Over $2.3 billion in Bitcoin (BTC) and Ethereum (ETH) options near expiration today, amid growing defensive positioning, BTC holds firm near $71,500, and implied volatility retreats from recent highs.

Crypto futures open interest rose 2% to $102 billion in the past 24 hours. However, flat-to-negative funding rates and cumulative volume delta suggest the buildup is driven by cautious bearish bets rather than fresh long exposure.

Options Positioning Tilts Defensive

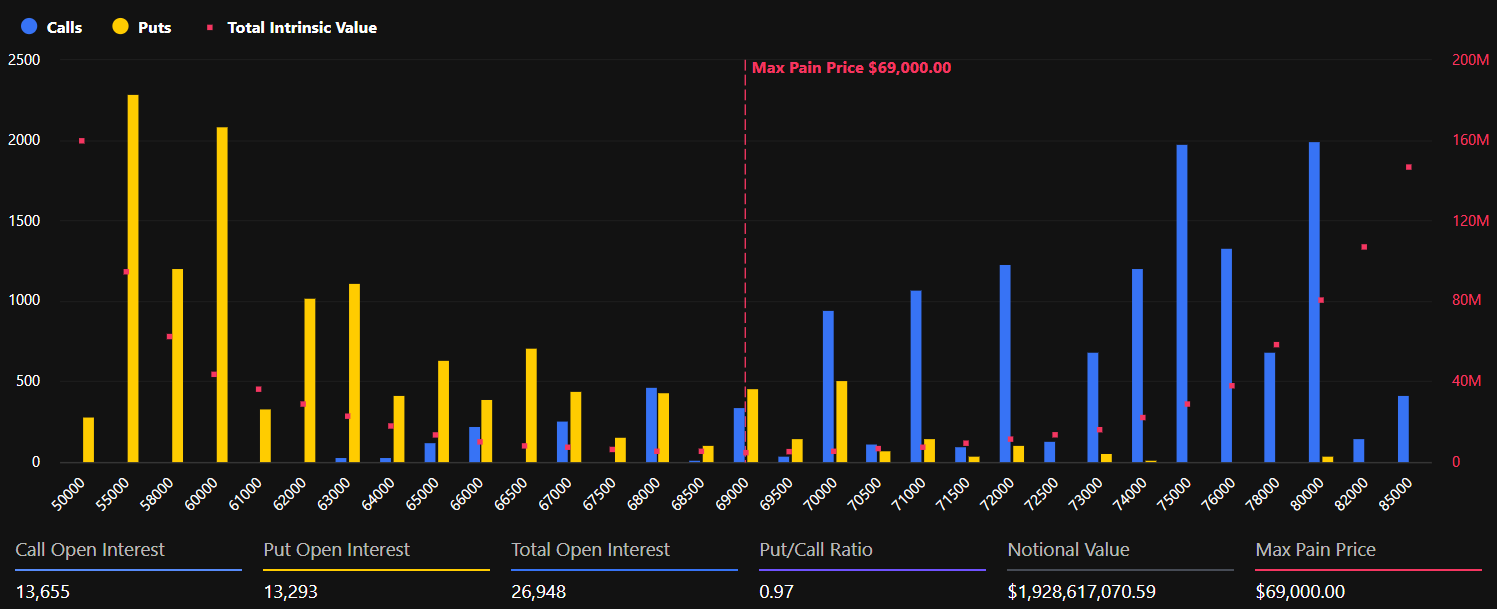

BTC options carry $1.93 billion in notional value across 26,948 contracts. The put-to-call ratio sits at 0.97, nearly balanced but with a slight defensive lean. Max pain rests at $69,000, just below spot price.

