Three key macro signals just turned, and investors may be underestimating what that means for the next leg of both traditional and crypto markets.

Inflation is steady but not falling, liquidity appears frozen but only temporarily, and the business cycle’s weakest point may already be behind us. December, as analysts warn, could be “very interesting.”

Inflation Holds Steady as Policy Pressure Eases

Real-time inflation data from Truflation, a blockchain-based gauge, indicates that prices are rising at an annual rate of 2.5%, which is near the Federal Reserve’s 2% target. That compares to 2.3% from official BLS data, suggesting inflation has stabilized, not resurged.

Director of Global Macro at Fidelity, Jurrien Timmer, notes that this mild trajectory gives the Fed “more room” to move toward a 3.1% terminal rate. This could open the door to a December rate cut.

However, consumer data continues to show uneven pressure, particularly in the grocery and insurance sectors. This highlights the gap between aggregate inflation and real-world pain.

For markets, stable inflation means less policy tightening, but not yet the kind of deep easing risk assets crave.

Liquidity Looks Dead, But Only for Now

According to HTX’s latest macro report, the US government shutdown has pulled over $200 billion in liquidity from the financial system.

The Treasury General Account (TGA) ballooned from roughly $800 billion to over $1 trillion. This effectively froze government spending and tightened funding across banks and money markets.

That, more than sentiment or risk aversion, explains why liquidity “looks dead,” as Milk Road put it. The moment Congress resolves the shutdown, that $1 trillion floodgate reopens, potentially unleashing a surge in both fiscal and market liquidity.

“Once the shutdown ends, spending should resume — and liquidity should expand,” Milk Road’s analysts wrote. “That should be bullish.”

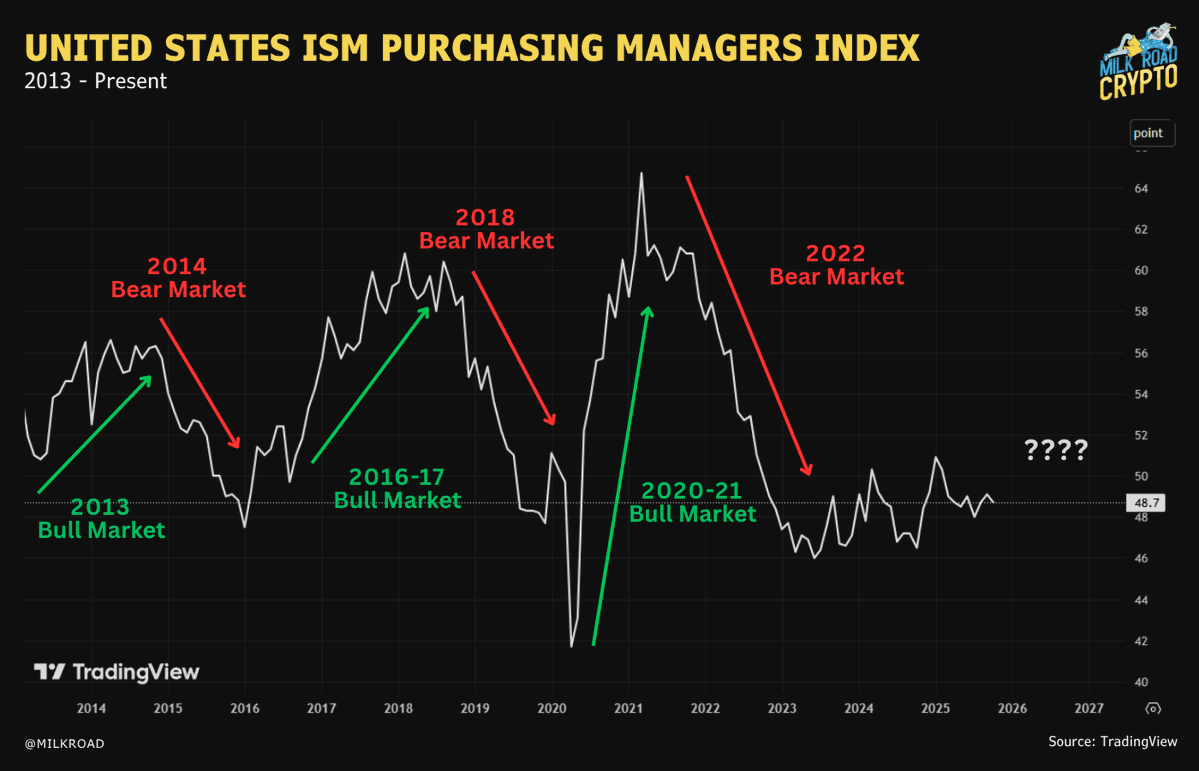

The Business Cycle Turns Beneath the Surface

While the ISM Manufacturing Index remains below 50, still in contraction territory, New Orders climbed from 48.9 to 49.4. It’s a small uptick, yet historically, this indicator turns higher before broader growth recovers.

Any ISM Purchasing Managers Index (PMI) value below 50 represents contraction for the sector. This result feeds a narrative of economic weakness that impacts sentiment toward riskier assets.

This difference between current and future orders creates some uncertainty about the economic outlook. These three signals deliver a nuanced market setting:

- Inflation remains stable, creating room for policy adjustments.

- Manufacturing is weak, but forward-looking areas are improving.

- Liquidity remains frozen but is likely to be released.

Once the government resolves its shutdown, the market may see quick and notable shifts.