SharpLink posted a $734.6 million net loss for fiscal year 2025, but $756.4 million of that figure came from non-cash accounting charges, not from selling a single Ether (ETH).

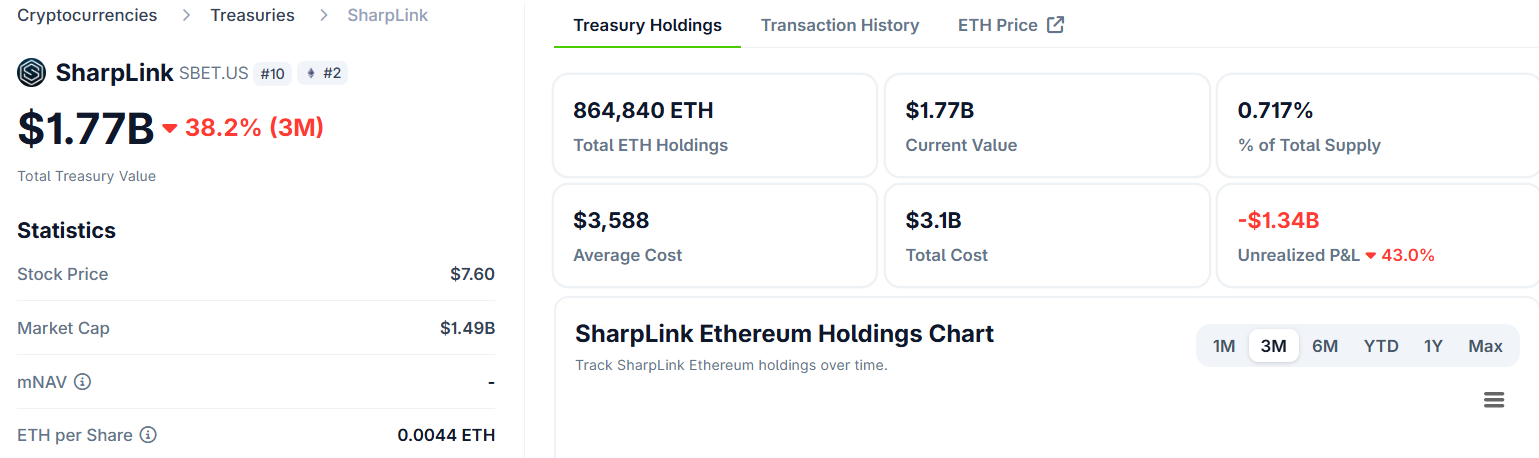

The Nasdaq-listed company (SBET) holds 864,597 ETH in its treasury and operates as a public-market proxy for institutional Ethereum exposure.

Why SharpLink’s Loss Number Misleads

Under U.S. Generally Accepted Accounting Principles (GAAP), companies must mark digital assets to market each reporting period.

For Sharplink, this produced a $616.2 million unrealized loss as ETH prices fell in the second half of 2025.

A separate $140.2 million impairment charge on Liquid Staking ETH (LsETH) compounded the headline figure.

LsETH uses a “historical cost less impairment” model. This means any price drop below acquisition cost triggers a one-way write-down, regardless of subsequent recovery.

Both charges are non-cash. No ETH was sold. The company’s treasury holdings did not shrink.

Meanwhile, a $55.2 million net realized gain from ETH-to-LsETH conversions partially offset the damage, a detail buried beneath the headline loss.

The Staking Engine Accelerates, Then the Flywheel Stalls

The operational picture diverges sharply from the accounting one. Q4 staking revenue reached $15.3 million, up nearly 50% from $10.3 million in Q3 2025. Total 2025 revenue hit $28.1 million, compared with $3.7 million in the prior year.

Since launching its ETH treasury strategy in June 2025, Sharplink has generated 14,516 ETH purely from staking rewards, comprising:

- Approximately 66% from native staking

- 33% from liquid staking, and

- 1% from liquid restaking.

The company also moved treasury management in-house, cutting external management fees and retaining yield margins directly for shareholders.

However, the metric SharpLink calls its “North Star” (ETH per share, or ETH Concentration) tells a more complicated story.

That figure moved from 4.00 in Q3 to just 4.01 in Q4, a near-complete stall after doubling from 2.0 to 4.0 during the summer.

“Every strategic decision is evaluated based on its ability to increase ETH per share,” SharpLink shared in a post.

ETH per share grows when Sharplink raises capital at a premium to Net Asset Value (NAV) and deploys it into ETH.

If the stock trades at or below NAV, that arbitrage disappears. The Q4 stall suggests SBET spent much of the quarter in precisely that position, unable to issue accretive equity.

Institutions Buy In, But Bulls and Bears Diverge

According to Sharplink’s SEC filing, institutional ownership of SBET rose from approximately 6% to 46% during 2025, the highest among publicly traded ETH treasury companies.

Joseph Lubin, Sharplink’s chairman and co-founder of Ethereum, pointed to macro structural demand as the basis for continued growth.

“The institutional adoption supercycle… accelerated in 2025 with global financial institutions launching stablecoins, tokenized real-world assets, and DeFi solutions directly in the Ethereum ecosystem,” wrote Lubin.

As it were, however, the market is split on what the data means. Book of Ethereum argued that Sharplink is proving the corporate treasury model “works even better for ETH” because Ethereum generates native yield. This is a structural advantage over Bitcoin treasury strategies.

Earnings analytics platform Finsee offered a more cautious read, rating the quarter neutral, but acknowledged that the staking operation itself is performing.

“[ETH-per-share stall is] a critical red flag that the capital-arbitrage machine has broken down in current market conditions,” wrote Finsee.

Cash and stablecoin reserves declined to $30.4 million at year-end, down from $37.8 million at the close of Q3.

The company has a $1.5 billion buyback authorization but has not disclosed the NAV threshold that would trigger it.

With Ethereum network upgrades on the horizon and institutions continuing to build positions, Sharplink’s 2026 thesis rests on whether ETH price recovery can reopen the accretive capital-raise window.

Notably, this is the mechanism that drove all of its per-share growth in the first place.