The Fed’s resumption of balance sheet expansion objectively benefits the stock market, while simultaneously weakening the US dollar and driving a sustained long-term rise in gold and silver prices, with the euro also benefiting. However, apart from a few cryptocurrencies like Bitcoin, the crypto market, as a dollar-denominated offshore equity-like market, struggles to compete with precious metals and stock indices due to investors’ limited risk appetite. Therefore, further reducing its allocation may be a better option.

A Not-So-Dovish Decision

Yesterday, the Federal Reserve announced the outcome of its final FOMC meeting of the year. Although officials delivered a rate cut for the third consecutive meeting, there is unusual discord within the ranks regarding whether inflation or the labour market poses the greater concern. Consequently, officials have signalled little appetite for further easing.

Public comments from Fed officials in recent weeks reveal a committee so deeply divided that the final decision may well hinge on how Chair Powell chooses to steer the ship. With Powell’s tenure set to expire next May, he will preside over only three more FOMC meetings. Sticky price pressures coupled with a cooling labour market present the Fed with an invidious trade-off—a dilemma not encountered in decades. During the “stagflation” era of the 1970s, when faced with a similar predicament, the Fed’s “stop-start” response allowed high inflation to become entrenched.

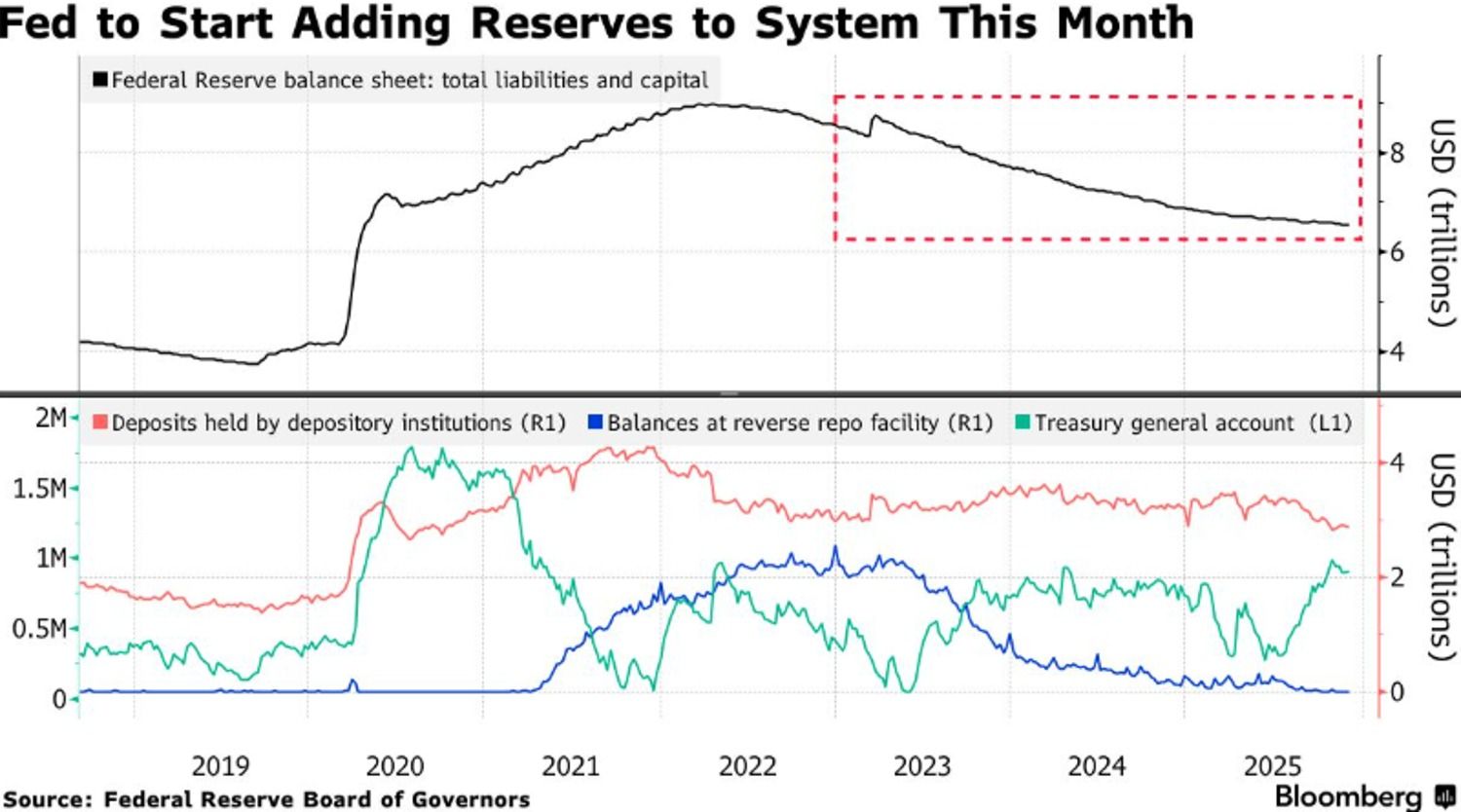

Against this backdrop, several Fed actions warrant close attention: firstly, the removal of the aggregate cap on the Standing Repo Facility (SRF); and secondly, the purchase of Treasury bills (T-bills) — and, if necessary, other US Treasuries with a remaining maturity of up to three years — to maintain ample reserves.

The Fed’s objective is crystal clear: it is not to provide premium liquidity for equity and crypto markets, but to stabilise short-term liquidity levels within the banking system and alleviate market shortages. T

he projected purchase of $40 billion in T-bills this month, combined with the relaxation of the SRF, objectively helps to steady equity markets, yet is unlikely to fuel a broad-market rally comparable to that of 2021.

Powell also emphasised that current T-bill purchases are solely for “reserve management”, implying the primary aim of the Fed’s balance sheet expansion is to maintain stability, not to unleash further liquidity to stimulate the economy and asset prices.

What is the Smart Money Thinking?