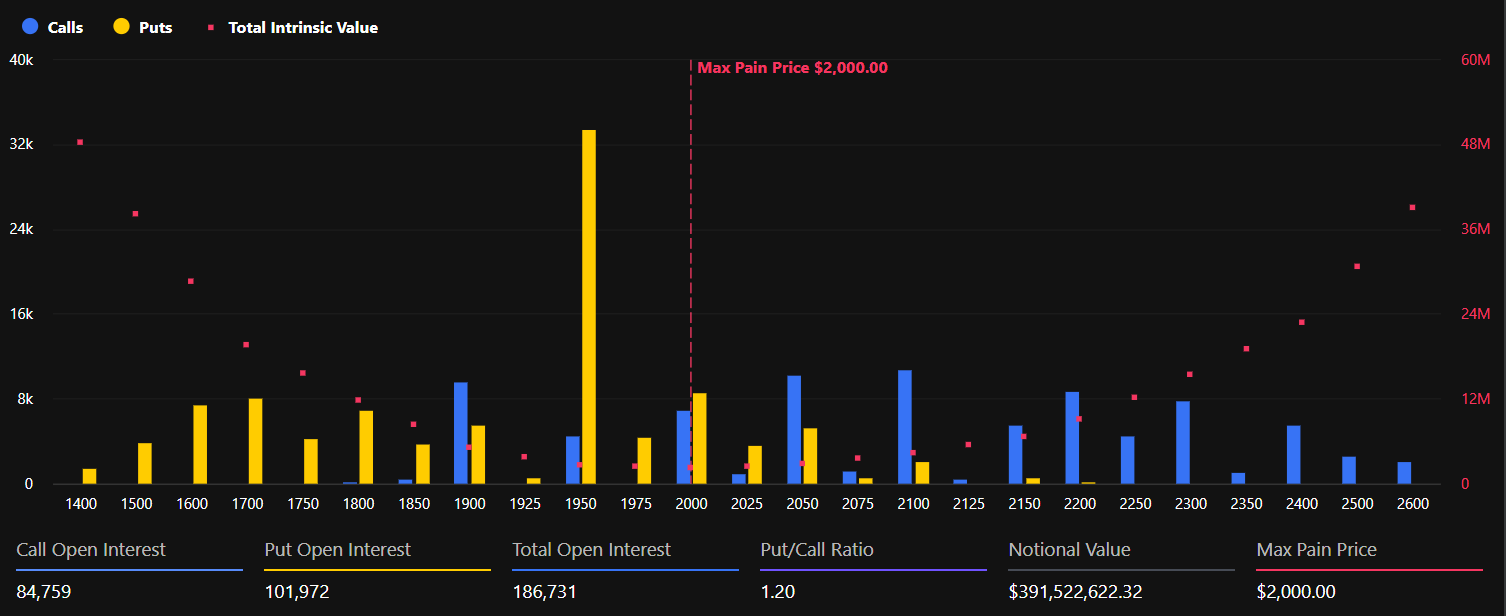

ETH positioning tells a sharper story. With $394 million in notional value across 186,732 contracts, Ethereum’s put-to-call ratio has climbed to 1.20.

That means put buyers outnumber call buyers by a significant margin, signaling hedging activity rather than directional conviction. Max pain for ETH sits at $2,000, roughly 5% below its current price of $2,110.

Greeks.live analysts noted that implied volatility across major maturities has pulled back sharply. The monthly volatility risk premium (VRP) dropped from +2% to -9% in a single day.

A widening negative VRP suggests traders expect future volatility to remain lower than current levels, even as broader macro risks escalate.

The $20,000 Put and What It Signals

On Deribit, the largest crypto options exchange, nearly $800 million in open interest is concentrated at the $20,000 BTC put strike.

That contract represents a wager that Bitcoin’s price will fall below that level. It ranks as the fourth-most popular bearish bet on the platform.

“Bitcoin looks resilient, but nearly $800 million in open interest is piled into the $20,000 put,” wrote analysts at Deribit.

Most of that open interest consists of short puts rather than directional long hedges, with traders known to often sell very far out-of-the-money puts as the chances of hitting those levels is minimal.

The consolidation pattern is flushing excess leverage from BTC, which tends to create a more stable base for the next directional move once a macro catalyst appears.

Oil, Bonds, and the Macro Squeeze

Bitcoin’s resilience above $70,000 is being tested by stress building in traditional markets. Crude oil benchmarks have pushed back toward $100 per barrel, rattling equity markets and reviving inflation concerns.

