Digital Asset Treasury (DAT) firms have emerged as a key narrative in 2025, with many institutional players betting big on digital assets as part of their balance-sheet strategies. However, the volatility in crypto markets has put these treasury models to the test.

This raises a critical question: Are firms truly strong enough to sustain their digital asset treasury strategies—or have many simply copied (Micro) Strategy’s high-profile playbook amid the hype? To find out, BeInCrypto consulted several leading experts to delve deeper into whether these companies can endure the current market environment or risk triggering broader systemic stress.

What Are DATs?

DAT firms, or Digital Asset Treasury companies, are publicly traded companies that acquire digital assets as a core part of their business strategy. Strategy (formerly MicroStrategy) started this trend in 2020 by accumulating Bitcoin. Soon, many more followed.

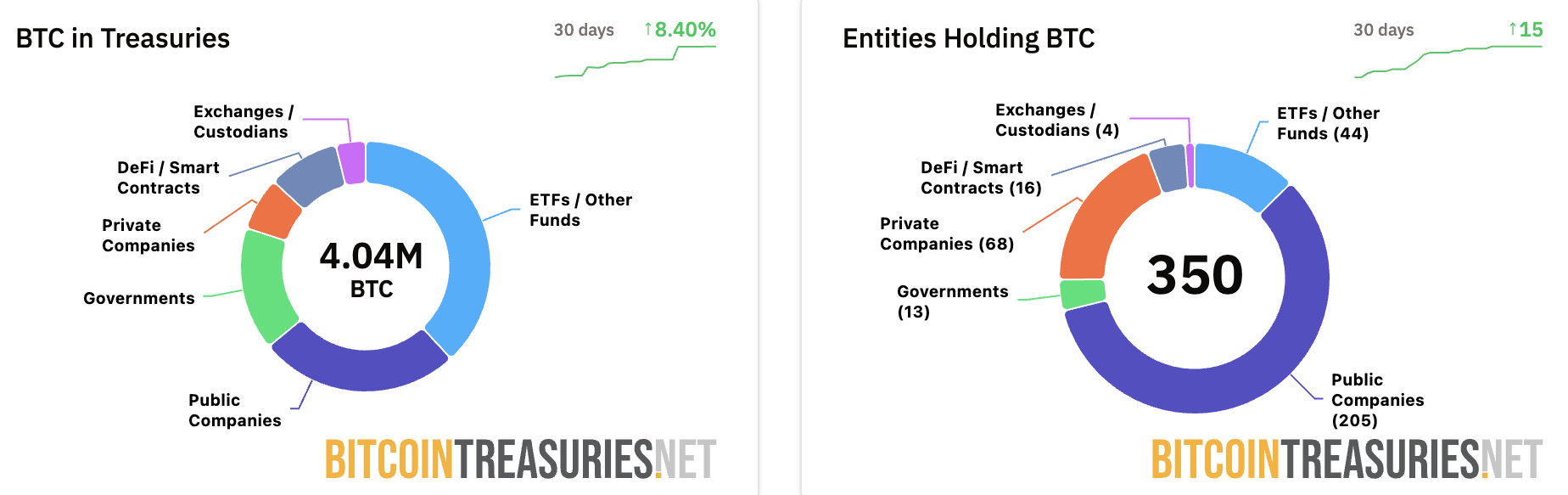

According to the latest data from Bitcoin Treasuries, 205 public companies hold BTC on their balance sheets. Furthermore, overall public companies hold over 1 million Bitcoins, with Strategy alone controlling 640,418 BTC.