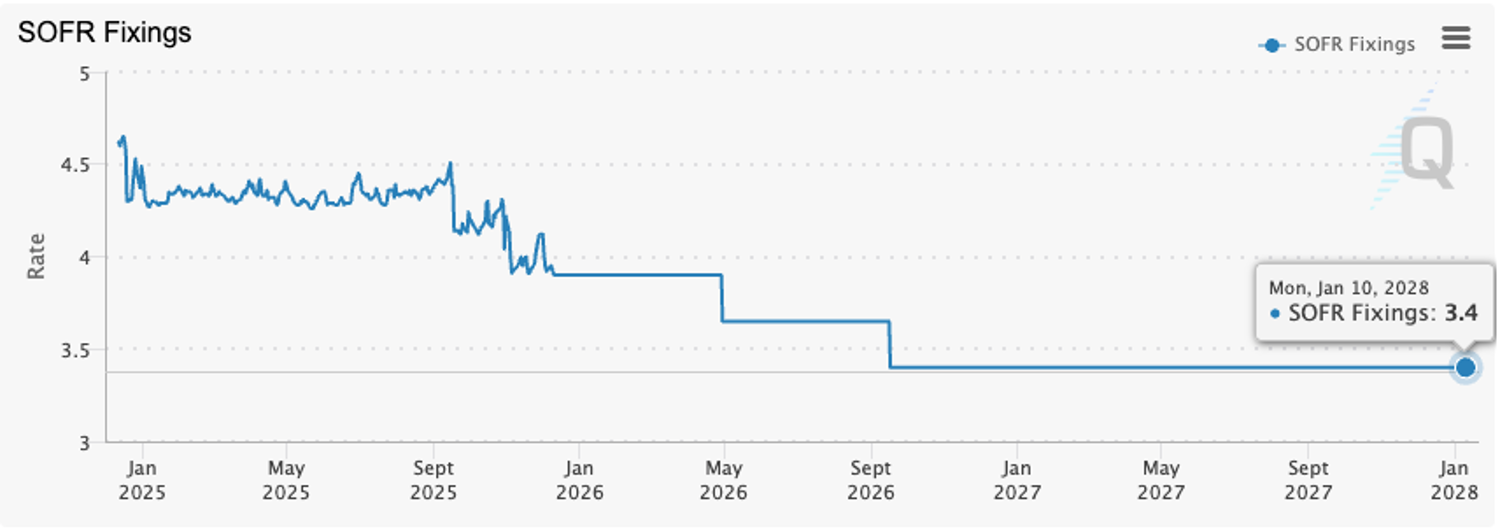

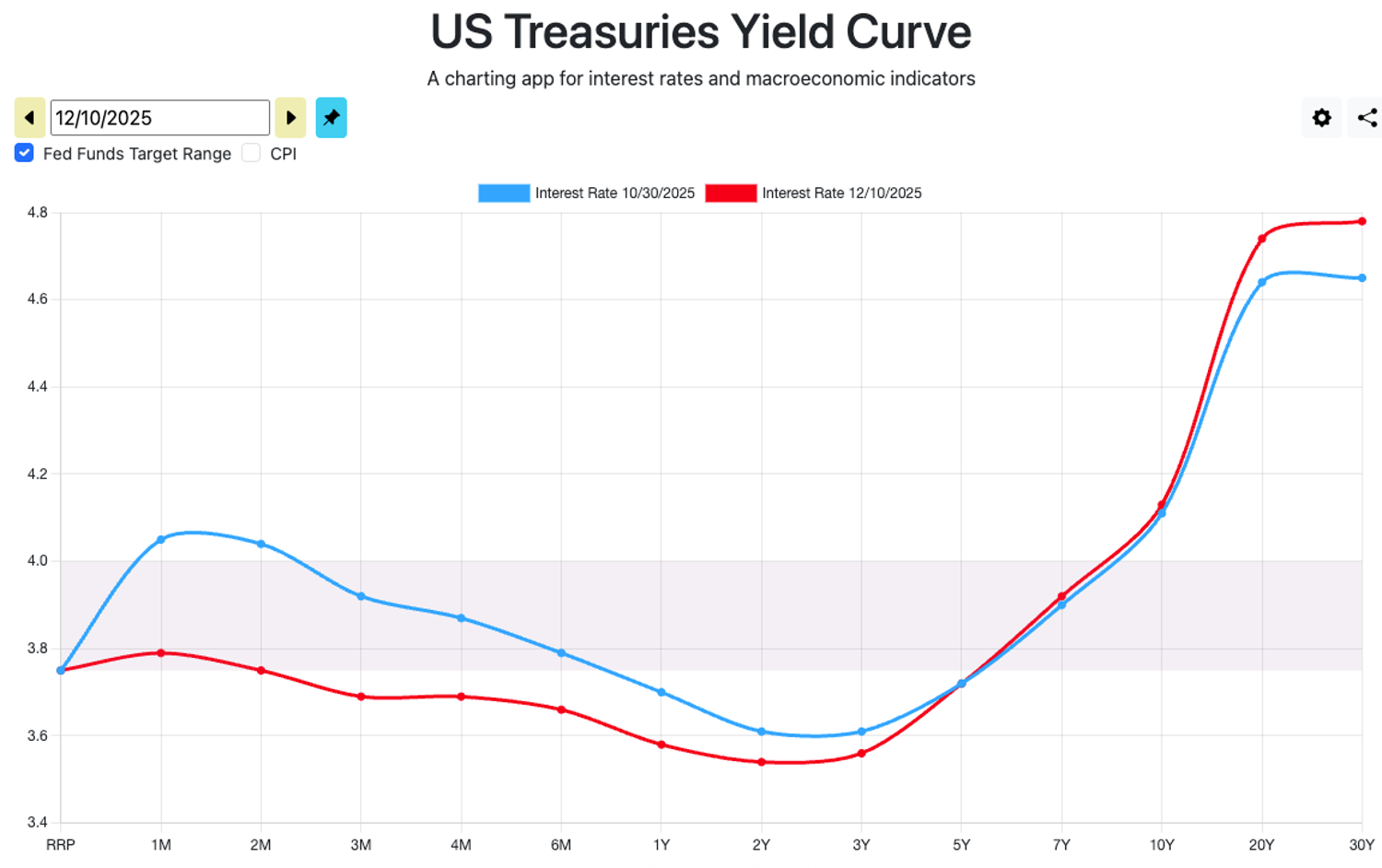

In the rates market, traders are pricing in more conservative expectations than they were before the FOMC meeting. Markets now anticipate only two cuts in 2026, of 25bps each, with no further easing expected until January 2028, leaving the terminal rate hovering around 3.4%. Bond market pricing is even more explicit: since late October, only yields on Treasuries with maturities under three years have fallen, whilst the 10-year yield remains stubbornly above 4.1%, and T-bond yields have actually risen significantly. This implies that long-term financing costs remain elevated, and riskier markets and assets will continue to face a liquidity drought for the foreseeable future.