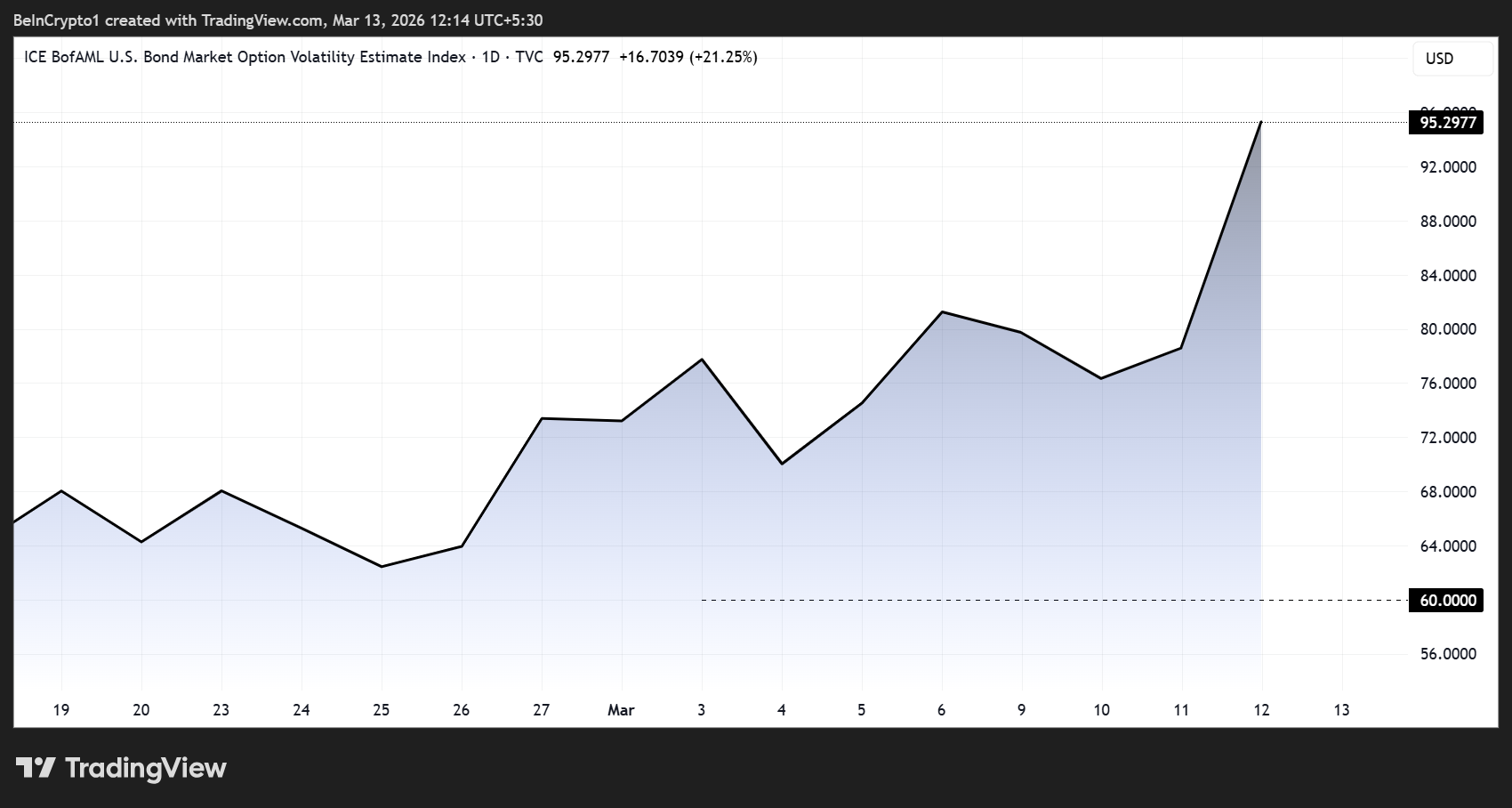

However, the more significant cross-asset signal is coming from bonds. The MOVE index, which measures 30-day expected volatility in U.S. Treasury notes, surged 21% to 95.30 on March 12 after sitting below 60 in late February.

Treasury notes serve as the pricing backbone for global finance. When bond volatility spikes, it typically tightens financial conditions and puts pressure on risk assets.

BTC and ETH implied volatility indices, BVIV and EVIV, have remained steady despite the oil rally and equity weakness. That stability suggests derivatives traders are not yet pricing in meaningful cross-asset contagion for major cryptos.

The disconnect may not last. If Treasury volatility continues to climb into next week’s FOMC meeting on March 17-18, the pressure could spill into crypto positioning.

For now, Bitcoin’s $69,000-$71,700 range holds, but the options market signals a trading community hedged and waiting rather than committed to direction.