A recent survey of more than 5,700 Bitcoin (BTC) holders reveals a clear disconnect between belief and behavior in the crypto space. While nearly 80% of respondents support broader crypto adoption, 55% say they rarely or never use digital assets for everyday payments.

This growing gap between conviction and real-world usage suggests that the industry’s biggest challenge is no longer awareness or ideological support, but something else.

Most Crypto Users Support Adoption, Yet Rarely Spend: Here’s Why

The GoMining survey drew responses from users across multiple regions. The largest share came from Europe (45.7%) and North America (40.1%).

Participants also represented a broad range of experience levels, split almost evenly between those new to crypto and holders with several years in the market.

This distribution indicates that limitations around crypto spending are not confined to a single region or user profile. The survey found that crypto payments remain a niche behavior among users.

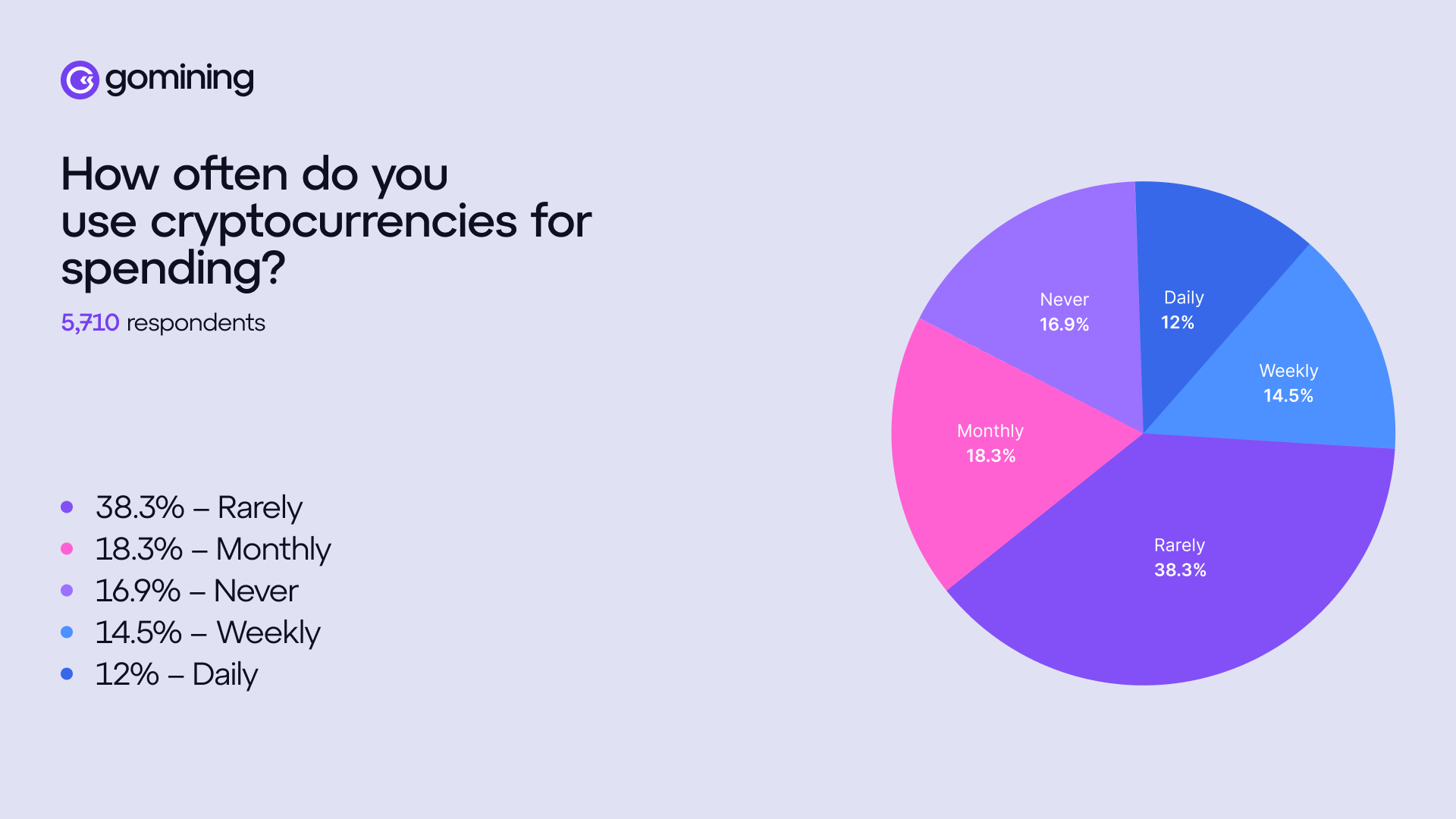

Only 12% of respondents used crypto for daily payments. That figure increases modestly to 14.5% on a weekly basis and 18.3% monthly. Still, the majority reported that they rarely or never spend crypto at all.