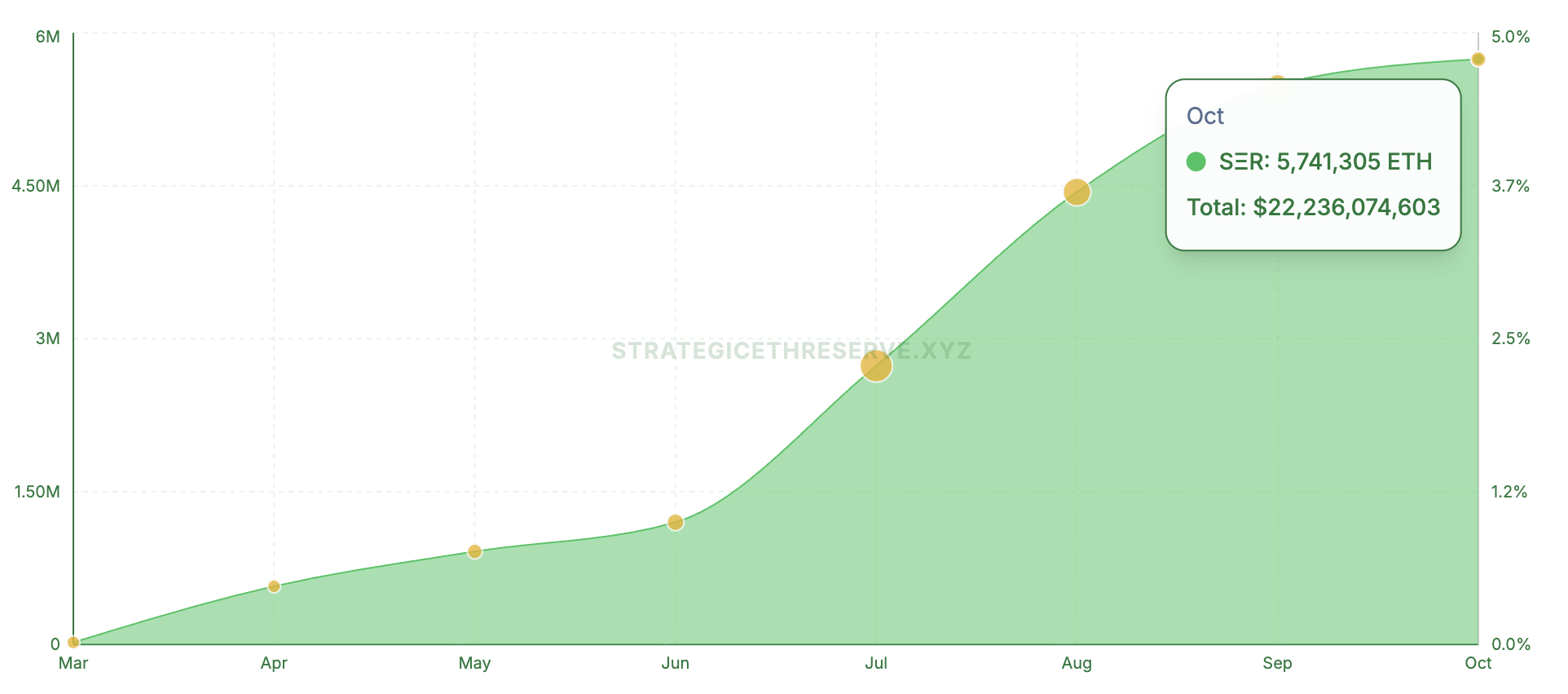

The trend extends beyond BTC. Strategic ETH Reserve data showed that 16 public firms control over 4.75% of Ethereum’s current supply and have committed over $22 billion.

Similarly, Solana-focused firms have invested $3.76 billion in the asset. BeInCrypto recently reported that DATs collectively manage $105 billion in the three asset classes.