Source: CME Group

Source: ustreasuryyieldcurve.com

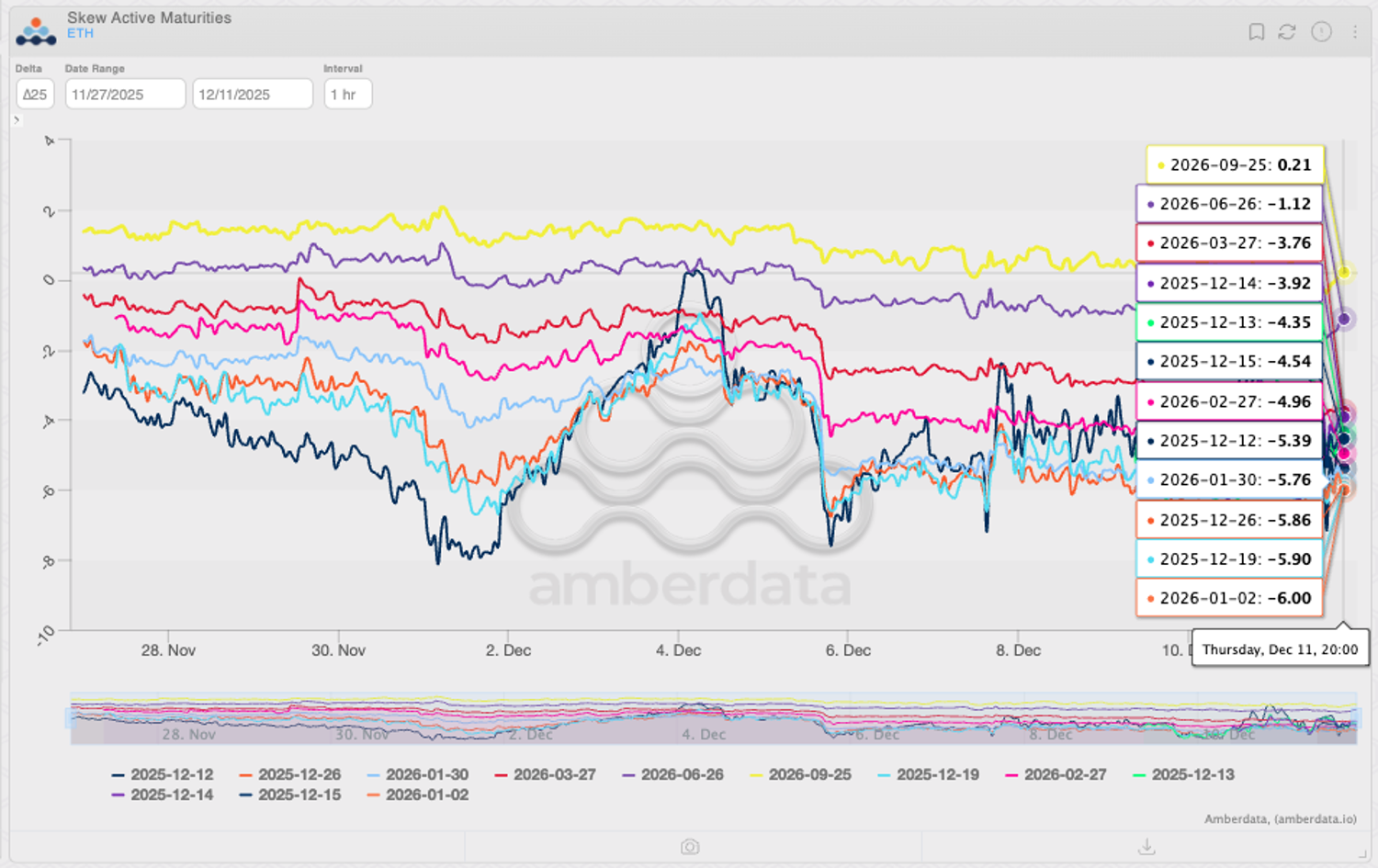

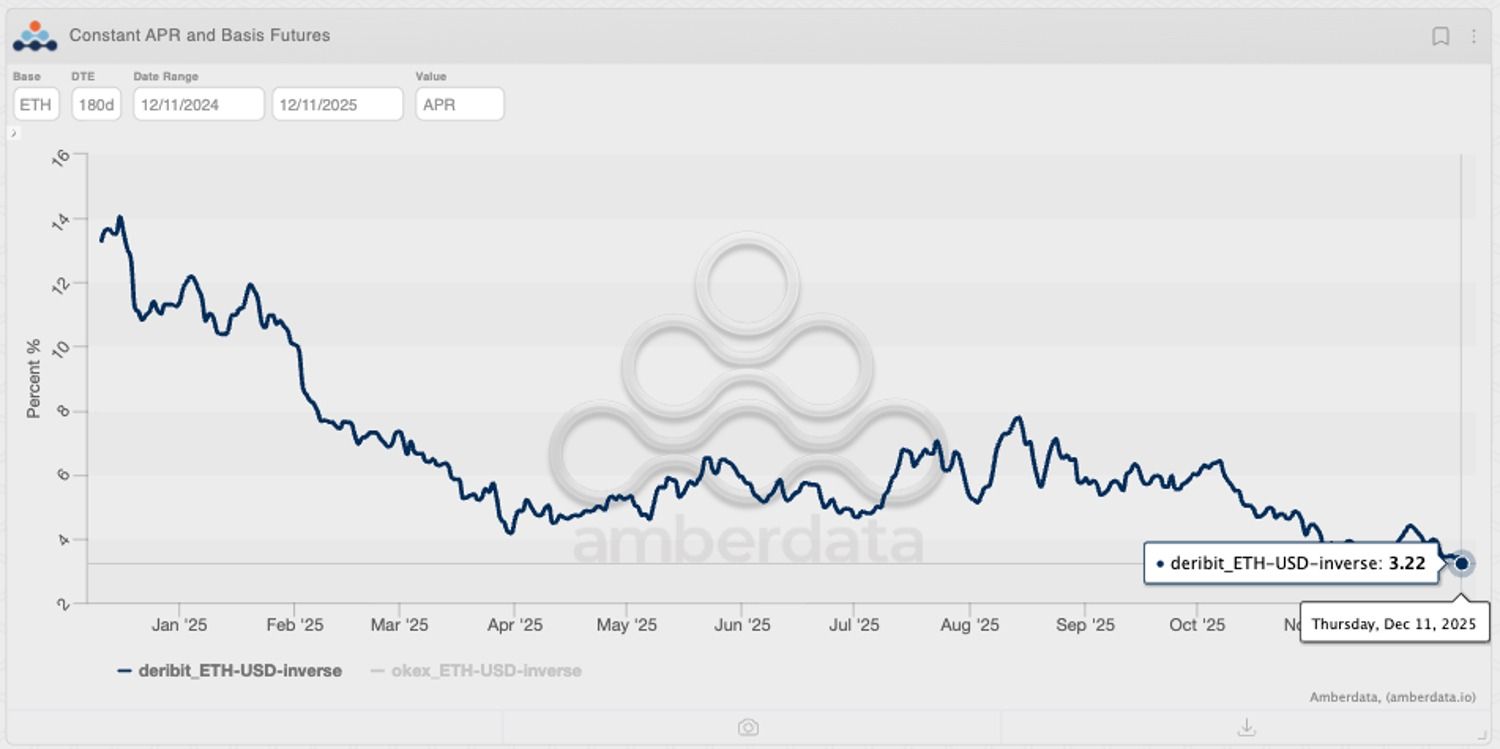

In the crypto options market, traders’ long-term bearish stance on BTC and ETH has not shifted; if anything, it has entrenched. Bullish sentiment is confined to short-term speculation in 0DTE options. Notably, the previously persistent far-month bullishness for ETH has evaporated, with sentiment shifting into “neutral-to-bearish” territory. This suggests that traders view ETH’s short-term rebounds not as a reflection of improving fundamentals, but rather as a product of speculative flows. Given that ETH’s implied forward yield sits at just 3.51%—compared to roughly 4.85% for BTC—current valuations do not represent a “reasonable investment proposition” for institutions, whilst BTC is viewed, at best, as a “hold”.

Source: Amberdata Derivatives

So, What’s the Trade?

For the crypto market, the Fed’s stance is hardly welcome news. In the current environment, sustained, large-scale rallies rely more on a deluge of long-term liquidity than on short-term relief measures. Meanwhile, elevated long-term rates will keep long-term investors cautious and on the sidelines, leaving price action to be dictated primarily by short-term speculators.

Short-term rebounds and long-term bearish expectations will coexist. For assets where traditional institutional pricing power is dominant (BTC, XRP, SOL), long-term bearish expectations will continue to weigh on prices. However, for assets where institutional influence is weaker (such as ETH and altcoins), leverage-induced short-term rallies will drive price movements.

