet maintains a self-custodial core while tying it to regulated bank accounts, card rails, and on-chain tools.

What is THORWallet?

At the base, THORWallet operates as a non-custodial wallet. You hold the keys, you approve every move, and crypto balances sit on public networks rather than on a company balance sheet.

From there, the app connects to a Swiss-regulated multicurrency account with an individual IBAN. Users can keep fiat in several major currencies, such as CHF, USD, EUR, and CNY, which creates a combination that you rarely see elsewhere: a self-custodial base paired with an actual regulated IBAN account.

Card support

You also get comprehensive card support sits with these accounts. A debit card with a Mastercard label links directly to fiat balances and works with Apple Pay and Google Pay.

The card processes everyday payments in the local currency in a way that feels familiar to anyone who already uses mobile banking or fintech apps. That structure avoids the constant top-ups that many prepaid crypto cards require.

Fiat flows also extend beyond card use. Users can send and receive transfers through standard IBAN and SEPA rails and, in some regions, pay QR invoices from inside the app.

That keeps bill payment and account transfers close to what people already expect from e-banking, only in this case, the same app also controls self-custodial crypto.

Crypto support

On the digital asset side, THORWallet connects to cross-chain swap routes. Users can move between assets such as BTC, ETH, SOL, and others without wrappers, which removes the need for separate bridges or centralized exchange accounts for simple asset shifts.

Liquidity options sit in the same interface, so users can hold positions in pools and earn on assets without a separate DeFi dashboard, while control still rests with the wallet owner.

USDC also plays a practical role. The app supports USDC across several networks and allows movement between them without extra bridge fees on top. That reduces friction for users who rely on stablecoins as a base unit for transfers, savings, or on-chain trades.

P2P fiat transfers

Finally, THORWallet includes peer-to-peer fiat transfers inside its own user base. People can move CHF, EUR, USD, or CNY between accounts, which turns the app into a tool for remittances, expense splits, or simple transfers to contacts.

In sum, it shows how one project can attempt a more complete web3 neo bank model by combining self-custody, regulated multicurrency accounts, card use, fiat rails, and cross-chain DeFi access in one place, while still facing the usual trade-offs around regulation, stablecoin exposure, and protocol risk.

Taken together, these components show how a Web3 neo bank can extend far beyond swaps or card rails.

But what does this “full-stack” approach signal for the sector?

A setup that merges self-custody, traditional banking access, and cross-chain tools hints at where the category could move next. It shows that Web3 neo banks no longer need to pick a side between crypto and fiat. They can support both without compromising control or access.

The presence of regulated accounts alongside non-custodial assets also indicates how compliance and decentralization may coexist as the sector matures. And with features like P2P fiat and on-chain swaps living in the same interface, these apps start functioning less like wallets and more like operating systems for money.

So, in practical terms, this full-stack direction suggests that the next wave of web3 banking will focus on unifying tools. Not by adding more of them, but by reducing friction while keeping ownership intact.

What this transformation ultimately points to

All factors considered, the general direction of the market is now (relatively) easy to read.

Put simply, people want full control of their funds, the ability to move money across borders without friction, predictable costs, and products that work together instead of in isolation. They also want fiat-to-crypto flows that feel as natural as using a regular banking app.

As you have seen in this quick review, THORWallet, among other emerging solutions, sits inside this movement by attempting to deliver a full-stack model in one application: self-custody at the base, payments and accounts at the surface, and cross-chain tools running throughout.