Corporate Crypto Portfolios Tested by Falling mNAVs

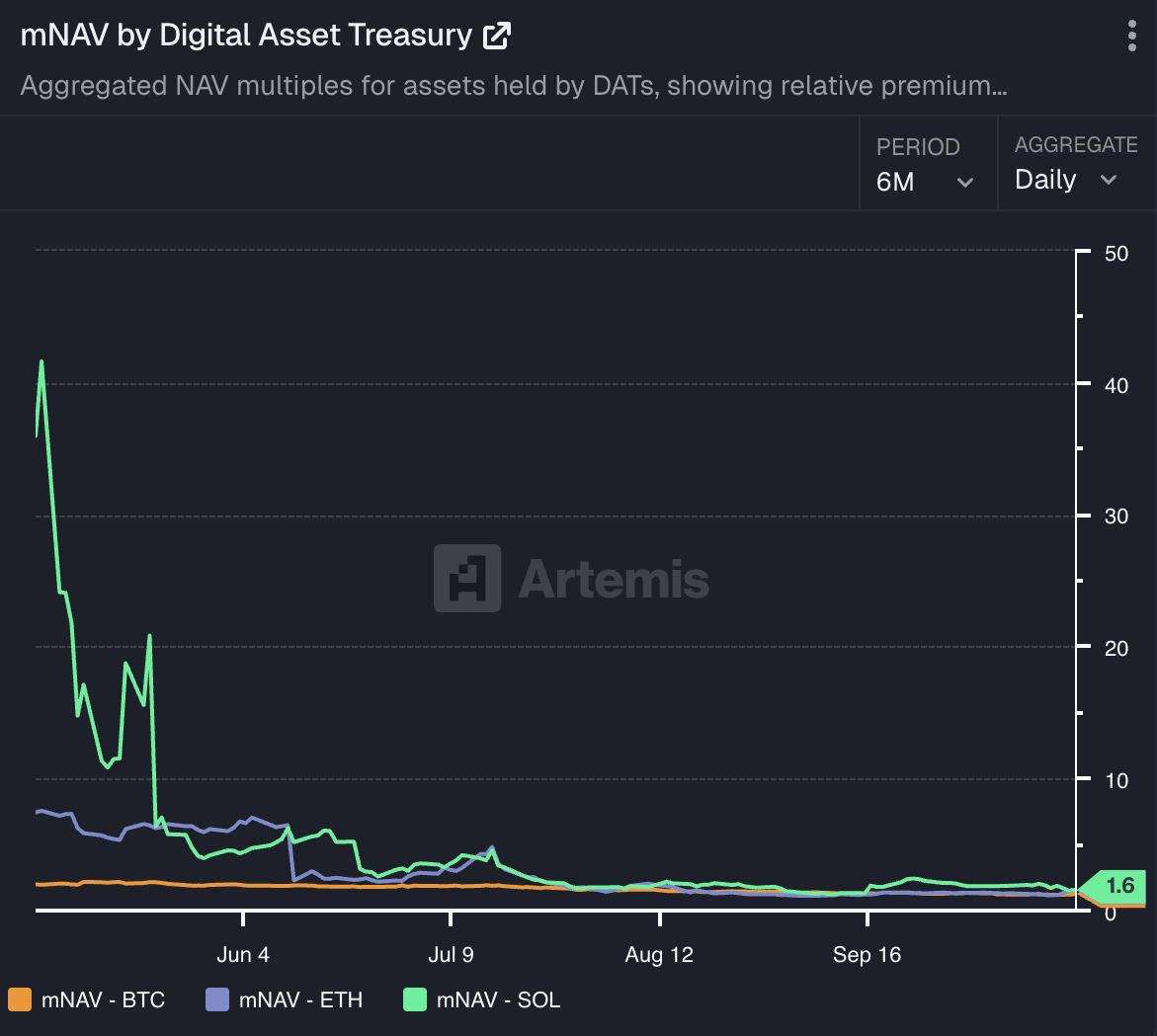

While the funding scale reflects confidence in these assets, holding them has not been without challenges. Artemis Analytics data shows that the mNAV of companies holding BTC, ETH, and SOL has continued to drop sharply, hitting new lows.

In fact, after the market crash, Metaplanet’s mNAV fell to 0.99, marking the first instance of the metric falling below the 1.0 threshold. While it recovered shortly after, the drop still raises concerns. Similarly, other firms faced similar setbacks.

