The long-anticipated clash between crypto and traditional banking systems officially started with the passage of the GENIUS Act. The legislation’s impact is already evident—within two weeks, retail giants like Amazon and Walmart are considering launching their own stablecoins.

Kronos Research CEO Hank Huang told BeInCrypto that if more companies adopt this trend, banking systems will have to adapt quickly, especially as money shifts away from traditional deposits. However, consumers who switch to retail-backed stablecoins won’t have the same protections conventional banks offer.

A New Era for Crypto Integration

The GENIUS Act represents a historic shift in how cryptocurrency, specifically stablecoins, will integrate into US financial markets. It ensures stablecoins are backed by real assets and subject to strong oversight while acknowledging their potential to innovate payments.

Among the bill’s most important provisions is a clear stipulation that only insured depository institutions, including banks and credit unions, and certain approved non-bank entities will be authorized to issue. It also strictly prohibits algorithmic or unbacked stablecoins to ensure stability and consumer trust.

Since the legislation was passed, several high-profile retailers have shown interest in launching company stablecoins. Reports are circulating that corporate giants like Amazon and Walmart are seriously considering this step.

Several motivations are probably driving their reasoning.

Retail Giants’ Motivations for Stablecoins

Retailers like Amazon and Walmart boast an enormous customer base, generating billions in daily revenue from purchases alone. Many customers pay using traditional credit card networks such as Visa and Mastercard.

While these networks typically charge interchange fees of 2-3% per transaction, for companies with such massive transaction volumes, these fees can accumulate to billions of dollars annually.

Powerhouse companies can bypass these networks by issuing their own stablecoin, significantly reducing or eliminating these costs.

At the same time, removing payment network intermediaries, such as banks, would drastically speed up settlement times. Since stablecoins are built on blockchain technology, they can facilitate nearly instantaneous settlements, leading to much better cash flow and efficiency for companies and their suppliers.

In the context of international transactions, retail-backed stablecoins would offer streamlined global payments, offering a less costly alternative to traditional cross-border payment methods, which often involve foreign exchange fees. Such a move would also inherently expand retailers’ customer base.

A proprietary stablecoin could also be integrated into loyalty and rewards programs, offering customers unique incentives or discounts. It could also open doors to new financial service offerings.

“Frictionless rewards and cost-saving, consumer-centric perks will fuel the shift. With preferred perks and practical utility, stablecoins steal the spotlight, they will chase yield over idle deposits,” Huang told BeInCrypto.

These numerous advantages prompt questions about how this new payment traffic might impact traditional banking services.

Stablecoins’ Disruptive Impact on Traditional Banking

The widespread adoption of retailer-backed stablecoins could significantly disrupt traditional banking, mainly by diverting money away from conventional deposits.

If Amazon or Walmart issues a stablecoin, consumers might opt to hold their purchasing power in these stablecoins rather than in traditional bank accounts. Instead of keeping money in a checking account to pay for groceries or online shopping, a consumer might transfer those funds into an Amazon or Walmart stablecoin wallet.

This shift would directly reduce the money held as deposits in traditional banks. Since these deposits are any bank’s lifeblood, a significant outflow would shrink their funding base. In turn, it would affect their ability to lend money to existing customers and businesses.

“Consumers will shift from TradFi to chains seamlessly seeking familiar, fast, and flexible rails. Retail coins will drain liquidity from banks into branded crypto networks,” Huang said.

In short, their overall economic activity would considerably decrease.

“The GENIUS Act levels the playing field with strict standards on reserves, regulation, and issuer eligibility. Banks gain ground with trusted frameworks, while non-bank entrants face tight rules. Ultimately, it’s a liquidity battle where the strongest survive,” Huang added.

Aware of these dangers, how will traditional banks adapt their strategies to remain competitive?

How Can Banks Adapt to the Digital Shift?

To some extent, banks have been experiencing generalized deposit displacement for a while now. Stablecoins might accelerate that trend further. Traditional banks have already been actively striving to meet the growing demand for digital banking in recent years.

