Bitcoin is often sold first during macro risk events because its perpetual futures–driven market structure embeds a persistent long bias and positive funding, making short exposure structurally easier and often cheaper during periods of stress.

- In the Perpetual Futures market, Bitcoin has exhibited a long-term bullish bias since its inception, with funding rates remaining positive (longs paying shorts) most of the time;

- Gold typically rises during macro stress events as investors add safe-heaven exposure. Bitcoin is frequently sold. This is more related to the perpetual funding structure instead of the “risk-on” or “risk-off” asset labels.

- Since Bitcoin funding is positive most of the time, an incremental wave of long demand would push the funding rate to even higher, increasing the carry cost of maintaining long exposure. By contrast, short positioning is cheaper, or even subsidized. The market structure and mechanism encourage shorting rather than longs under external stress.

In the previous article, we analyzed Bitcoin’s elevated volatility through a market structure lens, emphasizing its high volatility rooted in its derivatives-driven market structure, where speculative leverage and perpetual futures dominate price formation, which is in contrast to other major commodities like Gold or Oil which are operated in a physically anchored and comparatively low-leverage system.

Article: Whale’s Digital Asset View: Why Bitcoin Sells Off While Gold Stabilizes

This article examines a related question: why is Bitcoin consistently sold first during broad market risk events, particularly those that occur outside traditional market hours? Just as we stated in our previous article, the common explanation that labels Bitcoin as a “risk-on asset” is more of a description rather than an explanation. The relevant question is not whether Bitcoin is “risk-on” or “risk-off”, but:

- Which asset can absorb immediate macro hedging demand?

- Which market allows large-scale, frictionless short exposure at any time?

- Which assets structurally impose higher carrying costs on longs than on shorts?

Bitcoin satisfies all three conditions.

