Michael Saylor declared that Strategy generated ₿16,622 of BTC Gain last week, worth roughly $1.2 billion, calling it the closest analog to net income on the Bitcoin Standard.

The claim followed a 22,337 Bitcoin (BTC) purchase between March 9 and March 15, funded primarily through sales of Strategy’s perpetual preferred shares.

What BTC Gain Measures and Why It Matters

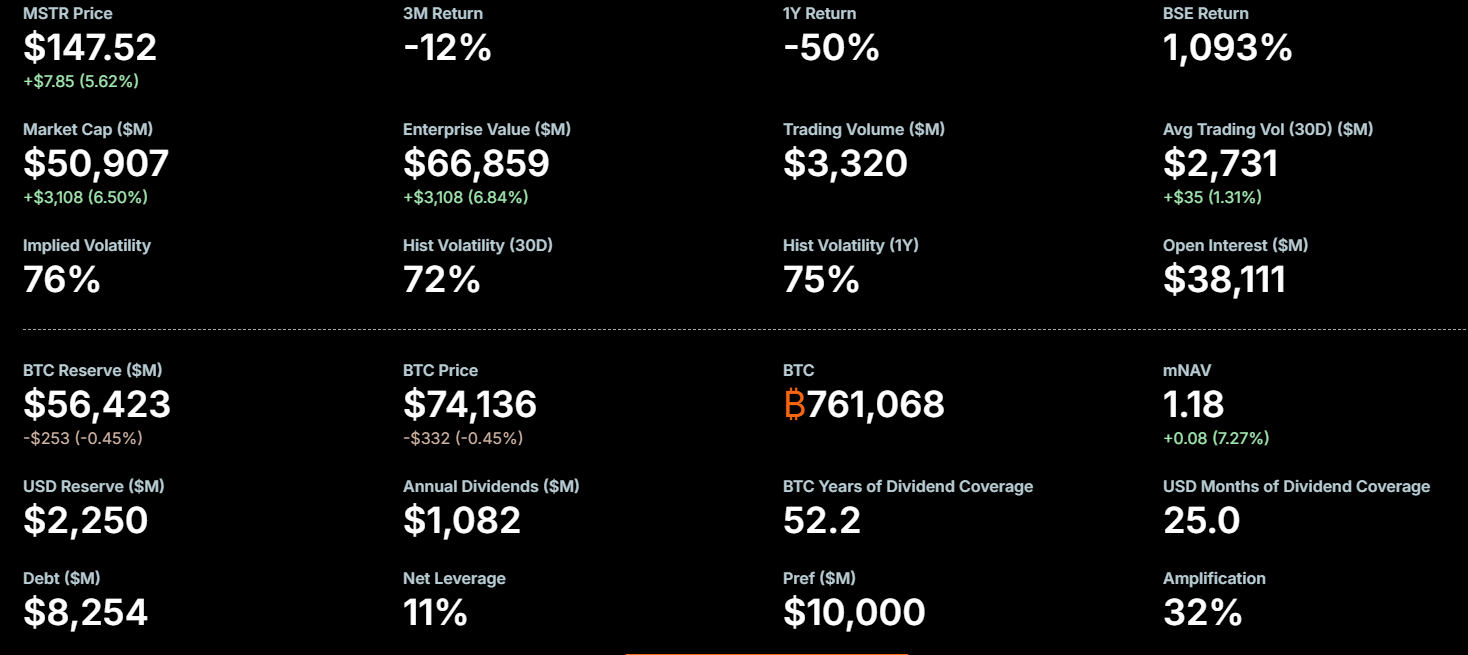

Strategy, formerly MicroStrategy, now holds 761,068 BTC acquired at an average price of $75,696 per coin. That stack represents over 3.5% of Bitcoin’s fixed 21 million supply.

BTC Gain is one of three proprietary KPIs the company uses to report performance. BTC Yield tracks the percentage growth in Bitcoin holdings relative to diluted shares outstanding.

It converts that yield into a Bitcoin-denominated figure. BTC $ Gain translates it into dollars at the current market price.

For the week ending March 15, Strategy reported a 2.3% BTC Yield. Year-to-date, the figure stands at 3.4%, with cumulative BTC Gain of 23,134 BTC.

Saylor argues that dollar-based accounting misrepresents the company’s performance.

Strategy reported a $12.4 billion GAAP net loss in Q4 2025 due to unrealized declines in Bitcoin’s price. Under his framework, the only question that matters is whether each share of MSTR represents more Bitcoin over time.

The Tension Between Accretion and Risk

The $1.57 billion weekly purchase was funded through $1.2 billion in sales of “Stretch” perpetual preferred shares (STRC), which carry an 11.25% annual dividend, and $400 million in common stock sales. This was Strategy’s 12th consecutive weekly buy in 2026.

However, Strategy’s market cap-to-net asset value ratio is roughly 0.98. In the chart above, however, the 1.18 mNAV represents Strategy’s Enterprise Value ($66.859B) divided by its Bitcoin holdings’ market value ($56.376B).

It shows the company trades at a premium of about 18% when accounting for its leveraged structure (debt + preferred stock).

This EV-based ratio highlights the market’s valuation of Strategy’s amplified Bitcoin exposure beyond just equity.

The stock has fallen approximately 69% from its summer 2025 peak. Bitcoin itself trades near $73,500, below the company’s average cost basis.

BTC Gain obscures the cost of capital. The metric does not account for preferred stock dividends, debt obligations, or the senior claims that sit above common shareholders.

In a note to clients, Benchmark analyst Mark Palmer said in late February that STRC is central to Strategy’s funding model, but the instrument’s high yield adds ongoing expense that BTC Gain does not reflect.

Strategy needs roughly 6,158 BTC per week to reach its stated goal of 1 million Bitcoin by year-end 2026. At the current pace, the target requires sustained capital market access and continued investor appetite for equity and preferred issuances through a period where Bitcoin remains below the company’s blended cost.