As part of BeInCrypto’s decentralized finance (DeFi) deep dive series, we’ll take a look at one of the first and oldest DeFi protocols, MakerDAO. DAO stands for Decentralized Autonomous Organization, and Maker was one of the first, founded by Rune Christensen in 2014. It is currently the longest-running project on the Ethereum (ETH) blockchain.

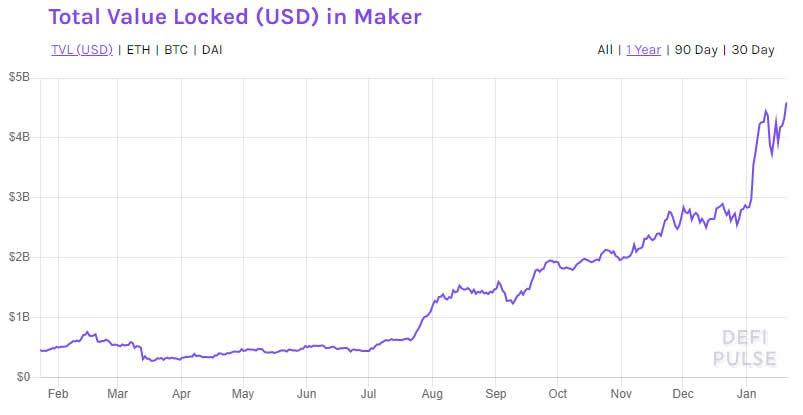

MakerDAO received a capital injection of $15 million from Andreessen Horowitz, in 2018, when he bought 6% of the total Maker (MKR) in circulation. Currently, Maker is the top DeFi protocol with a total value locked of around $4.5 billion and around 2.7 million in ether locked up.

In essence, it is a decentralized credit platform running on Ethereum that supports an ERC-20-based dollar pegged stablecoin called Dai. The primary difference with Dai and other stablecoins such as tether (USDT) or USDC is that it is decentralized. The protocol uses this stability to effectively make crypto loans possible without the volatility.

Christensen simplified Maker’s mission in late 2019 when he stated:

“The mission of the MakerDAO products and the Maker foundation is to create an unbiased currency for the world, which of course means for everyone all across the world.”

The DAI basics

Without going too deep into the technical nuances of the system, we’ll attempt to explain how MakerDAO actually works in as few words as possible.

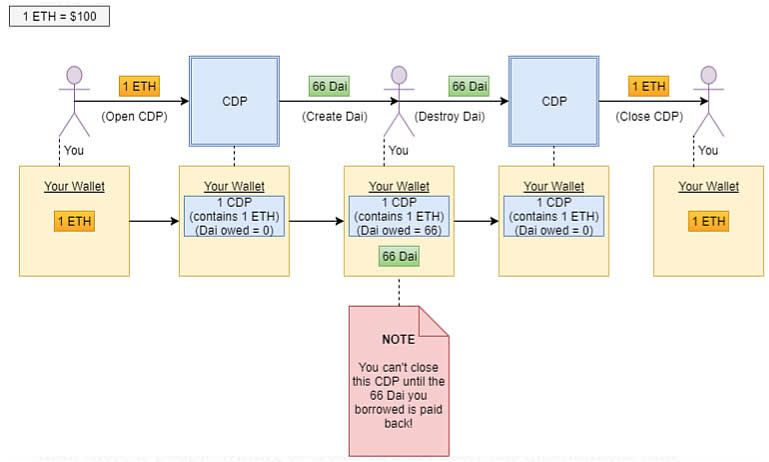

DeFi users can access Maker’s smart contracts to open a Vault and lock in collateral such as ETH in order to generate Dai as debt against that collateral.

This Dai stablecoin “loan” can then be used elsewhere such as other DeFi protocols or liquidity pools, and the ETH — or any other crypto collateral — can be reclaimed when the debt is repaid.

The process creates what is known as a collateralized debt position (CDP) which is simply the smart contract where the collateral (ether) in the Maker system is held. Users can borrow Dai up to 66% of their collateral’s value with a collateralization ratio of 150%, this is simplified in the diagram below.

If the value of the collateral (ETH in this case) goes below a certain threshold, users have to pay back the smart contract else it will auction off to the highest bidder.

This can result in a massive vault liquidation which is exactly what happened in March 2020 when crypto markets crashed (more on this below). Liquidation, and the threat of it, keeps the system stable by preventing people from borrowing too much though it does open opportunities to buy more ETH on leverage using borrowed Dai.

The Dai debt incurs something called a stability fee which is effectively a continuously accruing interest that is paid upon repayment of borrowed Dai. It is a way of maintaining the dollar peg as when CDP owners mint more Dai than the market demands, the price of it falls below $1.

The stability fee increases through a governance vote to push up the cost of borrowing Dai and return the stablecoin to its peg by reducing demand.

