Decentralized finance (DeFi) lending platform Compound (COMP) can be considered the catalyst for the yield farming frenzy that kicked off in mid-2020.

While MakerDAO was the first DeFi project allowing users to take out loans, Compound was the first to offer permissionless lending pools, enabling users to earn interest on their crypto deposits.

In essence, Compound allows lenders and borrowers to interact directly with the protocol to earn or pay a floating interest rate. They do not have to negotiate terms such as maturity, interest rates, or collateral with the counterparty.

The protocol pools together Ethereum (ETH)-based assets, and lends them out at an automatically-adjusted floating rate, which is usually much better than that offered at any high street bank. Each money market is unique to the ERC-20 asset and contains a transparent ledger, with a record of all transactions and historical interest rates.

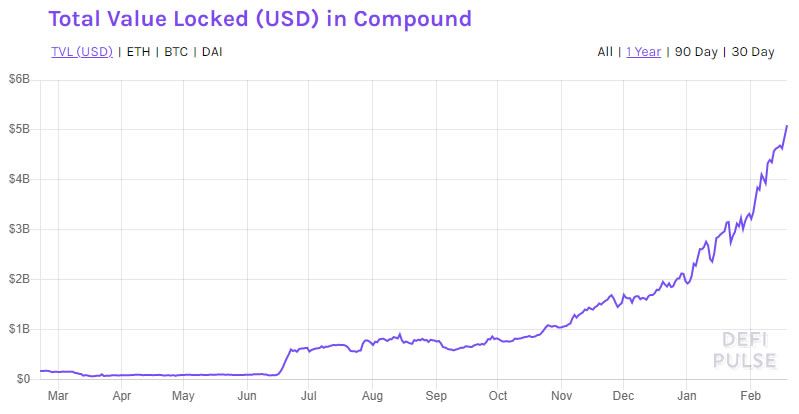

At the time of writing, Compound Finance was the third-largest DeFi protocol in terms of total value locked (TVL), which was a reported $5 billion according to DeFi Pulse.

Protocol history

The Compound Finance whitepaper was published in February 2019 by founder Robert Leshner and co-founder Geoffrey Hayes. It introduced a decentralized protocol that establishes money markets with algorithmically set interest rates based on supply and demand.

In 2018, Compound raised a little over $8 million in an initial seed round and an additional $25 million in a Series A round, in November 2019. The platform is heavily venture capital-backed with big names such as Andreessen Horowitz, Polychain Capital, and Coinbase Ventures taking part. These are now the largest holders of the governance token so can exert a major influence over voting and the direction of the protocol.

Compound Finance initially supported just six tokens: ether (ETH), 0x (ZRX), augur (REP), basic attention token (BAT), dai (DAI), and USDC. Currently, there are a couple more including wrapped bitcoin (WBTC), tether (USDT), uniswap (UNI), and, of course, its own COMP governance token.

How does it work?

Just like most DeFi protocols, crypto collateral must be provided before users can do anything on the system. Supplied asset balances are represented by cTokens, which are issued at 1:1 representing the underlying asset that earns interest and serves as collateral.

Supplying assets do involve additional confirmation transactions and gas fees, as do withdrawing them and claiming earned COMP. During times of high ethereum demand, gas fees can spike making the platform very expensive to use for small transactions.

Borrowing rates on these collateral tokens depend on which token it is, some have better values than others. These newly minted cTokens act as an IOU and redemption token, permitting the holder to redeem the original tokens.

Their value increases through the interest earned on the original collateral tokens, so cashing them out (or converting them back) usually yields more than the underlying assets.

Borrowing on Compound requires cTokens to be deposited as collateral, the factor of which, and amount that can be borrowed, varies depending on the token.

As an example, a user supplies 100 DAI as collateral, and the collateral factor for DAI is 75%, then the user can borrow at most 75 DAI worth of other assets at any given time. The protocol sets aside 10% of interest paid as reserves, and the rest goes to collateral suppliers.

Compound has its own “Open Price Feed” contract that has the current exchange rates of all supported assets. This is derived from high liquidity crypto exchanges and also used to calculate interest rates and collateral factors.

It bases its interest rate upon a “utilization rate,” which defines how much of lenders’ assets go out to borrowers in order to prevent a run on liquidity. As a result of these mechanisms, Compound survived the March 2020 “Black Thursday” event that caused mass liquidations on MakerDAO vaults.

If the debt position becomes larger than the amount of collateral (or under collateralized), the protocol exchanges the over-borrowed asset for the supplied collateral at a slightly lower than the market rate. The mechanism also acts as an incentive for users to manage their debt positions efficiently.

Compound also allows community members to act as liquidators using third-party tools like the Compounder Liquidator which allows them to repay others’ loans in return for ETH at a better market rate.

The protocol has had a number of security audits and is one of the few in the DeFi ecosystem that has not suffered a hack or flash loan exploit.

A yield farming pioneer

When Compound Finance launched its COMP governance token in June 2020, the team behind the project made the first step to decentralize the ownership, management, and governance of the protocol.

“By placing COMP directly into the hands of users and applications, an increasingly large ecosystem will be able to upgrade the protocol, and will be incentivized to collectively steward the protocol into the future with good governance.”

It was also the first yield farming incentive as Compound began distributing COMP to users of the protocol depending on how much collateral they had provided. Its ethos sparked a slew of copycats launching their own community governance tokens in a bid to become fully decentralized.

However, what actually happened to Compound, and a large number of DeFi protocols that followed, was the majority of tokens ending up in the bags of a few whales and early investors.