Therefore, incorporating far-month put protection for crypto assets remains a prudent strategy. However, the cost of hedging warrants reconsideration. Yields from the crypto carry trade can no longer cover the cash flow requirements for put protection.

Consequently, holding assets that are still in a robust uptrend (e.g., the “Mag 7”) and using their gains to fund “insurance premiums” appears to be a sound approach. The beta of the Mag 7 is typically lower than that of BTC and ETH, meaning that when equities rise, their gains can offset option premiums.

Conversely, if markets fall, the higher sensitivity of crypto assets means that far-month puts will generate superior returns.

Of course, reducing exposure to crypto risk is also essential. With BTC’s implied forward yield now virtually indistinguishable from T-bond yields, holding crypto assets per se offers little comparative advantage. If one must maintain long exposure, consider the following structures:

- Risk Reversal: Use a portion of previous profits to enter a risk reversal structure expiring in 30-60 days (i.e., sell a put and buy a call with the closest absolute delta), whilst retaining ample cash.

- Roll Over: Once the price rises significantly and appropriate gains are secured (at the investor’s discretion), roll the position over.

- Capture the Skew: If price movement is muted, investors can still profit from the spread between the two options near expiry due to the significant negative skew, before rolling over.

- Buy the Dip: If prices fall significantly, use the cash collateral to accumulate the underlying asset at lower levels.

The implied forward yield of ETH has not been as good as that of T-bills. Source: Amberdata Derivatives

Furthermore, considering the risk of USD depreciation, holding Euros as a cash reserve is a proper alternative. With the Fed still in a cutting cycle, the Euro’s long-term outlook remains constructive.

Simultaneously, as European inflation shows signs of a slight rebound, the ECB is likely to lean towards holding rates steady, whilst the Bank of Japan may intervene to sell USD to combat a weak Yen and inflation. This significantly increases the probability of the Euro appreciating in the near term.

In summary, the rate cut has not fundamentally altered the crypto landscape. Any sharp rally lacking fundamental support should be viewed as a risk rather than an opportunity.

Closely monitoring leverage indicators, such as open interest, and tightening risk parameters may be the optimal strategy for navigating this uncertain festive season. Adopting a defensive posture is also advisable. After all, in this market, “survival” takes precedence over betting on a “Santa rally”.

Disclaimer: The information provided herein does not constitute investment advice, financial advice, trading advice, or any other sort of advice, and should not be treated as such. All content set out below is for informational purposes only.