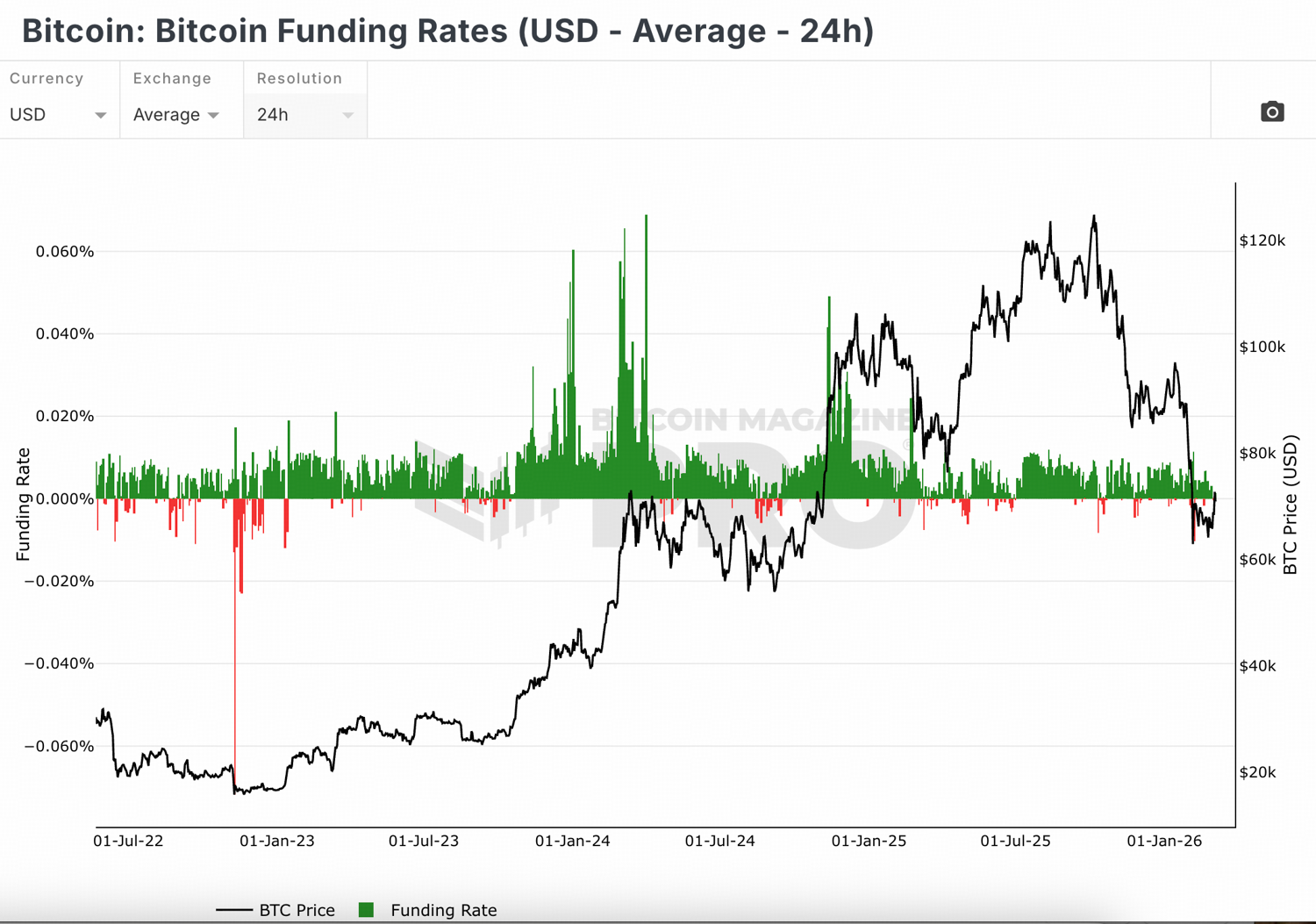

Bitcoin Funding Rates Remained Positive Over 90% of the Time

The crypto derivatives market, and Bitcoin in particular, is predominantly operated through perpetual futures rather than dated contracts. Across major exchanges, perpetual swaps account for the majority of derivatives volume and open interest. These instruments have no expiry date and are continuously margined, making them the primary instrument for short-term positioning and price discovery. In practice, Bitcoin’s spot market often follows the derivatives market rather than leading it.

Perpetual futures differ from traditional futures through their funding rate mechanism. Instead of converging to spot at expiry, they anchor to spot via periodic funding payments exchanged between longs and shorts. When the contract trades above spot, the funding rate is positive, and longs pay shorts. When it trades below spot, the funding rate is negative, and shorts pay longs. This system continuously balances directional demand.

Source: The Bitcoin Magazine

Bitcoin has exhibited a long-term bullish bias since its inception, with funding rates remaining positive (longs paying shorts) for most of the time, as shown on above chart. Across major exchanges (Binance, Bybit, etc.), Bitcoin perpetual funding rates have been positive on the majority of days, indicating that longs are willing to pay a “carry cost” to shorts to maintain upside exposure.

There is no definitive answer to this. One possible explanation is that Bitcoin is widely viewed as having long-term upside potential over extended time horizons, despite short-term volatility. Market participants tend to prefer long positioning over short positioning over multi-year periods.

Bitcoin is Structurally the Easiest Major Asset to Short

Bitcoin is the only large-scale macro asset that trades continuously, 24 hours a day, seven days a week, across both spot and derivatives markets. Liquidity is distributed globally across numerous centralized and decentralized exchanges and is anchored by a substantial perpetual futures market that drives short-term price discovery. When geopolitical or systemic shocks occur outside traditional market hours, Bitcoin becomes the only deep, tradable venue capable of absorbing immediate cross-asset hedging demand.