Fakhul Miah, Managing Director of GoMining Institutional, told BeInCrypto that companies holding digital assets like Bitcoin operate in a volatile, mark-to-market environment, so price drops don’t imply insolvency if they’ve planned for market cycles.

Well-managed treasuries run stress tests, keep liquidity reserves, and align funding with long-term goals — unlike those built on short-term price momentum.

“It’s also important to note that the mNAV declines we’re seeing aren’t purely a reflection of recent Bitcoin price weakness, though BTC has since recovered. Many of these companies were initially priced for perfection during their early accumulation phases, when market sentiment and FOMO drove their market caps far ahead of fundamentals. As such, when BTC prices corrected, their mNAVs naturally reacted more sharply, reflecting the same volatility that propelled their earlier gains,” he added.

He noted that as the market matures and corporate balance sheets align more closely with Bitcoin’s underlying fundamentals rather than speculative valuations, volatility is likely to stabilize over time.

Timot Lamarre, Head of Market Research at Unchained, argued that Bitcoin treasuries are fundamentally different from altcoin treasuries, which often exploit retail investors.

“Even for bitcoin treasury companies, it should be expected that for the vast majority of companies, mNAV will trend toward one over time,” he said.

Lamarre also pointed out that a few firms may thrive by giving indirect Bitcoin exposure to investors who can’t buy it directly. Still, ultimately, the most successful treasuries will be those that hold Bitcoin directly — without leverage or complexity.

How Much Risk Do Declining mNAVs Pose to Corporate Balance Sheets?

Nonetheless, if mNAVs continue to decline, could that pressure firms to sell their holdings and, in turn, trigger market volatility? According to experts, this is indeed possible. Speaking to BeInCrypto, Fabian Dori, CIO at Sygnum Bank, said,

“Basically, this risk exists. The likelihood of it happening mainly depends on the debt structuring of the individual companies. To monitor the likelihood the market attaches to a ‘forced de-leveraging’ scenario, it might for example, be interesting to analyze the credit spread of (convertible) bonds relative to the broader market and relative to peers, or the implied volatility term structure and skew for options on the company,” he mentioned.

In addition, Lamarre detailed that the major participants in the Bitcoin treasury space — such as Strategy — maintain strong collateral positions and could withstand even a significant decline in Bitcoin’s price without being forced to liquidate. Smaller firms, however, that take on excessive leverage could spark short-term turbulence in the market.

“The larger risk lies with the treasury company’s stockholders rather than bitcoin holders. Bitcoin holders can ride out bear markets with bitcoin held in self-custody, where companies can go under. Past catalysts for massive bear markets have been fraud and hacks,” the analyst noted.

Miah agreed, saying that some forced selling could happen at the margin. Nevertheless, it’s unlikely to threaten the system unless a major player, such as Strategy, faced a default.

In his view, the current market is actually helping to strengthen the ecosystem by recrepricing risk where governance was weak and capital mismatched. Well-structured firms can handle short-term pressure without disrupting the market, making this more of a refinement phase than a credit crisis.

Is Corporate Exposure to Digital Assets Jeopardizing Shareholder Value?

Beyond declining mNAVs, digital asset treasuries also face the risk of their stock performance being closely correlated with crypto market movements, which can lead to volatility.

Dori highlighted that a digital asset treasury’s stock price is driven by volatility in its underlying token on a daily basis. Structurally, this makes DATs a ‘high-beta bet’ to the assets they hold.

“From a longer-term perspective, each DAT needs to create value to shareholders to justify a sustainable mNAV premium. This idiosyncratic value or risk is driven by company-specific choices: issuance discipline, capital structure, cash flow planning, operational execution, etc,” he added.

However, Miah stressed that equity weakness among DAT firms stems more from how their capital and exposure are structured than from Bitcoin’s price movements alone. Investors can tolerate volatility when they trust a company’s balance sheet — what they reject is dilution and reactive financing.