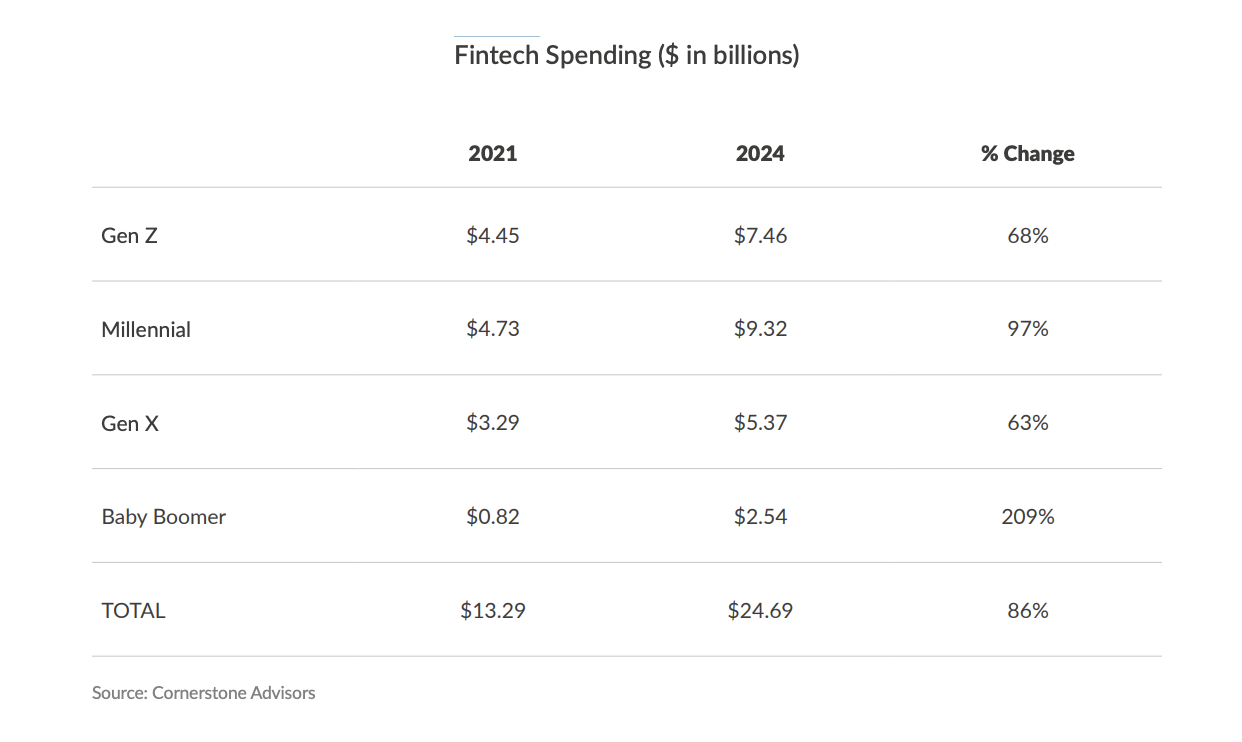

A recent report by Cornerstone Advisors highlights a significant surge in fintech spending across all generations. From 2021 to 2024, fintech spending among Gen Z, Millennials, Gen X, and Baby Boomers collectively jumped 86%, from $13.29 billion to $24.69 billion.

Some banks have already made significant strides to prepare for the anticipated widespread adoption of retail-backed stablecoins. JPMorgan Chase, for instance, has been preparing for this shift for years.

“Banks like JPMorgan won’t just defend deposits, they will leveraging trusted infrastructure to create fast, secure digital dollars that unlock new revenue, and deepen client benefits,” Huang said.

Starting with the launch of JPM Coin in 2019, JPMorgan pioneered the concept of a bank-issued digital currency for wholesale payments, leveraging private blockchain technology within their Kinexys unit to enhance efficiency and accelerate interbank settlements.

Following the passage of the GENIUS Act, it has now announced its latest strategic step: the introduction of JPMorgan Deposit Token (JPMD), which will be piloted on Coinbase’s public Base blockchain.

This move is particularly significant as JPMD is positioned as a fully insured and notably interest-bearing digital representation of bank deposits.

This directly contrasts with the GENIUS Act’s prohibition on non-bank payment stablecoins from paying interest to holders, a provision critics argue is a concession to incumbent banks.

JPMD’s ability to offer yield aligns with the new regulatory clarity. It offers institutional clients a compliant and highly integrated alternative to traditional stablecoins for on-chain settlements and cross-border B2B transfers.

It also clearly shows how a bank can use its existing strengths to maintain its strategic advantage against this new competition.

The Critical Role of FDIC Insurance

Due to their existing infrastructure, resources, and unique regulatory protections, banks possess a strong foundation for adapting to shifts in the financial sector.

“TradFi banks must build bridges between legacy and digital—deploying deposit tokens, boosting blockchain-backed benefits, and bundling security with seamless convenience. To lock liquidity in, banks need to blend innovation with insurance,” Huang told BeInCrypto.

This possibility is especially critical given the disparities in consumer protection between traditional banks and stablecoin issuers that are not banks. Traditional banks offer Federal Deposit Insurance Corporation (FDIC) protection, which insures deposits up to $250,000 per depositor. This insurance, backed by the US government, is the strongest guarantee available in the financial world.

FDIC insurance does not apply to stablecoin issuers outside the banking industry. While the GENIUS Act aims to ensure robust reserves and audits for stablecoins, a “run” on an issuer could still lead to operational issues, liquidity problems, or even the stablecoin losing its $1 peg. In such cases, recovery relies on the issuer’s solvency and operational integrity.

In contrast, if an FDIC-insured bank fails, insured deposits remain safe. The FDIC intervenes to ensure principals are not lost, which is the core purpose of deposit insurance: protecting consumers from bank failures.

“Without deposit insurance, consumers face security risks and liquidity slippage, with unclear transparency on real reserves. During big redemptions, stablecoins may struggle to stay stable under pressure,” Huang added.

By leveraging this significant advantage, banks can maintain a strong appeal to consumers who prioritize guaranteed deposits.

The Future of Finance: A Hybrid System

The emergence of stablecoins, especially those from large retailers or non-bank entities, marks a significant shift in the financial industry. This development could influence the future of the traditional banking model and alter conventional capital flows.

Each player has unique advantages, making the panorama all the more competitive. Though the outcome will likely be a hybrid financial system, non-bank and bank entities alike will have to earn their spot or bleed slowly.

The ultimate winners will be those who best combine technological innovation with trust, security, and regulatory compliance.