Up until that fateful crypto crash in March 2020, there were also good earnings to be made just by holding Dai through the Dai Savings Rate (DSR). This is currently zero, however, and has never returned to those pre-crash levels despite the recovery of crypto markets.

The easiest way to interact with Maker is through its Oasis Portal which enables users to open and manage Vaults, review Vault history, deposit Dai into the Dai Savings Rate, and get the latest stats on the whole Maker system.

So where does MKR fit in?

MKR is the DAO governance token that is used for voting on protocol changes and upgrades, collateralization amounts, borrowing rates, and in extreme cases protecting the system from Black Swan events.

Should the collateral in the system be insufficient to cover the amount of Dai in existence, MKR is minted and sold onto the open market in order to raise the additional collateral and protect the system. Exposure to this potential scenario is one of the drawbacks of being a holder of MKR.

Effectively, this mechanism provides strong incentives for MKR holders to responsibly regulate the parameters at which the protocol can create Dai. Ultimately, it will be their funds on the line should the system fail, not the holders of Dai.

Multi-collateral Dai (MCD)

In November 2019, the previously single collateralized Dai (called Sai thereafter) was launched with options to provide collateral in a number of different crypto assets.

The MCD introduced new features to the Maker Protocol, including the much-anticipated Dai Savings Rate (DSR), additional collateral asset types, and a rebranding. Users were urged to migrate their Sai to Dai after the launch using the Oasis decentralized trading platform which Maker launched the previous month.

The first set of assets, in addition to ETH, to be voted upon for Dai (MCD) collateral were augur (REP), basic attention token (BAT), digixDAO (DGD), golem (GNT), OmiseGo (OMG), and 0x (ZRX).

Today, there are many different tokens that can be used to open a Maker vault and generate Dai including bitcoin (BTC) which needs to be tokenized or wrapped as an ERC-20 token (wBTC). Collateral can also be deposited in USDC, GUSD, and TUSD stablecoins, loopring (LRC), chainlink (LINK), compound (COMP), kyber (KNC), and yearn finance (YFI), among others.

A tumultuous year in 2020

Things were running swimmingly for MakerDAO at the beginning of 2020, but that all came crashing down in mid-March when crypto markets, and the world economy, slumped in the wake of the escalating covid-19 pandemic.

In an event the team dubbed “Black Thursday,” the mass liquidation of the vast majority of Maker vaults resulted in around $4 million in Dai being under-collateralized. This was caused by a crash in the price of ether which was used as collateral. In one week in March, ETH prices dumped 58% from around $250 to just over $100 and Dai lost is peg, increasing to $1.08.

No code was exploited, but many vault owners lost all of their collateral resulting in both a class-action lawsuit against the Maker Foundation, and an executive poll to compensate victims. The protocol dropped the Dai Savings Rate to zero to encourage holders to sell their Dai and drop the peg, and adjusted the stability fee to compensate.

MKR prices suffered for the entire year as their DeFi brethren surged around them. Following the massive dump in March, MKR prices hovered around $500 for most of the year, while the DeFi boom sent others such as yearn (YFI) and aave to the moon.

In October, a flash loan exploit threatened Maker’s governance system when a controlling party attempted to influence the outcome and pass a proposal after borrowing MKR tokens to vote with.

The good news for Maker is that it has reclaimed its top spot on the DeFi TVL charts as liquidity returned to the protocol towards the end of the year. However, there is still no way to earn interest by holding Dai aside from depositing it in third party DeFi liquidity pools.

MakerDAO into 2021

2021 has been much better for Maker and MKR prices literally took off a couple days after Jan. 1. Since the beginning of the year, MKR has surged 136% with a high of almost $1,600 hit on Friday, Jan. 15.

The surge has been attributed to an increased demand in stablecoins, particularly decentralized ones such as Dai. The amount of Dai currently in circulation is at record levels of $1.4 billion, according to Coingecko.

Since the beginning of 2020, the market capitalization of Dai has surged a whopping 3,200%. It is hard to believe there was just under $100,000 Dai in circulation this time last year.

According to DeFi Pulse, Maker is still the clear dominant force in DeFi, with $4.6 billion in total value locked and a market share of almost 19%. As expected, the TVL chart can be overlaid onto the Dai market cap one with uncanny similarity.

In terms of ETH, January saw a peak of 2.7 million locked, which is approximately 2.4% of the entire supply of the asset.

MakerDAO is one of the stalwarts of the crypto industry and it is in a prime position to dominate the fledgling DeFi ecosystem by offering a truly decentralized stablecoin and token-based governance system.

These attributes may be even more crucial if centralized stablecoins, such as the market dominant tether, come under the scrutiny of United States regulators this year and their potentially crypto crippling “Stable Act” proposal.