“The difference between strong and weak performers lies in treasury governance, how leverage, capital raises, and timing are managed. A well-structured company can weather price swings while maintaining investor confidence,” he mentioned.

Furthermore, Lamarre believes that Bitcoin treasury companies may be appealing to traders typically drawn to the high-risk nature of altcoins. According to him,

“Bitcoin’s downward volatility usually follows a euphoric upside phase, which we have yet to see in this cycle. Altcoins appear to be continuing their decline in bitcoin terms. Perhaps these bitcoin treasury companies are scratching the itch for traders who are typically attracted to the risk of altcoins. It may be a poor strategy that has led to stock prices going down, but the game they are trying to play is hard. Once you understand Bitcoin, the idea of buying a company’s stock for exposure feels redundant. Holding your own bitcoin reduces counterparty risk in a way equity can’t.”

Another concern stems from the selling pressure that arises when PIPE shares enter the market. For example, BeInCrypto recently reported that KindlyMD’s stock plunged 55% following the release of new shares into circulation.

The PIPE Dilemma

CryptoQuant found that Bitcoin treasury companies raising funds through PIPE programs saw their share prices drop by 42% to 97%, mainly due to actual or anticipated selling by PIPE investors. It also warned that some stocks could fall up to another 50%, as they still trade above their PIPE offering prices.

Nonetheless, Miah explained that PIPEs or equity offerings are not inherently problematic — the issue arises when they are used reactively rather than strategically.

“When equity raises are paired with risk-managed Bitcoin exposure, the structure can be accretive. But without a clear capital allocation plan or investor communication, it erodes trust. The issue isn’t the use of capital markets; it’s how the capital stack is engineered,” the executive remarked.

Lamarre emphasized that the most secure treasury approach remains simple — generate profits and allocate a portion to Bitcoin. When firms issue new equity solely to purchase more Bitcoin, shareholders should question whether they’d be better off holding the asset directly.

He revealed that while financial engineering can benefit investors unable to hold Bitcoin themselves, historical results show that such strategies rarely outperform Bitcoin’s own returns. For most investors, the cryptocurrency’s consistent 60%+ compound annual growth rate makes the case for direct ownership compelling.

What It Takes to Build a Successful Digital Asset Treasury

While the risks are clear, they don’t invalidate the Digital Asset Treasury model. Strategy stands out as a notable example.

Miah detailed that the firm’s success was not just about conviction in Bitcoin but execution. The company paired belief with sound architecture: recurring revenue, long-dated financing, and governance alignment.

Many of its imitators, he noted, saw the headlines but missed the foundation. They tried replicating the exposure without matching liquidity, cash flow, or investor profile.

“A sustainable Bitcoin treasury isn’t about mirroring strategy; it’s about matching design to capacity. Firms that approach this as a capital allocation problem, not a branding exercise, are evolving the model correctly,” the GoMining Institutional executive disclosed to BeInCrypto.

He underlined that digital assets amplify whatever is already in place. A company with stable operating cash flow can use Bitcoin as productive collateral — a tool to enhance yield or diversify reserves.

However, crypto exposure only magnifies financial stress for firms with weak fundamentals. Treasury strategies succeed when backed by consistent revenue, predictable financing, and strong risk controls. They fail when treated as substitutes for growth.

This principle is especially relevant in today’s environment, where Bitcoin operates within a mature institutional ecosystem of ETFs, custodians, and regulated derivatives. That infrastructure makes Bitcoin uniquely suitable as a balance-sheet asset. Broader digital-asset strategies often lack the same liquidity depth or policy clarity, limiting their integration into traditional treasury frameworks.

Lamarre shared that the foundation of any sustainable treasury is profitability and prudent capital management.

“Profitability is essential to sustainably growing bitcoin treasuries. This applies to both individuals and public companies. The goal is to earn more than you spend. Bitcoin reinforces fundamentals that have been lost in a fiat monetary system. Instead of emphasizing growth over profitability, Bitcoin rewards efficiency and disciplined saving for the future,” he claimed.

