Earlier this year, the new marketplace Blur made waves in the NFT sector. Recent numbers suggest its lending platform could create a similar buzz. However, there are real and serious risks when borrowing against an NFT.

Blur’s lending platform, Blend, has quickly gained popularity since its launch just ten days ago. According to data from Dune dashboard, users have already borrowed a staggering 51,656 ETH—equivalent to $95 million—against their digital collectibles. Impressively, over 3,000 individual loans have been opened on the platform thus far.

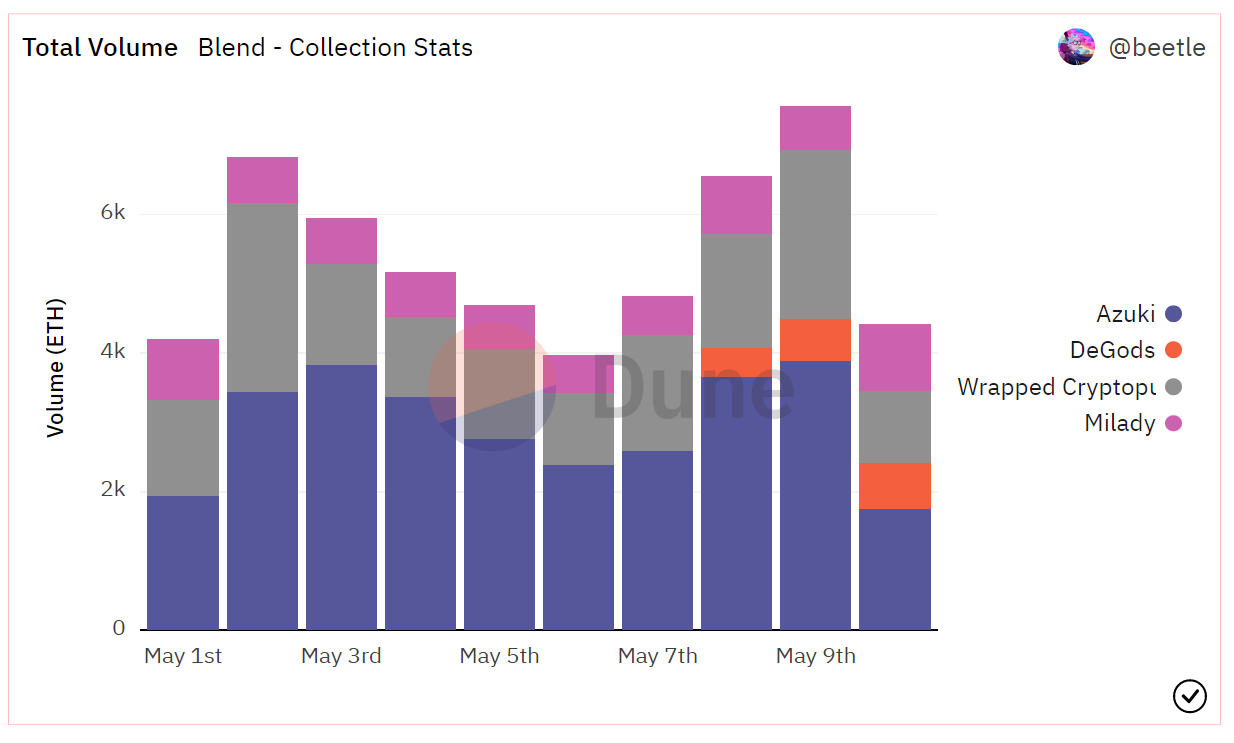

Blend Supports Four Collections

Blend currently supports loans backed by four NFT collections: Miladys, Azukis, DeGods, and wrapped versions of CryptoPunks.

Blur generated a buzz earlier in the year with its impact on the NFT market. Soon after launch, it surpassed OpenSea, the king of NFT marketplaces, with 53% market share. Blur’s native token airdrop in Q1 2023 drove significant traction to the NFT marketplace and aggregator, resulting in a surge in Ethereum‘s NFT trading volumes.

Blend, also known as Blur Lending, looks like it might do even better. Since its launch, Blur’s lending platform has swiftly surpassed competitors like NFTfi, Arcade, and BendDAO, driving the NFT loan volume to an impressive $67 million in just one week.

Blend’s loans alone make up a remarkable 75% of the total volume. Currently, the total number of accepted and refinanced loans is 3,045, with 922 unique lenders, according to Dune.

Blend is the latest player to join the market. But using NFTs as collateral has been popular since 2021 thanks to the emergence of new platforms and the rising cost of digital assets. In more recent months, prices have been more muted. In any event, using NFTs as collateral presents severe risks to lenders.

Liquidity Risk

Using an NFT for collateral is not unlike using other assets to fund loans. Borrowers deposit their NFT as collateral, set loan terms, and receive ETH from the lender, while the NFT remains as collateral. The borrower then repays the loan to retrieve the NFT. A failure to repay results in liquidation and the lender claiming ownership of the NFT.

However, NFT lending platforms like Blur pose a danger by enabling collectors to buy tokens without having the necessary funds. This creates liquidity risks in the future when collection floors suddenly tank.

A liquidity risk arises when a borrower will not have enough cash to meet its financial obligations—in this case, the loan.

Taking on loans on NFTs can require a margin call to avoid liquidation. A margin call occurs when the lender requests additional collateral from you to compensate for the decreased value of the asset.

In 2022, traders were floored after BAYC NFT prices plummeted by 80% in six weeks. Many of them had over-leveraged themselves by using their Apes as collateral for taking loans on BendDAO. Dozens of those who did faced margin calls.