The spending behavior shows where crypto functions most effectively as a payment option. Digital goods account for the largest share at 47%, followed by gaming purchases at 37.7% and e-commerce transactions at 35.7%.

This indicates that users are already actively using crypto in digital-first environments that natively support payments. Beyond those spaces, payment usage declines significantly.

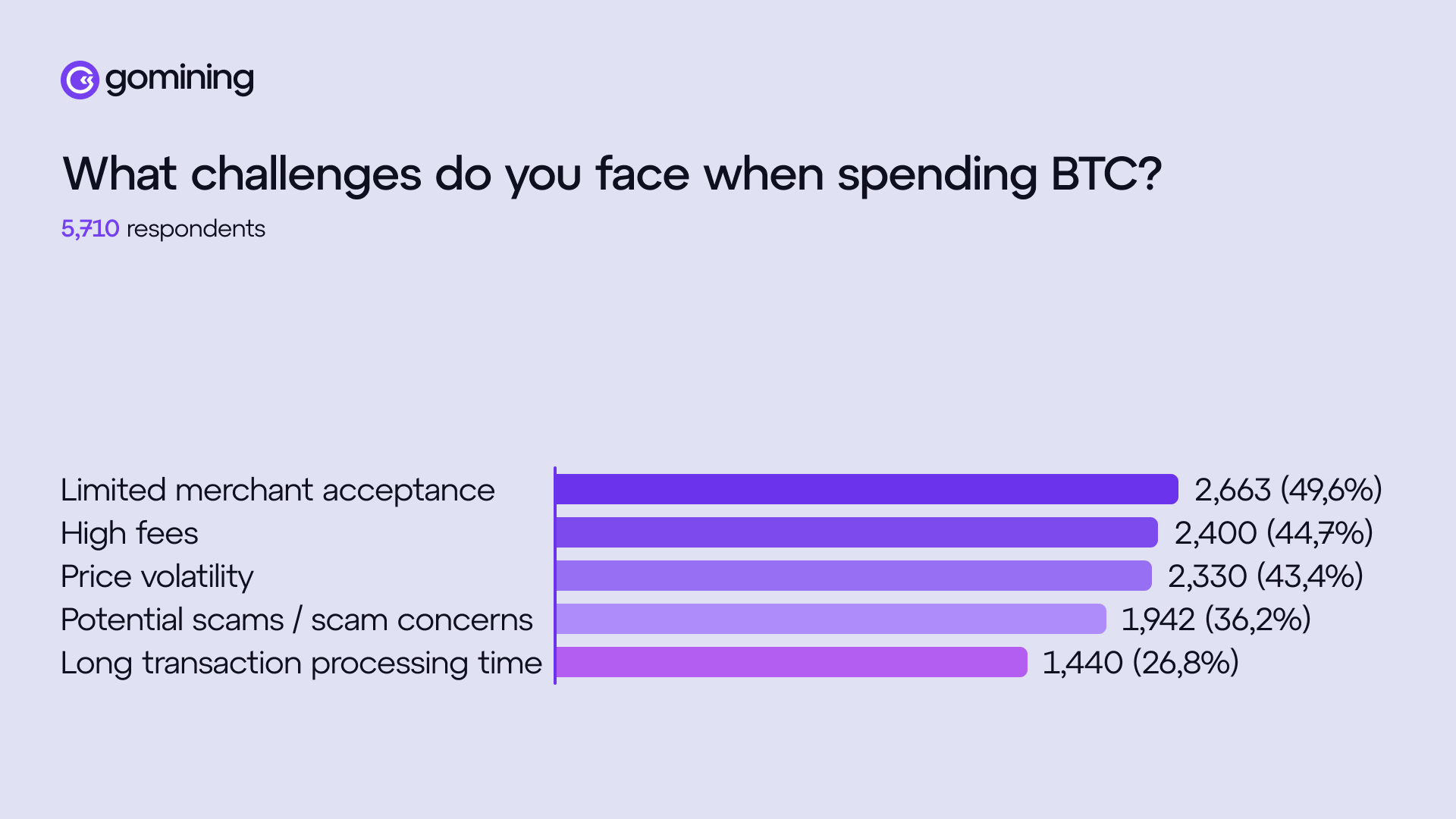

The findings revealed that infrastructure-related issues remain the primary barrier to spending. Respondents cited limited merchant acceptance (49.6%), high fees (44.7%), and volatility (43.4%) as the main reasons they do not use crypto for payments. Notably, 36.2% of the users also pointed to potential scams as a key reason.