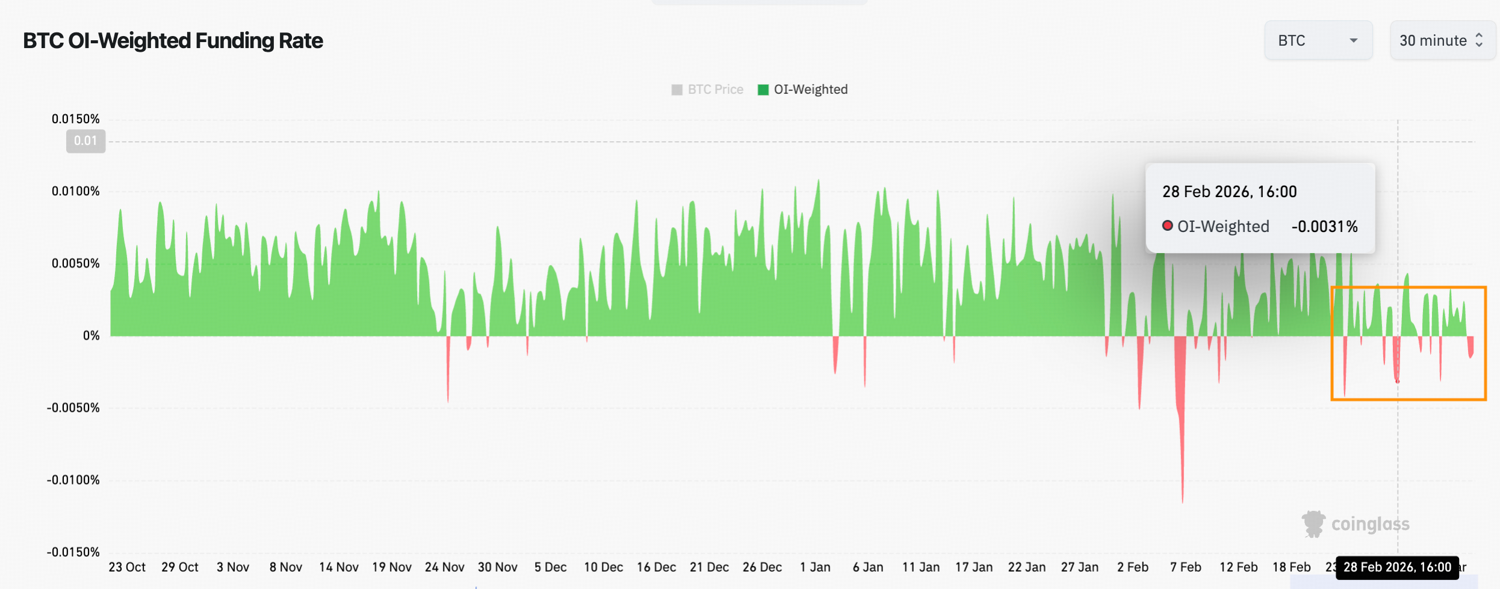

The fact that funding rates are positive most of the time implies that meaningful short capacity is structurally embedded in the market. The funding mechanism effectively subsidizes short exposure, reinforcing the market’s ability to scale short positioning when needed. And because of the high leverage on the long side (built up during positive funding period), the sudden scaling up of shorts often leads to forced liquidations when prices dip, creating mechanical selling pressures.

Source: Coinglass

As observed from the above chart, during periods of geopolitical shock or macro stress, funding rates often invert abruptly alongside rapid downside price moves and rising short-side open interest. The shift from consistently positive funding rate to sharply negative levels provides real-time evidence of concentrated short positioning.

The late January to Early March 2026 period provides a vivid example. Funding rates turned and stayed negative amid the outbreak of U.S.-Israel military strikes on Iran, starting around Feb 28, which occurred over a weekend. The negative funding rate reflects tactical hedging flows entering the market. Bitcoin is used as an immediate instrument for downside protection during risk-off events through shorting positioning.

This also clarifies the “digital gold” paradox. Gold often attracts safe-haven inflows during macro risk events, while Bitcoin is used as a liquid, always-on risk hedge vehicle, where a short position of Bitcoin to offset downside in correlated risk assets.

Bottom Line

Will this behavior change, and could Bitcoin evolve into a safe-haven asset similar to gold in the foreseeable future? The answer is probably No.

Under the current market structure, it simply does not favor long positions for Bitcoin during a risk-off event. Since Bitcoin funding is positive most of the time (longs paying shorts), an incremental wave of long demand would push the funding rate even higher, increasing the carry cost of maintaining long exposure. By contrast, short positioning is cheaper, or even subsidized.

In periods of external stress, this asymmetry in carrying costs tilts positioning toward shorting, reinforcing Bitcoin’s tendency to trade lower during macro shocks.

Disclaimer: The information provided herein does not constitute investment advice, financial advice, trading advice, or any other sort of advice, and should not be treated as such. All content set out below is for informational purposes only.