Either way, on its first day of trading on June 16, 2020, COMP became the most valuable DeFi asset, at the time, making the protocol a market cap “unicorn” as it reached a billion dollars.

The tokens were placed into a “Reservoir Contract,” which transferred 0.5 COMP per Ethereum block into the protocol for distribution. Around 2,880 tokens were distributed per day, at the time, and collateral surged as a result of the embryonic industry’s first real liquidity farm.

The Compound distribution tracker shows how much is distributed to each token pool. At the time of writing, over 614,000 COMP had been distributed and there were around 3.8 million to go under the protocols tokenomics system.

COMP tokenomics and governance

The primary purpose of the COMP token was for community governance, and according to Compound founder, Leshner:

“The individuals, applications and institutions that use the Compound protocol are capable of collectively stewarding it into the future — and are incentivized to provide good governance.”

However, since proposals are limited to addresses with more than 100,000 tokens, it is really only the whales and investors that can make a difference.

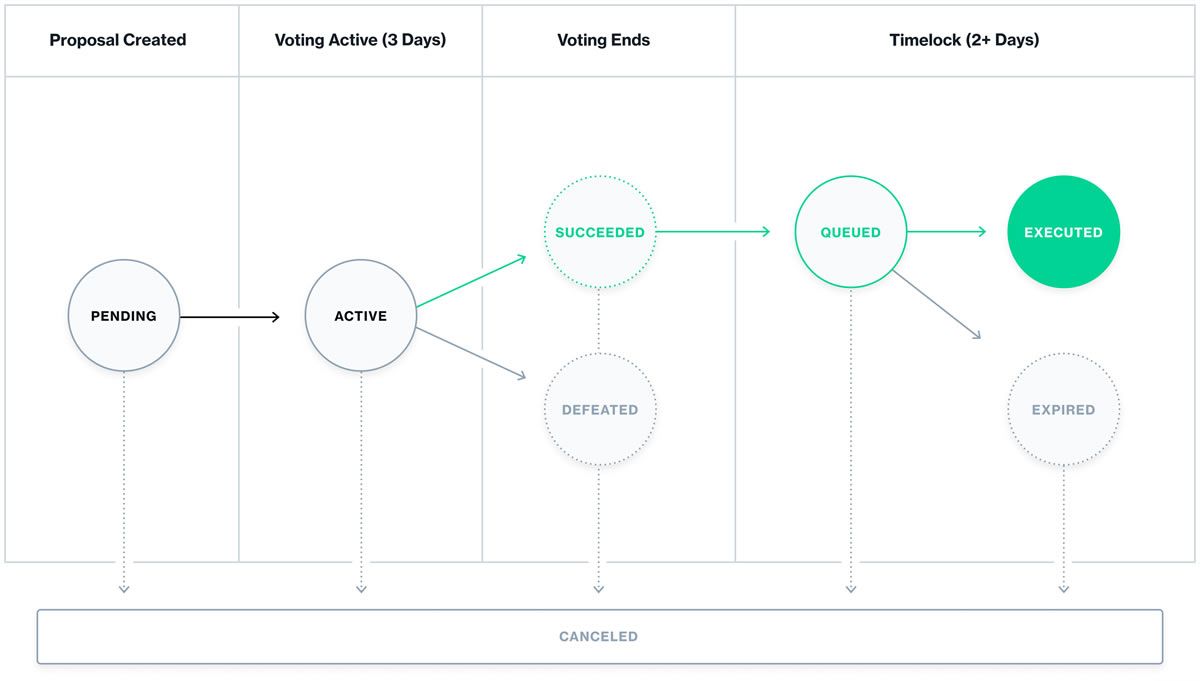

Once submitted, a three-day voting period commences and a minimum of 400,000 votes must be cast to reach quorum. If a majority of the votes support the proposal, the new change will be implemented after a two-day waiting period.

The public distribution of COMP includes approximately 4.3 million tokens out of a maximum supply of 10 million, dispersed over a four-year period via the protocol to liquidity providers.

The remaining 5.7 million tokens will be divided as follows: 24% going to shareholders of Compound Labs, with Andreessen Horowitz (a16z) and Polychain Capital owning almost 7%. These two token holders alone make up 27% of the voting power with Bain Capital Ventures holding an additional 10%, according to the protocol governance overview.

Compound founders and the team get 22.25% of the remaining COMP tokens which are subject to four-year vesting, and the rest will be reserved for new team members and future governance participation incentives.

The protocol is heavily venture capital-backed, with less than half of the token supply going into the hands of users and the community. While the platform itself is autonomous and decentralized, the governance system cannot really be considered so when compared to other DeFi platforms, though it is very transparent about this.

Compound Finance into 2021

Compound was the leading DeFi protocol by total value locked in mid-2020 as liquidity surged in propelling collateral levels to almost $1 billion by mid-August.

It started to lose ground to rival protocols offering better returns through food themed yield farms as the degen (degenerate) farming frenzy gathered steam. COMP token prices plunged from their launch peak of over $335 to below $100 by early November and TVL had dipped to $600,000.

However, being one of the early DeFi protocols like MakerDAO, Compound had a resurgence towards the end of the year and has surged into 2021 in terms of volume, token price, and liquidity.

By mid-February, COMP token prices had surged to a new all-time high of around $550 and total value locked on the platform reached a record $5 billion according to DappRadar. DeFiPulse reported a similar figure.

By mid-February 2021, there had been 38 governance proposals, 32 of which had been passed. Its highest earning interest, at the time of writing, was USDC, with 13% APY.

There have been no formal announcements yet but it is likely that the protocol will implement Layer 2 scaling solutions at some stage in 2021 to ease the burden of high transaction fees.