Mark Zalan, CEO of GoMining, told BeInCrypto that if using crypto involves additional complexity, such as selecting networks, managing fees, accounting for price volatility, or figuring out how to reverse a mistake, most users will continue to see it as a novelty.

“For everyday users, “real utility” starts when crypto disappears into the background. When it’s accepted where they already shop, the cost is clearly competitive, settlement is fast, and consumer expectations like receipts or dispute handling are supported. To win that user, crypto payments should feel as boring and reliable as tapping a card,” he stated

Furthermore, the executive added that the gap looks less like an “adoption problem” and more like a “day-to-day product problem.”

“People can be open to crypto in principle while still defaulting to cards and bank apps, because those options are accepted everywhere and feel effortless. Our survey result is consistent with that: interest exists, but routine usage stalls when acceptance is patchy, costs feel unpredictable, and volatility creates hesitation,” he said.

Zalan noted that token abundance didn’t automatically create everyday utility because most tokens don’t remove a daily friction for regular consumers.

Practical utility emerges where crypto offers clear structural benefits, namely cross-border value transfers, faster settlement, and programmability. As a result, the industry is increasingly focusing on payment rails and integrations rather than expecting users to manage and navigate dozens of different assets actively.

Bitcoin Payments Face Incentive-Driven Expectations From Users

Meanwhile, the survey explored what actually drives users to choose crypto over traditional payment methods. Privacy and security emerged as the leading factors, cited by 46.4% of respondents. Rewards and discounts close behind at 45.4%.

Regarding Bitcoin payments, users were clear about what they wanted. 62.6% pointed to lower fees. Incentives such as rewards or cashback, followed at 55.2%, while wider merchant acceptance came in at 51.4%.

Notably, nearly half of the respondents said they expect to earn yield or rewards every time they pay. This highlights how incentive-driven expectations have become.

The data also points to a bigger shift in how users think about Bitcoin itself. While many still describe themselves as long-term holders, growing interest in mining, yield-generating products, and tokenized hashrate suggests a preference for Bitcoin that actively produces returns rather than sitting idle in a wallet.

Payments, in this context, are increasingly viewed as another opportunity to grow holdings. Zalan mentioned that incentives are a standard mechanism in payments.

He explained that traditional systems also use incentive structures. They offer rewards to consumers, economic benefits to issuers, and predictable settlement for merchants.

“Expecting crypto payments to scale without similar ‘make it worth switching’ dynamics is unrealistic. What incentives do reveal is where the remaining friction sits: if the experience were already cheaper, faster, and universally accepted, incentives would matter less. For now, incentives compensate for switching costs and help people build habits while the ecosystem closes the gap on acceptance, refunds/resource expectations, and ‘it just works’ checkout flows,” the CEO remarked.

Can Bitcoin Be Both a Payment Tool and a Store of Value?

Respondents also outlined what they would consider using Bitcoin for in the future. Everyday expenses ranked highest at 69.4%. This was followed by gaming and digital entertainment at 47.3%, and high-value or luxury items at 42.9%.

From the users’ perspective, Bitcoin is not limited to niche use cases but is increasingly seen as a viable option for daily spending. However, it also raises a critical concern: if Bitcoin succeeds as a daily payment method, does that reinforce its role as a store of value, or does it risk diluting that narrative?

Zalan believes a broader payment utility would ultimately strengthen Bitcoin’s role as a store of value. He explained that store-of-value status is ultimately a social and market coordination outcome.

It is shaped by liquidity, reliable settlement, and the extent to which an asset is integrated into real-world financial systems. According to him,

“The more often Bitcoin can be used (even via layers like Lightning or cards), the more it behaves like a durable monetary asset with resilient demand and infrastructure around it.”

He stressed that concerns about “dilution” often confuse spending with a loss of conviction. In mature financial systems, long-term holding and everyday use are not mutually exclusive, provided the infrastructure removes friction.

Looking ahead to 2026, Zalan outlined a more realistic outcome: Bitcoin serving as a reserve and settlement anchor, while user-friendly payment layers handle checkout, allowing users to transact without having to think about blocks, fees, or timing.