Nevertheless, according to him, there may be room for select Bitcoin treasury companies in different jurisdictions where regulatory or capital allocation limits prevent direct investment. However, the broader market doesn’t need an excess of such entities.

“Bitcoin stands as the most powerful, long-term savings vehicle for individuals and public entities alike. Diluting shareholders to acquire more bitcoin has to provide value on the other end of that trade. What are you providing to the market that they can’t find elsewhere,” he stated

(Micro) Strategy Started a Trend — But Can Others Survive?

Thus, while launching a Digital Asset Treasury may be simple, surviving in the market requires far more. According to Miah, current market conditions distinguish between treasuries structured for sustained conviction and those driven by momentum.

“The next Bitcoin bear cycle will likely wipe out a portion of weaker players, particularly those in the broader multi-asset DAT space, leaving behind better-capitalized and operationally disciplined firms. The steepest drawdowns tend to occur outside Bitcoin exposure. Bitcoin treasuries benefit from the asset’s scale, liquidity, and established derivatives markets, which allow for far better risk management. The same cannot be said for many firms concentrated in smaller tokens, where liquidity dries up quickly,” Miah commented.

Dori also noted that weaker DAT firms could be ‘weeded out.’ However, the decisive factor is not necessarily size — though larger players do benefit from cheaper capital and deeper liquidity — but rather their ability to create sustainable value beyond a simple buy-and-hold strategy in the underlying token.

Annelise Osborne, Chief Business Officer at Kadena, warned that history offers plenty of cautionary examples — from the collapse of Long-Term Capital Management and Bear Stearns to Lehman Brothers, AIG, and Enron. The common thread across these failures was complex financial structures, excessive leverage, and overexposure to volatile markets. Derivatives, algorithms, and risk models work — until they don’t.

According to her, DATs face similar structural vulnerabilities. Many lack meaningful cash flow or operational revenue, relying instead on the market value of the cryptocurrencies they hold or the yield those assets generate. Digital assets, by nature, are volatile and prone to sharp price swings.

While Bitcoin’s volatility has moderated as institutional holders take long-term positions, most other cryptocurrencies lack the same depth of demand and liquidity.

“DAT defi strategies include significant risk to increase the return generally using leverage on leverage. Market disruption could cause a house of cards to collapse. Also, markets are interconnected so can move together. When a market seizes, there can be limited to no liquidity. Sales can also cause significant drops in value. It could be a race to the bottom while unwinding a DAT,” she told BeInCrypto.

Despite this, Osborne outlined that DATs managed by experienced, compliant asset managers with strong risk controls are more likely to endure.

The Future of DATs

Finally, the experts also shared their long-term outlook for DATs. Sygnum’s CIO suggested that DATs will be seen as an important step in the broader institutionalization of digital assets over the next two to three years.

“Right now, they provide investors with convenient, listed-market access and pioneer new revenue and financing rails. In the medium- to long-term, the business model of these companies is likely to evolve over time to maintain a sustainable mNAV premium. For example, they might get more deeply engaged in supporting the ecosystem of the token they are invested in to develop additional revenue sources,” Dori disclosed to BeInCrypto.

Still, Miah envisions a clearer divergence ahead between Bitcoin-focused and multi-asset treasuries. In his view, Bitcoin treasuries will emerge as the most sustainable model within the next two to three years.

He forecasted that Bitcoin’s scale, liquidity, and growing regulatory clarity make it uniquely suited as a corporate reserve asset. Meanwhile, multi-asset treasuries are likely to continue facing structural challenges.

In conclusion, DATs mark an important phase in the institutional adoption of crypto, but not all will endure. Firms with disciplined governance, sustainable financing, and long-term conviction are best positioned to thrive. Others built on leverage or short-term speculation risk becoming the next casualties of market correction.